Coty has gotten torched over the last six months - since December 2025, its stock price has dropped 37.3% to $2.05 per share. This might have investors contemplating their next move.

Is there a buying opportunity in Coty, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Do We Think Coty Will Underperform?

Despite the more favorable entry price, we don’t have much confidence in Coty. Here are three reasons we avoid COTY, plus one stock we’d rather own.

1. Core Business Falling Behind as Organic Sales Decline

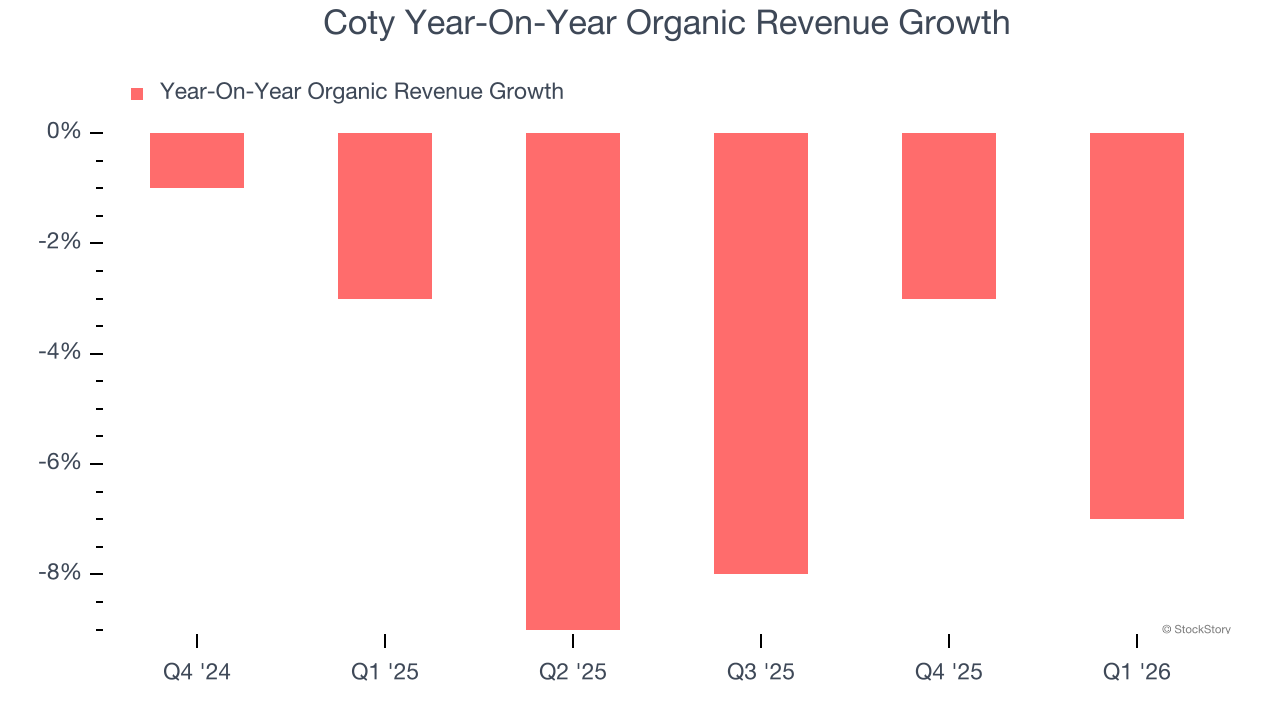

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

Coty’s demand has been falling over the last eight quarters, and on average, its organic sales have declined by 5.2% year on year.

2. Projected Revenue Growth Shows Limited Upside

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Coty’s revenue to stall, a deceleration versus This projection is underwhelming and indicates its products will see some demand headwinds.

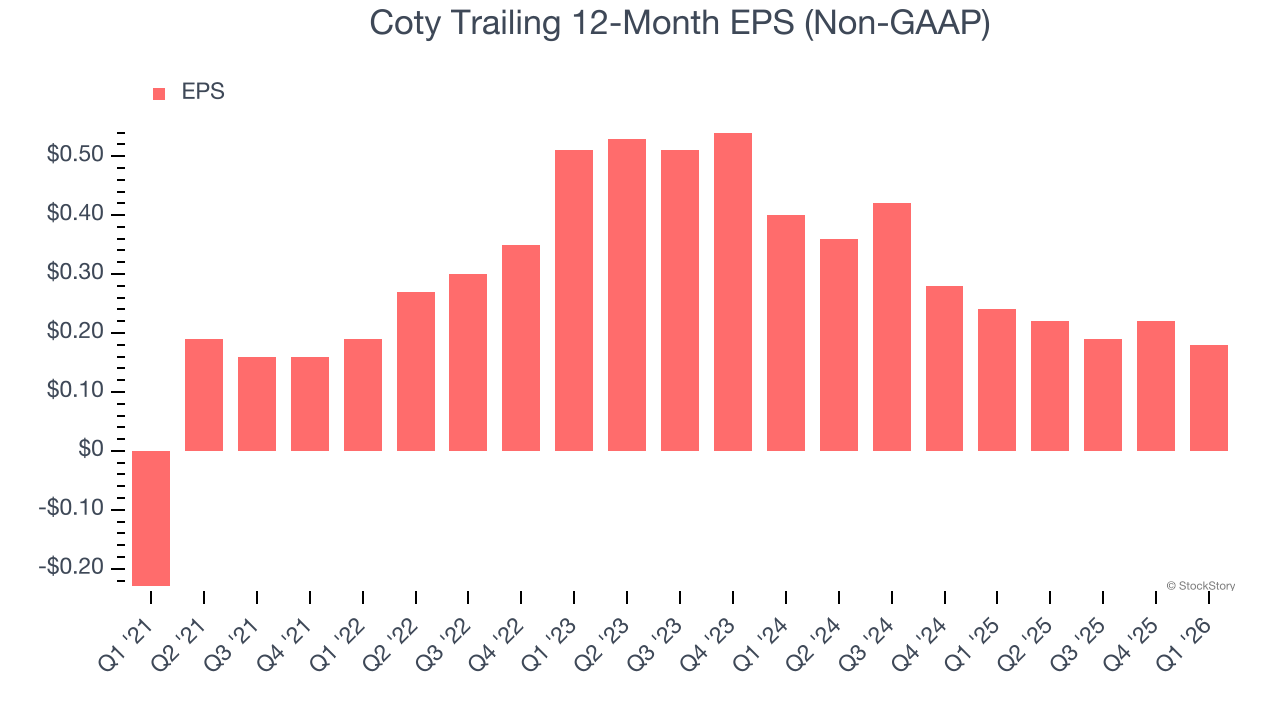

3. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Coty, its EPS declined by 29.3% annually over the last three years while its revenue grew by 2.5%. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

We see the value of companies helping consumers, but in the case of Coty, we’re out. After the recent drawdown, the stock trades at 6.1× forward P/E (or $2.05 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better stocks to buy right now. Let us point you toward the most dominant software business in the world.

Stocks We Would Buy Instead of Coty

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.