Shareholders of PennyMac Financial Services would probably like to forget the past six months even happened. The stock dropped 39.3% and now trades at $80.08. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in PennyMac Financial Services, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is PennyMac Financial Services Not Exciting?

Even with the cheaper entry price, we’re swiping left on PennyMac Financial Services for now. Here are three reasons we avoid PFSI, plus one stock we’d rather own.

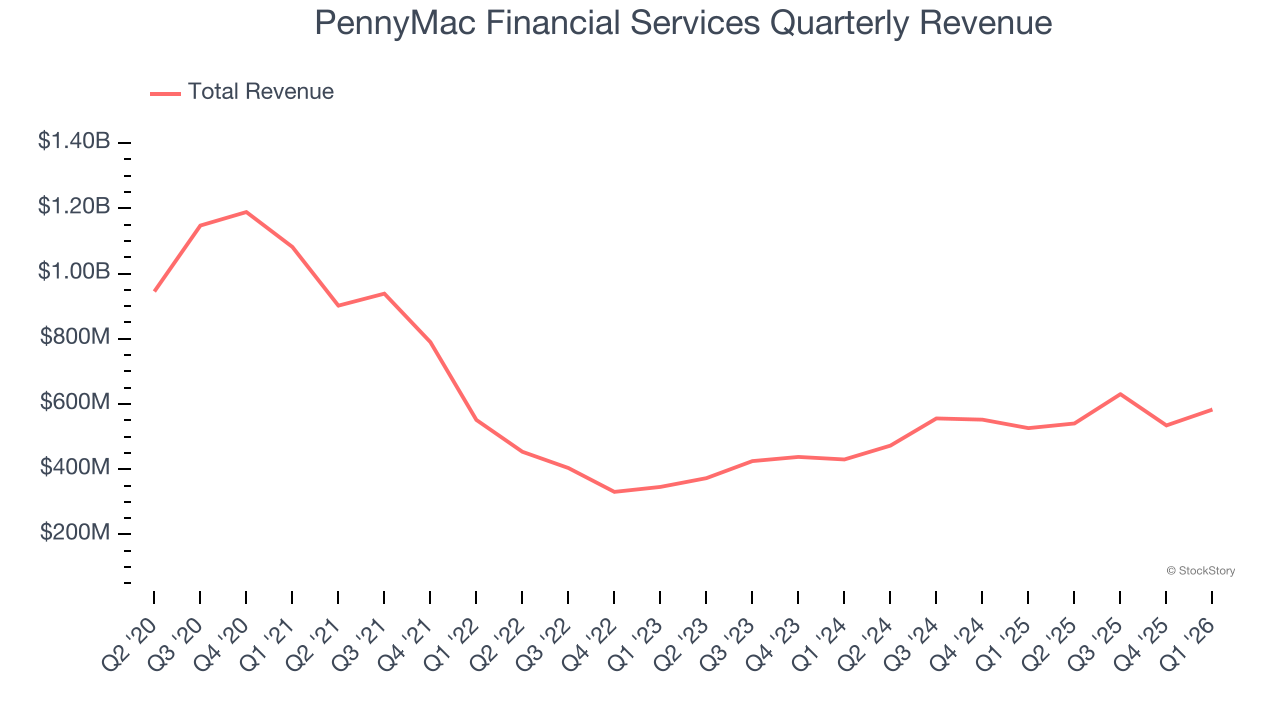

1. Revenue Spiraling Downwards

Net interest income and fee-based revenue are the two pillars supporting bank earnings. The former captures profit from the gap between lending rates and deposit costs, while the latter encompasses charges for banking services, credit products, wealth management, and trading activities.

PennyMac Financial Services struggled to consistently generate demand over the last five years as its revenue dropped at a 12.1% annual rate. This wasn’t a great result and signals it’s a lower quality business.

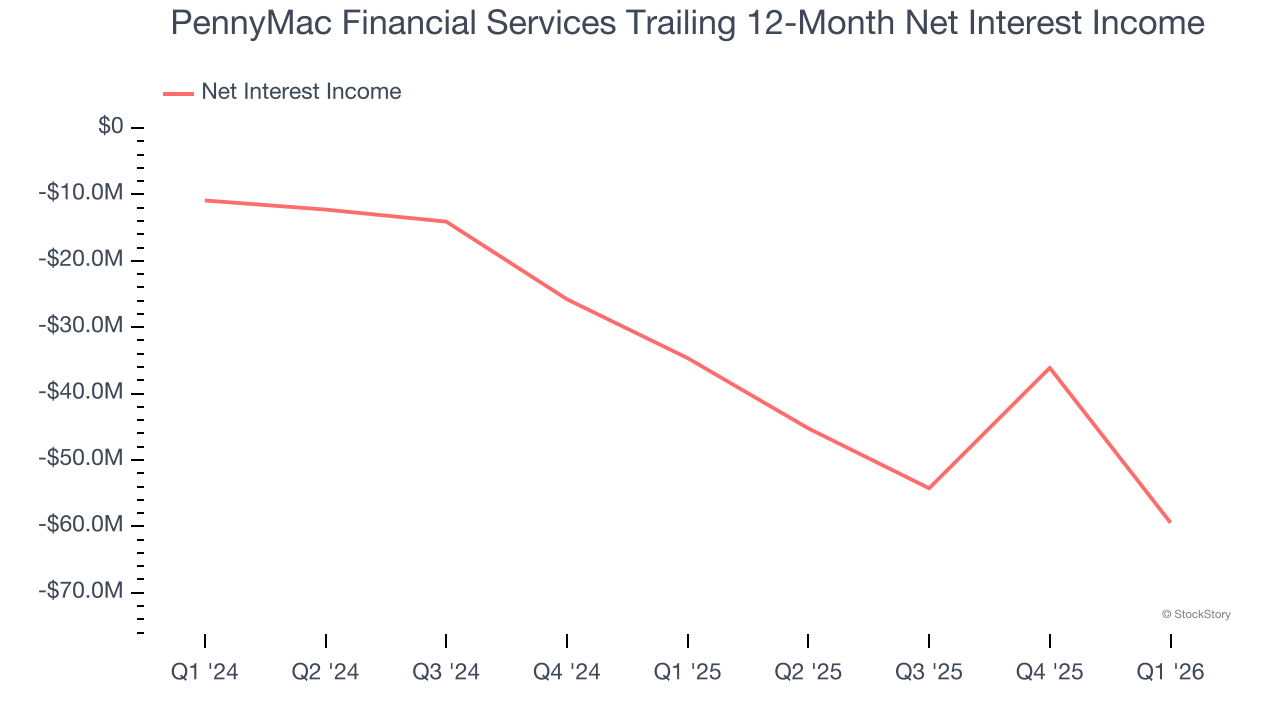

2. Net Interest Income Points to Soft Demand

Markets consistently prioritize net interest income over non-recurring fees, recognizing its superior quality compared to the more unpredictable revenue streams.

PennyMac Financial Services’s net interest income has grown at a 4% annualized rate over the last five years, much worse than the broader banking industry.

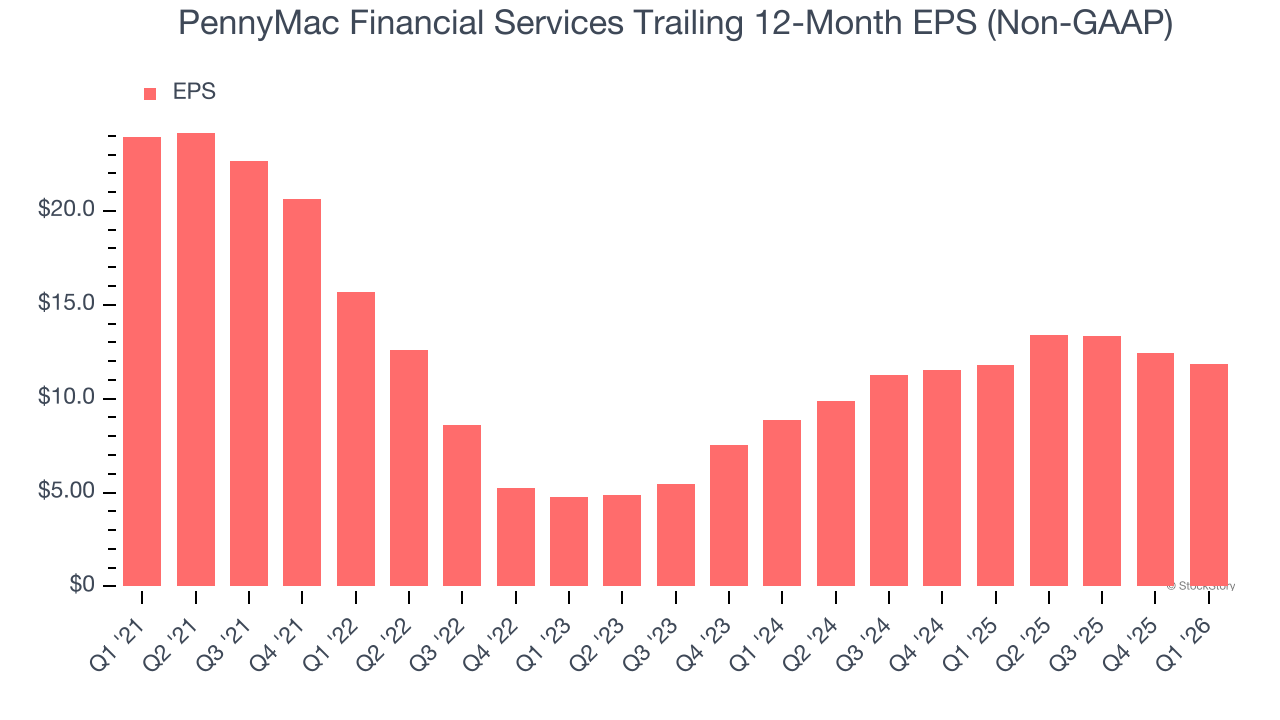

3. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for PennyMac Financial Services, its EPS and revenue declined by 13.1% and 12.1% annually over the last five years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, PennyMac Financial Services’s low margin of safety could leave its stock price susceptible to large downswings.

Final Judgment

PennyMac Financial Services’s business quality ultimately falls short of our standards. Following the recent decline, the stock trades at 0.9× forward P/B (or $80.08 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We’re pretty confident there are more exciting stocks to buy at the moment. Let us point you toward the most entrenched endpoint security platform on the market.

Stocks We Like More Than PennyMac Financial Services

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.