Looking back on home furniture retailer stocks’ Q4 earnings, we examine this quarter’s best and worst performers, including Williams-Sonoma (NYSE: WSM) and its peers.

Furniture retailers understand that ‘home is where the heart is’ but that no home is complete without that comfy sofa to kick back on or a dreamy bed to rest in. These stores focus on providing not only what is practically needed in a house but also aesthetics, style, and charm in the form of tables, lamps, and mirrors. Decades ago, it was thought that furniture would resist e-commerce because of the logistical challenges of shipping large furniture, but now you can buy a mattress online and get it in a box a few days later; so just like other retailers, furniture stores need to adapt to new realities and consumer behaviors.

The 4 home furniture retailer stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 0.9% while next quarter’s revenue guidance was 0.9% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 28.6% since the latest earnings results.

Williams-Sonoma (NYSE: WSM)

Started in 1956 as a store specializing in French cookware, Williams-Sonoma (NYSE: WSM) is a specialty retailer of higher-end kitchenware, home goods, and furniture.

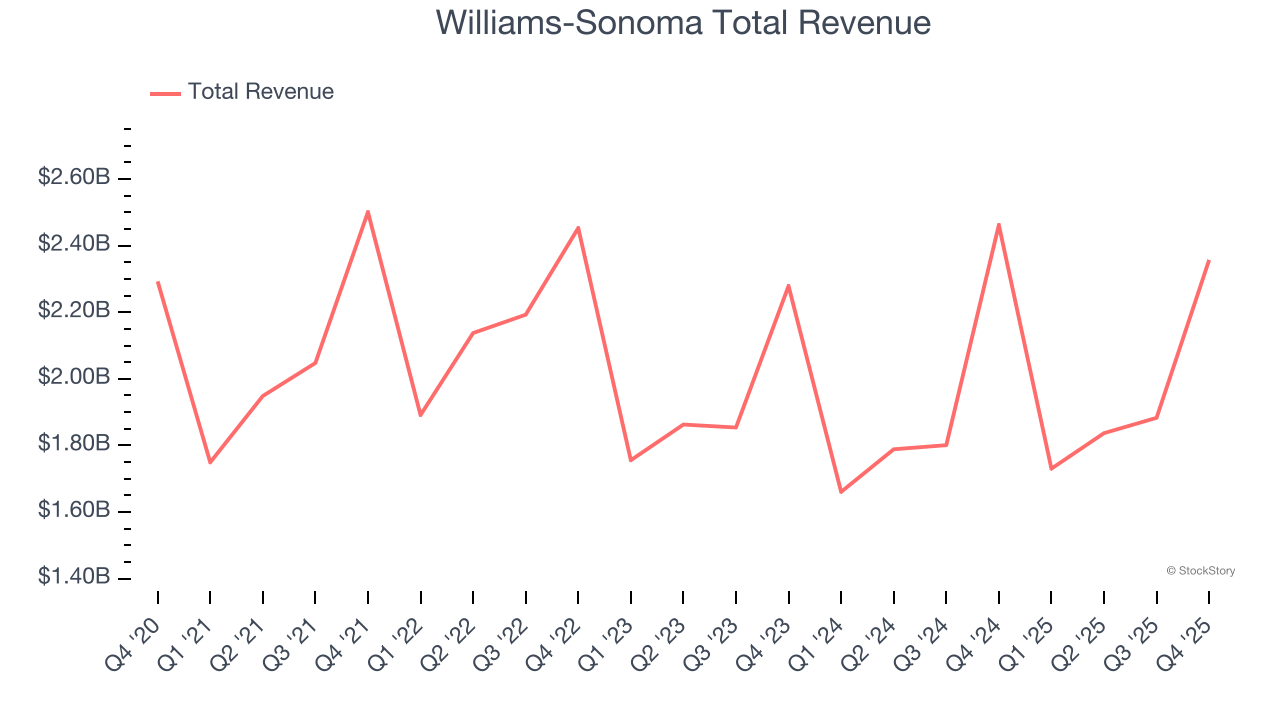

Williams-Sonoma reported revenues of $2.36 billion, down 4.3% year on year. This print fell short of analysts’ expectations by 2.5%. Overall, it was a mixed quarter for the company with an impressive beat of analysts’ gross margin estimates but a miss of analysts’ revenue estimates.

“We are proud of our strong finish to 2025. In Q4, our comp came in at +3.2%, and we delivered an operating margin of 20.3% with earnings per share of $3.04. Normalizing for the 53rd week last year and the tariff impact this year, we delivered substantial operating margin improvement versus last year. As we look forward to 2026 and beyond, we are confident in our competitive advantages that have allowed us to take market share, and our focus is on widening that advantage,” said Laura Alber, President and Chief Executive Officer.

The market was likely pricing in the results, and the stock is flat since reporting. It currently trades at $182.24.

Read our full report on Williams-Sonoma here, it’s free.

Best Q4: Sleep Number (NASDAQ: SNBR)

Known for mattresses that can be adjusted with regards to firmness, Sleep Number (NASDAQ: SNBR) manufactures and sells its own brand of bedding products such as mattresses, bed frames, and pillows.

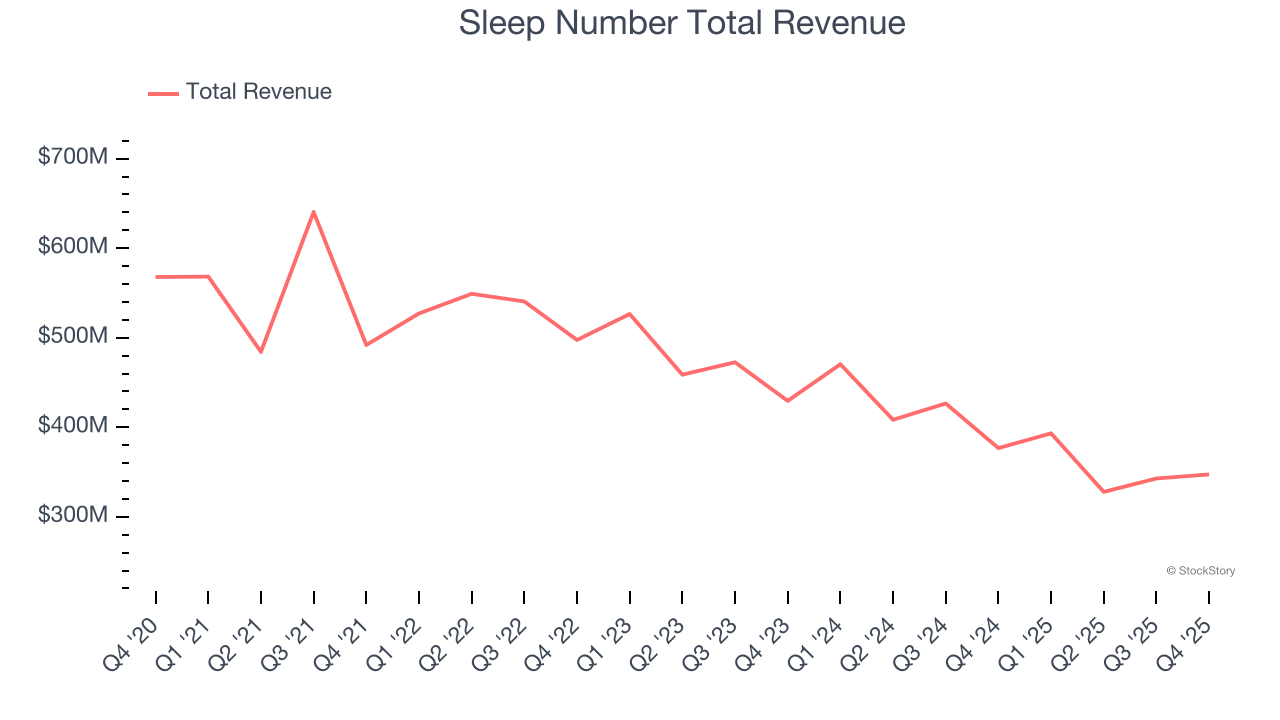

Sleep Number reported revenues of $347.4 million, down 7.8% year on year, outperforming analysts’ expectations by 5.7%. The business had a stunning quarter with a beat of analysts’ EPS and EBITDA estimates.

Sleep Number achieved the biggest analyst estimates beat among its peers. Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 74.6% since reporting. It currently trades at $1.17.

Is now the time to buy Sleep Number? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: RH (NYSE: RH)

Formerly known as Restoration Hardware, RH (NYSE: RH) is a specialty retailer that exclusively sells its own brand of high-end furniture and home decor.

RH reported revenues of $842.6 million, up 3.7% year on year, falling short of analysts’ expectations by 3.6%. It was a disappointing quarter as it posted revenue guidance for next quarter missing analysts’ expectations and a significant miss of analysts’ EBITDA estimates.

RH delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 15.5% since the results and currently trades at $118.15.

Read our full analysis of RH’s results here.

Arhaus (NASDAQ: ARHS)

With an aesthetic that features natural materials such as reclaimed wood, Arhaus (NASDAQ: ARHS) is a high-end furniture retailer that sells everything from sofas to rugs to bookcases.

Arhaus reported revenues of $364.8 million, up 5.1% year on year. This print topped analysts’ expectations by 4.1%. Aside from that, it was a satisfactory quarter as it also produced an impressive beat of analysts’ EBITDA estimates but revenue guidance for next quarter missing analysts’ expectations.

Arhaus pulled off the fastest revenue growth among its peers. The stock is down 24.2% since reporting and currently trades at $6.36.

Read our full, actionable report on Arhaus here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.