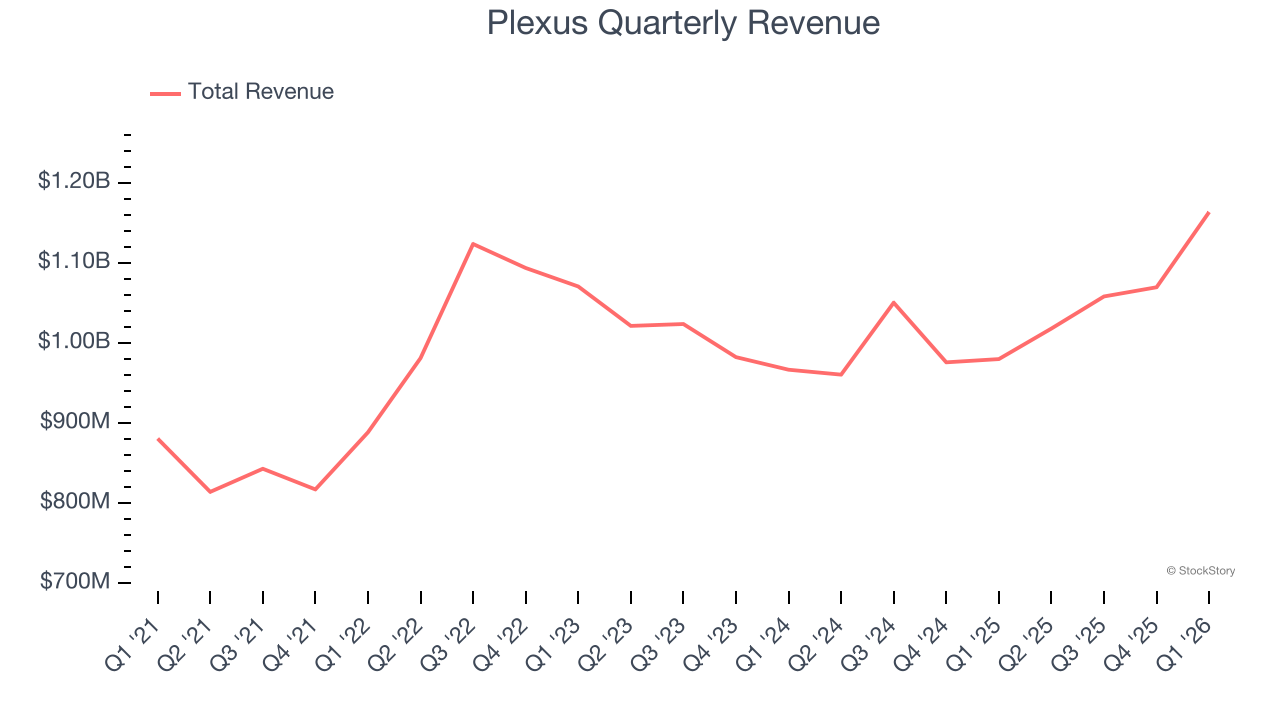

Electronic manufacturing services company Plexus (NASDAQ: PLXS) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 18.7% year on year to $1.16 billion. On top of that, next quarter’s revenue guidance ($1.23 billion at the midpoint) was surprisingly good and 6.5% above what analysts were expecting. Its non-GAAP profit of $2.05 per share was 8.8% above analysts’ consensus estimates.

Is now the time to buy Plexus? Find out by accessing our full research report, it’s free.

Plexus (PLXS) Q1 CY2026 Highlights:

- Revenue: $1.16 billion vs analyst estimates of $1.13 billion (18.7% year-on-year growth, 2.9% beat)

- Adjusted EPS: $2.05 vs analyst estimates of $1.88 (8.8% beat)

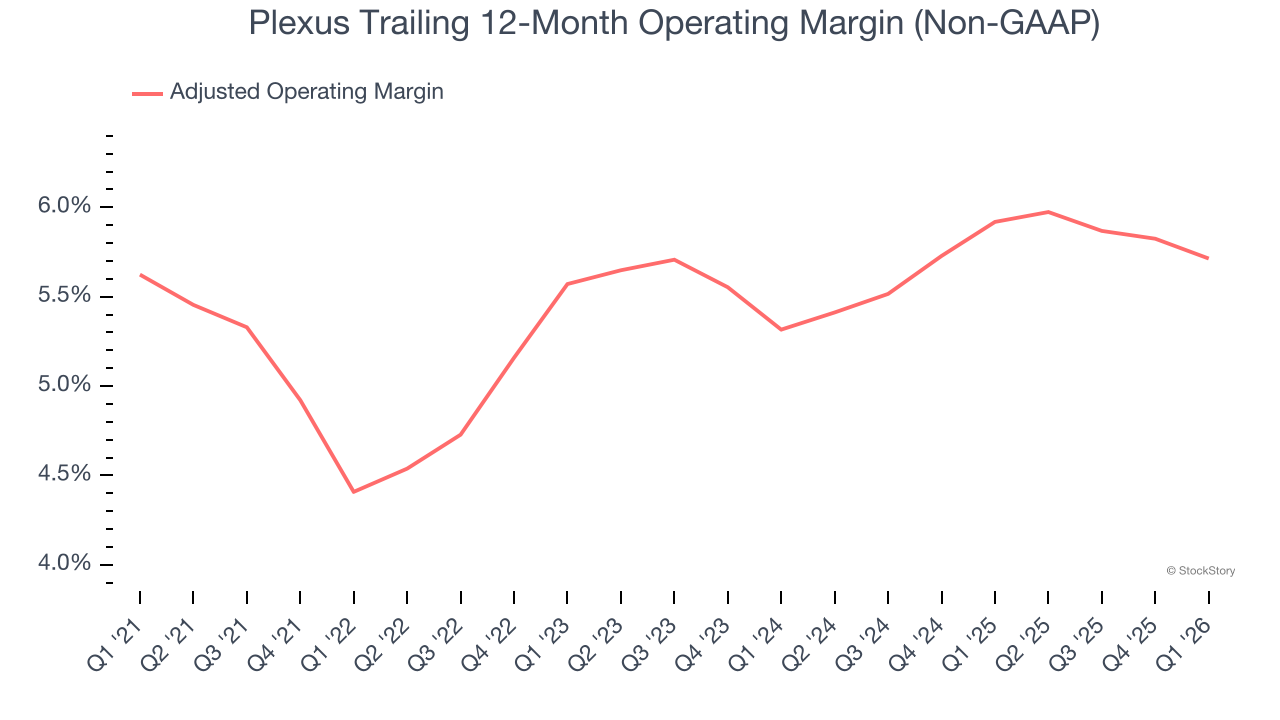

- Adjusted Operating Income: $61.84 million vs analyst estimates of $66.13 million (5.3% margin, 6.5% miss)

- Revenue Guidance for Q2 CY2026 is $1.23 billion at the midpoint, above analyst estimates of $1.15 billion

- Adjusted EPS guidance for Q2 CY2026 is $2.10 at the midpoint, above analyst estimates of $1.99

- Operating Margin: 5.3%, in line with the same quarter last year

- Market Capitalization: $6.60 billion

Todd Kelsey, President and Chief Executive Officer, commented, “Our momentum is accelerating broadly. For the fiscal second quarter, we increased revenue significantly year-over-year, delivered record manufacturing wins, expanded our efficiency efforts and generated robust profitability. We produced record revenue of $1.164 billion, which exceeded our guidance range and increased 19% year-over-year with significant contributions from all market sectors. In addition, non-GAAP operating margin of 6.0% met the high end of guidance, while non-GAAP EPS of $2.05 exceeded guidance.”

Company Overview

With over 20,000 team members across 26 global facilities, Plexus (NASDAQ: PLXS) designs, manufactures, and services complex electronic products for companies in aerospace/defense, healthcare, and industrial sectors.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $4.31 billion in revenue over the past 12 months, Plexus is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because it’s harder to find incremental growth when you’ve penetrated most of the market. To accelerate sales, Plexus likely needs to optimize its pricing or lean into new offerings and international expansion.

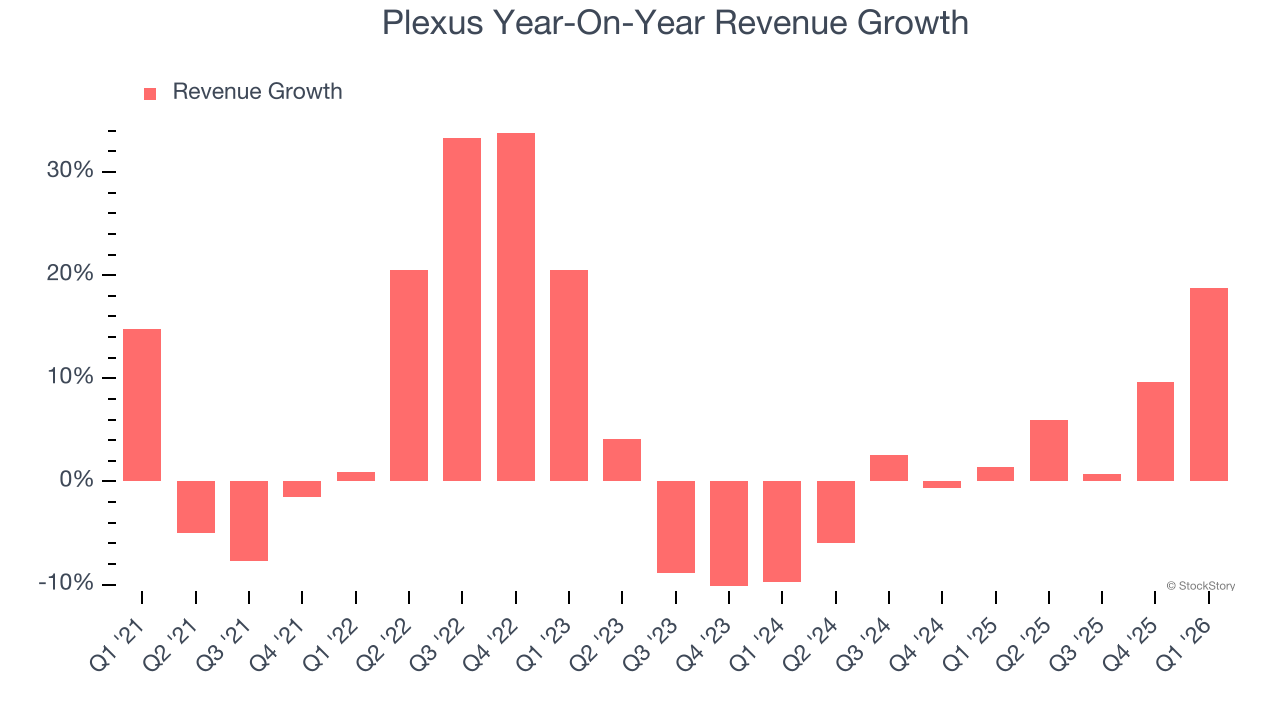

As you can see below, Plexus’s 4.4% annualized revenue growth over the last five years was mediocre. This shows it couldn’t generate demand in any major way and is a tough starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Plexus’s annualized revenue growth of 3.9% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

This quarter, Plexus reported year-on-year revenue growth of 18.7%, and its $1.16 billion of revenue exceeded Wall Street’s estimates by 2.9%. Company management is currently guiding for a 20.3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 9.1% over the next 12 months, an improvement versus the last two years. This projection is commendable and indicates its newer products and services will spur better top-line performance.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Adjusted Operating Margin

Plexus was profitable over the last five years but held back by its large cost base. Its average adjusted operating margin of 5.4% was weak for a business services business.

On the plus side, Plexus’s adjusted operating margin rose by 1.3 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Plexus generated an adjusted operating margin profit margin of 5.3%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

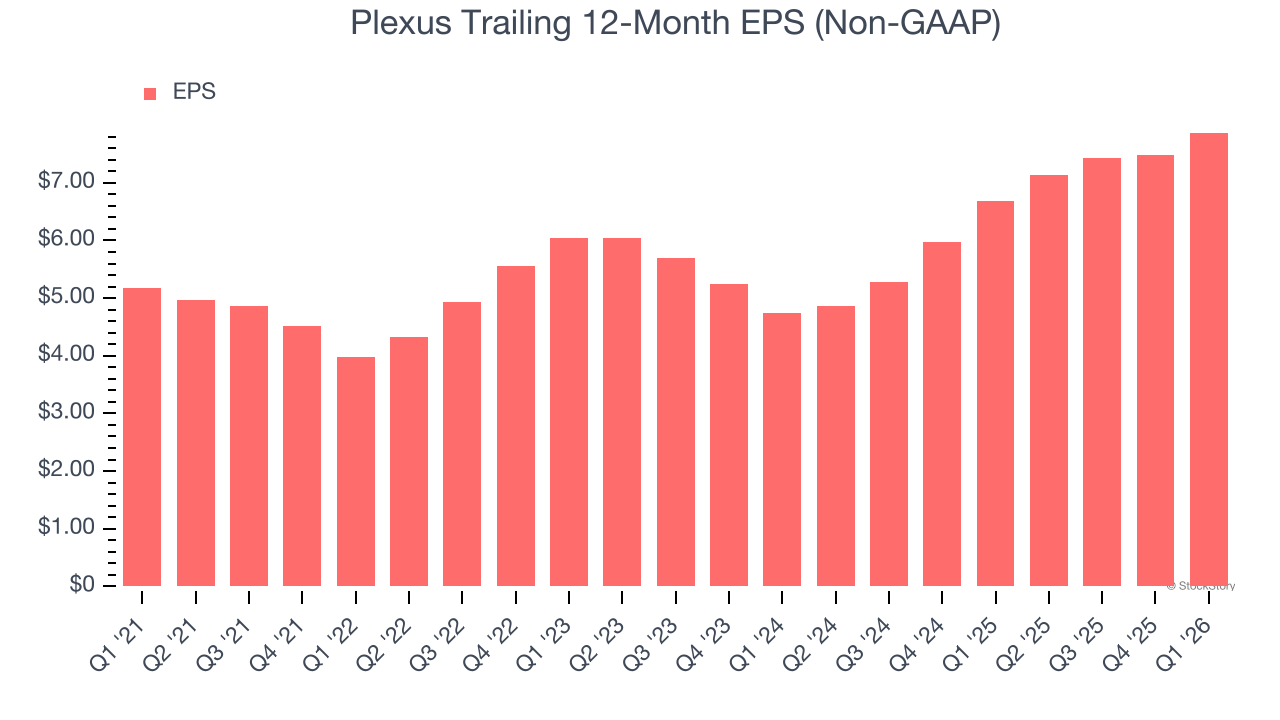

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Plexus’s EPS grew at 8.7% compounded annual growth rate over the last five years, higher than its 4.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

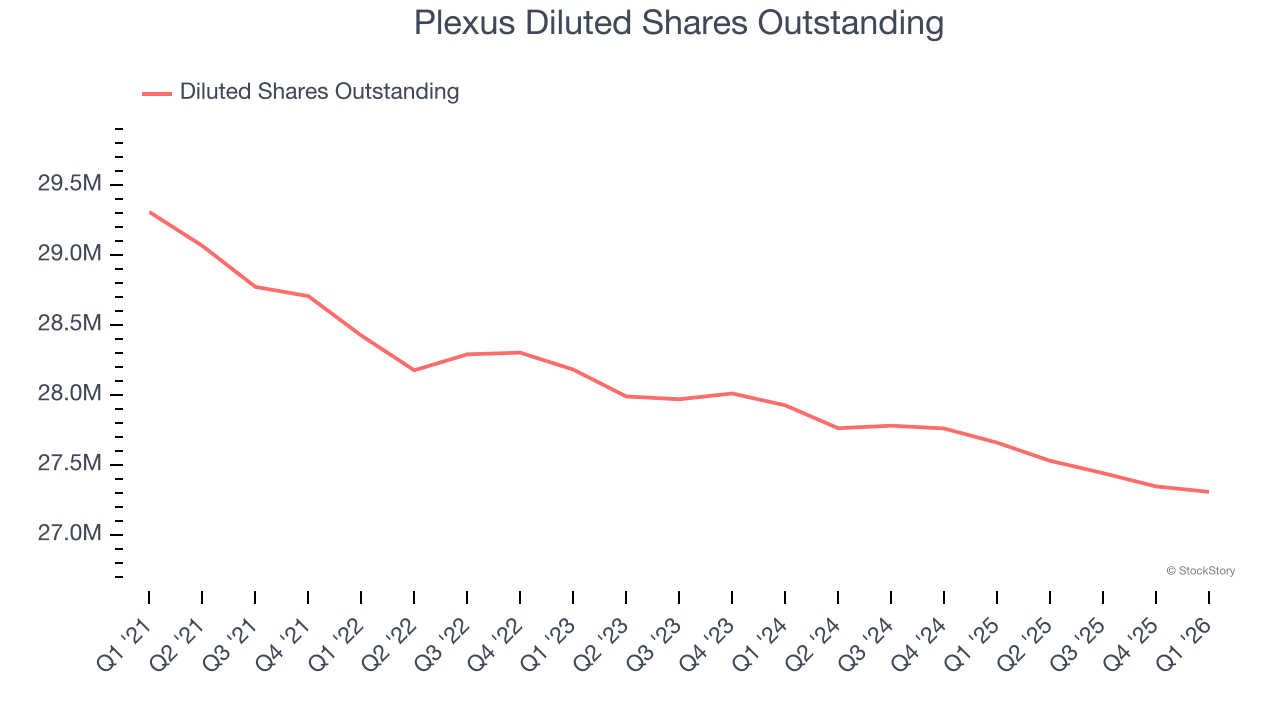

We can take a deeper look into Plexus’s earnings to better understand the drivers of its performance. As we mentioned earlier, Plexus’s adjusted operating margin was flat this quarter but expanded by 1.3 percentage points over the last five years. On top of that, its share count shrank by 6.8%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Plexus, its two-year annual EPS growth of 28.9% was higher than its five-year trend. This acceleration made it one of the faster-growing business services companies in recent history.

In Q1, Plexus reported adjusted EPS of $2.05, up from $1.66 in the same quarter last year. This print beat analysts’ estimates by 8.8%. Over the next 12 months, Wall Street expects Plexus’s full-year EPS of $7.87 to grow 3.9%.

Key Takeaways from Plexus’s Q1 Results

We were impressed by how significantly Plexus blew past analysts’ EPS guidance for next quarter expectations this quarter. We were also glad its revenue guidance for next quarter trumped Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock remained flat at $248.44 immediately following the results.

Is Plexus an attractive investment opportunity at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).