The past six months have been a windfall for Hewlett Packard Enterprise’s shareholders. The company’s stock price has jumped 82.6%, hitting $44.82 per share. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is it too late to buy HPE? Find out in our full research report, it’s free.

Why Is HPE a Good Business?

Born from the 2015 split of the iconic Silicon Valley pioneer Hewlett-Packard, Hewlett Packard Enterprise (NYSE: HPE) provides edge-to-cloud technology solutions that help businesses capture, analyze, and act upon their data across hybrid IT environments.

1. ARR Surges as Recurring Revenue Flows In

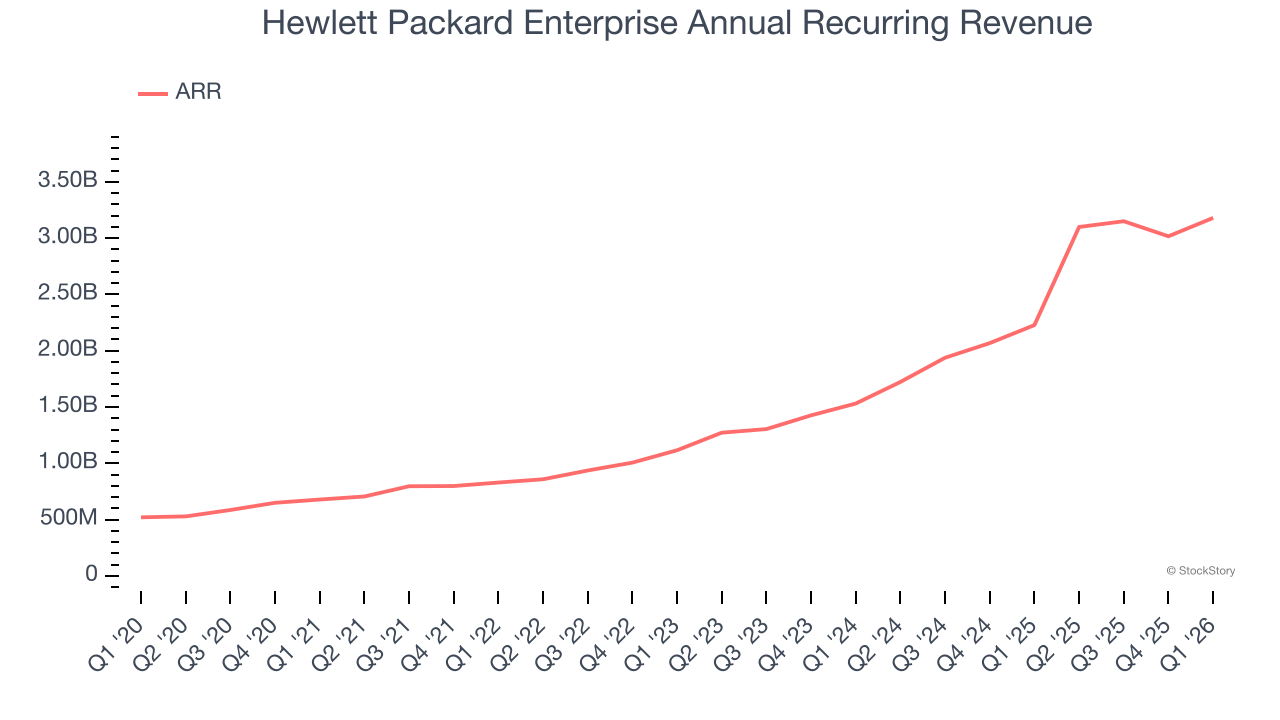

We can better understand Hardware & Infrastructure companies by analyzing their ARR, or annual recurring revenue. This metric shows how much Hewlett Packard Enterprise expects to collect from its existing customer base in the next 12 months, giving visibility into its future revenue streams.

Hewlett Packard Enterprise’s ARR punched in at $3.18 billion in the latest quarter, and over the last two years, its year-on-year growth averaged 50.7%. This performance was fantastic and shows that customers are willing to take multi-year bets on the company’s product offerings. Its growth also makes Hewlett Packard Enterprise a more predictable business, a tailwind for its valuation as investors typically prefer businesses with recurring revenue.

2. Economies of Scale Give It Negotiating Leverage with Suppliers

With $38.79 billion in revenue over the past 12 months, Hewlett Packard Enterprise is a behemoth in the business services sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices.

3. Projected Revenue Growth Is Remarkable

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite, though some deceleration is natural as businesses become larger.

Over the next 12 months, sell-side analysts expect Hewlett Packard Enterprise’s revenue to rise by 25.3%, an improvement versus its 7.1% annualized growth for the past five years. This projection is eye-popping for a company of its scale and suggests its newer products and services will spur better top-line performance.

Final Judgment

These are just a few reasons Hewlett Packard Enterprise is a rock-solid business worth owning, and with the recent surge, the stock trades at 12.5× forward P/E (or $44.82 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Hewlett Packard Enterprise

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.