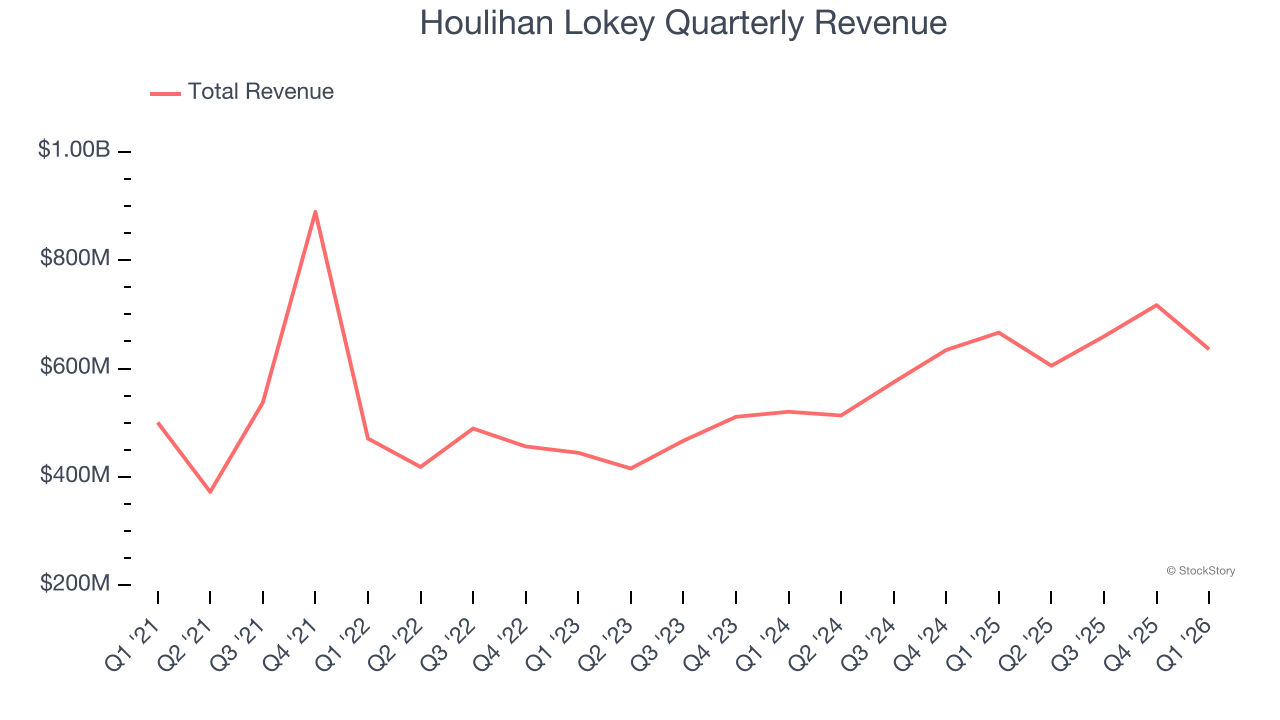

Investment banking firm Houlihan Lokey (NYSE: HLI) fell short of the market’s revenue expectations in Q1 CY2026, with sales falling 4.6% year on year to $635.6 million. Its non-GAAP profit of $1.63 per share was 8.9% below analysts’ consensus estimates.

Is now the time to buy Houlihan Lokey? Find out by accessing our full research report, it’s free.

Houlihan Lokey (HLI) Q1 CY2026 Highlights:

- Revenue: $635.6 million vs analyst estimates of $679.4 million (4.6% year-on-year decline, 6.4% miss)

- Adjusted EBITDA: $133.2 million vs analyst estimates of $172.8 million (21% margin, 22.9% miss)

- Adjusted EPS: $1.63 vs analyst expectations of $1.79 (8.9% miss)

- Market Capitalization: $10.48 billion

“Despite a challenging external environment, fiscal 2026 was another record year for our firm, demonstrating the resilience and diversification of our business model. Although there is some uncertainty in the market as we enter fiscal 2027, we remain optimistic about the prospects across all three of our business lines,” stated Scott Adelson, Chief Executive Officer of Houlihan Lokey.

Company Overview

Founded in 1972 and known for its expertise in complex financial situations, Houlihan Lokey (NYSE: HLI) is a global investment bank specializing in mergers and acquisitions, capital markets, financial restructurings, and valuation advisory services.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Houlihan Lokey’s 11.4% annualized revenue growth over the last five years was solid. Its growth surpassed the average financials company and shows its offerings resonate with customers, a great starting point for our analysis.

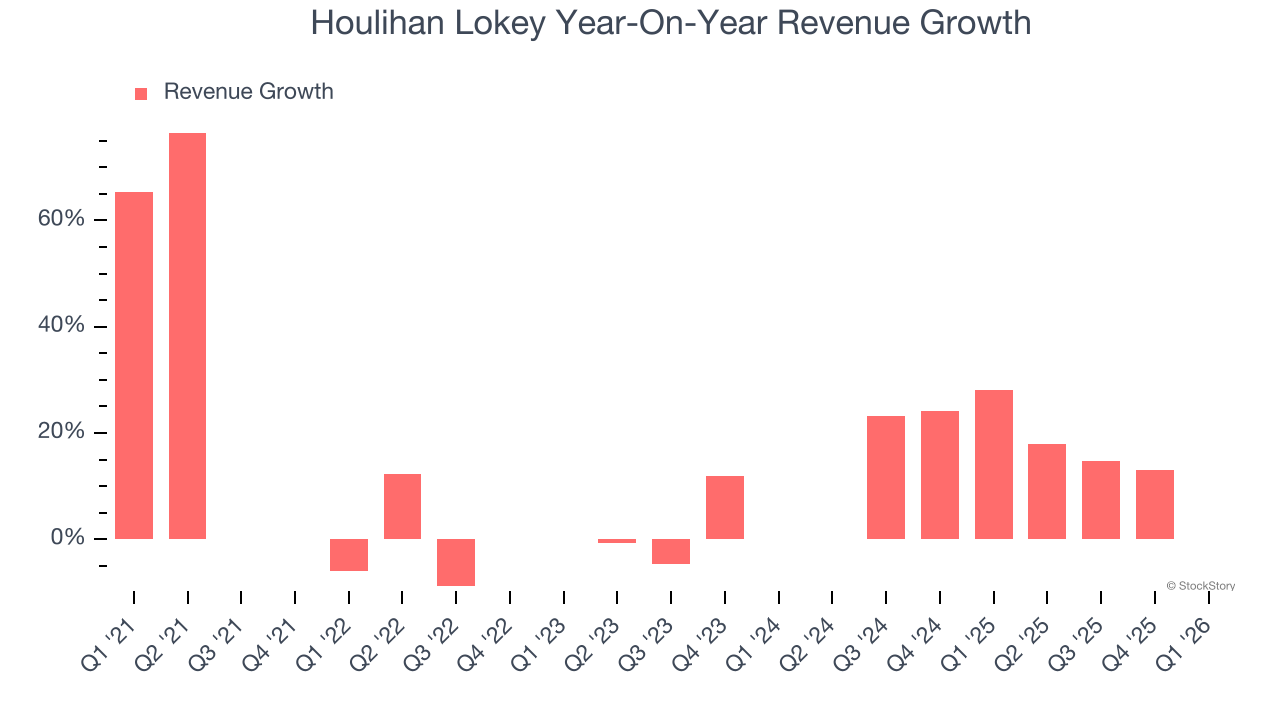

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Houlihan Lokey’s annualized revenue growth of 16.9% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Houlihan Lokey missed Wall Street’s estimates and reported a rather uninspiring 4.6% year-on-year revenue decline, generating $635.6 million of revenue.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Key Takeaways from Houlihan Lokey’s Q1 Results

We struggled to find many positives in these results. Its EBITDA missed and its revenue fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 1.6% to $144.82 immediately following the results.

Houlihan Lokey didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).