What a time it’s been for agilon health. In the past six months alone, the company’s stock price has increased by a massive 538%, setting a new 52-week high of $117.62 per share. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy agilon health, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is agilon health Not Exciting?

We’re glad investors have benefited from the price increase, but we’re swiping left on agilon health for now. Here are three reasons why AGL doesn’t excite us, plus one stock we’d rather own.

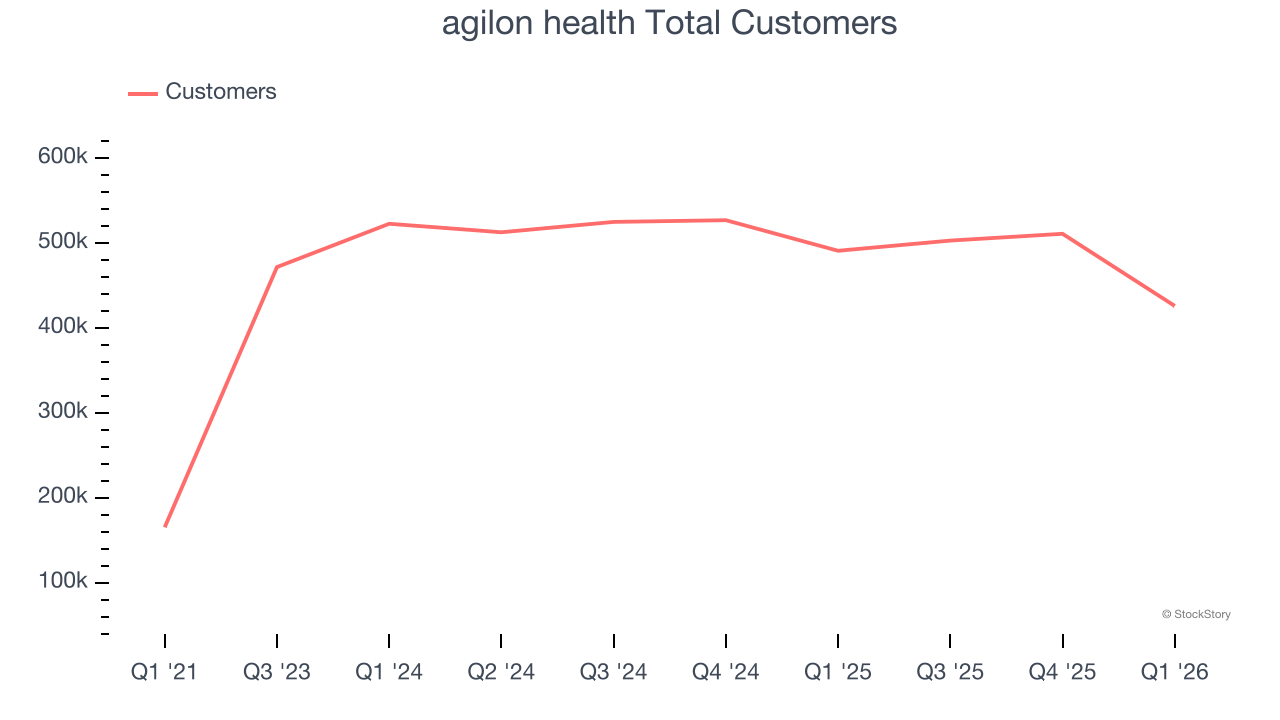

1. Declining Customer Base Reflects Product and Sales Weakness

Revenue growth can be broken down into the number of customers and the average spend per customer. Both are important because an increasing customer base leads to more upselling opportunities while the revenue per customer shows how successful a company was in executing its upselling strategy.

agilon health’s total customers came in at 426,000 in the latest quarter, and over the last two years, their count averaged 3.1% year-on-year declines. This performance was underwhelming and shows the company lost deals and renewals. It also suggests there may be increasing competition or market saturation.

2. Projected Revenue Growth Shows Limited Upside

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect agilon health’s revenue to stall, a deceleration versus its 34.1% annualized growth for the past five years. This projection is underwhelming and suggests its products and services will see some demand headwinds.

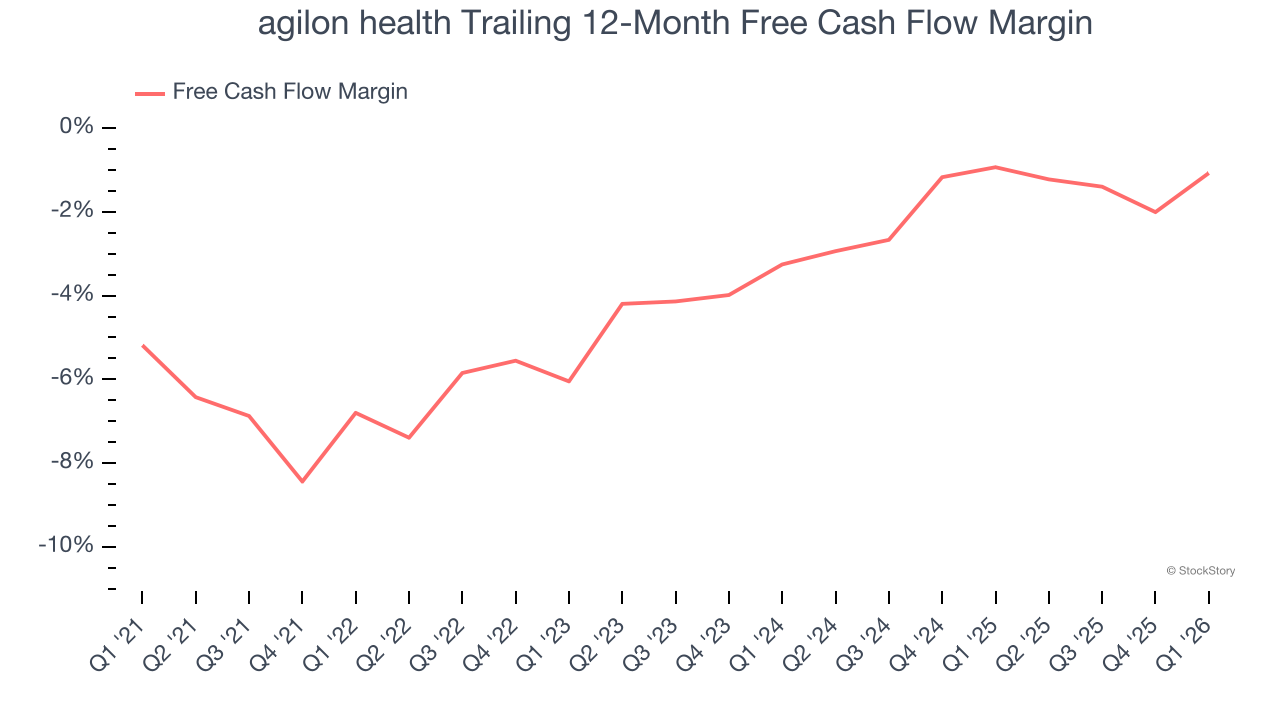

3. Cash Burn Ignites Concerns

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

While agilon health posted positive free cash flow this quarter, the broader story hasn’t been so clean. agilon health’s demanding reinvestments have consumed many resources over the last five years, contributing to an average free cash flow margin of negative 2.8%. This means it lit $2.76 of cash on fire for every $100 in revenue.

Final Judgment

agilon health isn’t a terrible business, but it doesn’t pass our quality test. After the recent rally, the stock trades at 97.9× forward EV-to-EBITDA (or $117.62 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We’re pretty confident there are superior stocks to buy right now. We’d recommend looking at the most dominant software business in the world.

High-Quality Stocks for All Market Conditions

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.