New York-based vertically integrated hydrogen-based power company Plug Power (PLUG) is slated to report its results for Q1 2026 today after the market closes. Expectations around the yet-to-be-profitable company are for a loss per share of $0.10 and revenues of $139.8 million.

In the same quarter a year ago, Plug Power had revenues of $133.7 million and a loss per share of $0.21. With this context, for a company that has been in existence for about three decades now, even if the Street expectations are met, it would not be much of an achievement.

Valued at a market cap of $4.35 billion, PLUG stock is up 76.9% year-to-date (YTD).

Q4 Lowdown

As we gear up for Plug's Q1 print, a look in the rearview mirror at the Q4 numbers is warranted.

In Q4 2025, Plug had a mixed showing. While revenues of $225.2 million marked a yearly growth of 17.6%, losses narrowed by more than 57% in the same period to come in at $0.21 per share. Although the revenues surpassed estimates, the loss per share came in higher than the consensus estimate of a loss of $0.10 per share.

Cash from operations continued to remain negative, although the quantum of the same was less. Net cash used in operating activities was at $535.8 million in 2025, lower than the $728.6 million reported in the year-ago period. Overall, Plug exited 2025 with a cash balance of $368.5 million, much higher than its short-term debt levels of $78.7 million.

Notably, the company has also brought in new leadership in the form of Jose Luis Crespo, who assumed the CEO chair on March 2 and has been with Plug since 2014. Serving in the capacities of President and Chief Revenue Officer, during Crespo's tenure, Plug's annual revenues grew from about $20 million in 2014 to more than $700 million in 2025. Moreover, Crespo has played a pivotal role in strengthening relations with key customers like Amazon (AMZN), Walmart (WMT), and Home Depot (HD).

Following the appointment, Crespo said, “I’m honored to have the opportunity to lead Plug Power at this pivotal stage of growth and transformation. In 2026, we will continue executing with discipline, driving margin improvement, and delivering exceptional outcomes for our customers. By leveraging our strong commercial foundation, advancing cost-efficiency initiatives, and capitalizing on our more than $8 billion global sales funnel, we are converting operational momentum into sustainable financial performance. Our targets remain consistent in achieving positive EBITDAS in Q4 of 2026, positive operating income by the end of 2027, and full profitability by the end of 2028, while still growing the Company substantially.”

What Can Jolt Plug To Power?

My last analysis on Plug was quite a while ago. Still, even amid heightened energy demand for AI, the stock is up 57.8% since then. Moreover, how a company insider like Crespo will steer the company will also be of much intrigue as much of the issues highlighted in my piece happened under his watch, although his first comments raised optimism with clear targets.

Now, for Q1, analysts and investors are closely watching whether the company can deliver a second consecutive quarter of positive gross margins. That would be a meaningful milestone for a company that has spent years burning cash at an uncomfortable pace. Plug Power burned through roughly $535.8 million in cash last year, and while that figure was down 26.5%, entering 2026 with just under $370 million in unrestricted liquidity does not inspire a great deal of comfort. So the Street wants to see that margin improvement is not a one-quarter anomaly but something that is actually sticking.

Beyond margins, much of the investor community will be listening closely for updates on Project Quantum Leap, the internal restructuring program aimed at achieving positive EBITDA by the end of 2026, positive operating income by the end of 2027, and full profitability by 2028. CEO Jose Luis Crespo has described the margin improvement as "not accidental" and pointed to an "inflection point" for the company, and the Street will want specifics around cost savings translating into real numbers rather than forward guidance language.

In terms of products, all eyes will be on Plug's GenEco electrolyzer platform. In 2025, the company shipped more than 185 MW of GenEco electrolyzers, representing roughly 203% year-over-year (YOY) growth compared to 2024, pushing total cumulative electrolyzer shipments past 317 MW across more than 70 units, with deployments now active on every continent except Antarctica.

Notably, the industrial use cases are broadening fast.

GenEco uses proton exchange membrane technology and is designed for applications ranging from ammonia production to refining and green steel, offering higher purity hydrogen and better performance under fluctuating power compared to alkaline systems. The deal pipeline reflects that momentum. In April 2026, Plug was awarded the front-end engineering design contract to supply a 275 MW GenEco system for Hy2gen Canada's "Courant" project in Quebec, one of the largest electrolyzer project awards in the company's history. Earlier in January 2026, Plug completed the installation of all 100 MW of GenEco electrolyzer units at Galp's Sines Refinery in Portugal, a project expected to produce up to 15,000 tons of renewable hydrogen per year once commissioned.

Additionally, the second frontier worth watching is data centers. In November 2025, Plug signed a non-binding letter of intent to monetize electricity rights in New York and one other location and collaborate with a U.S. data center developer on auxiliary and backup power solutions using its GenSure fuel cell technology. This is a vital development as AI-driven data center expansion is pushing power demand to levels that diesel generators simply cannot meet cleanly or reliably. Plug had already been collaborating with three major data center operators to plan initial deployments and test its hydrogen fuel cell backup systems.

Thus, with GenEco at an industrial scale globally and GenSure in the data center space, Plug has two credible paths toward the kind of revenue diversification that could actually make the 2028 profitability target feel achievable rather than aspirational. Now, its just a matter of execution.

Analyst Opinion

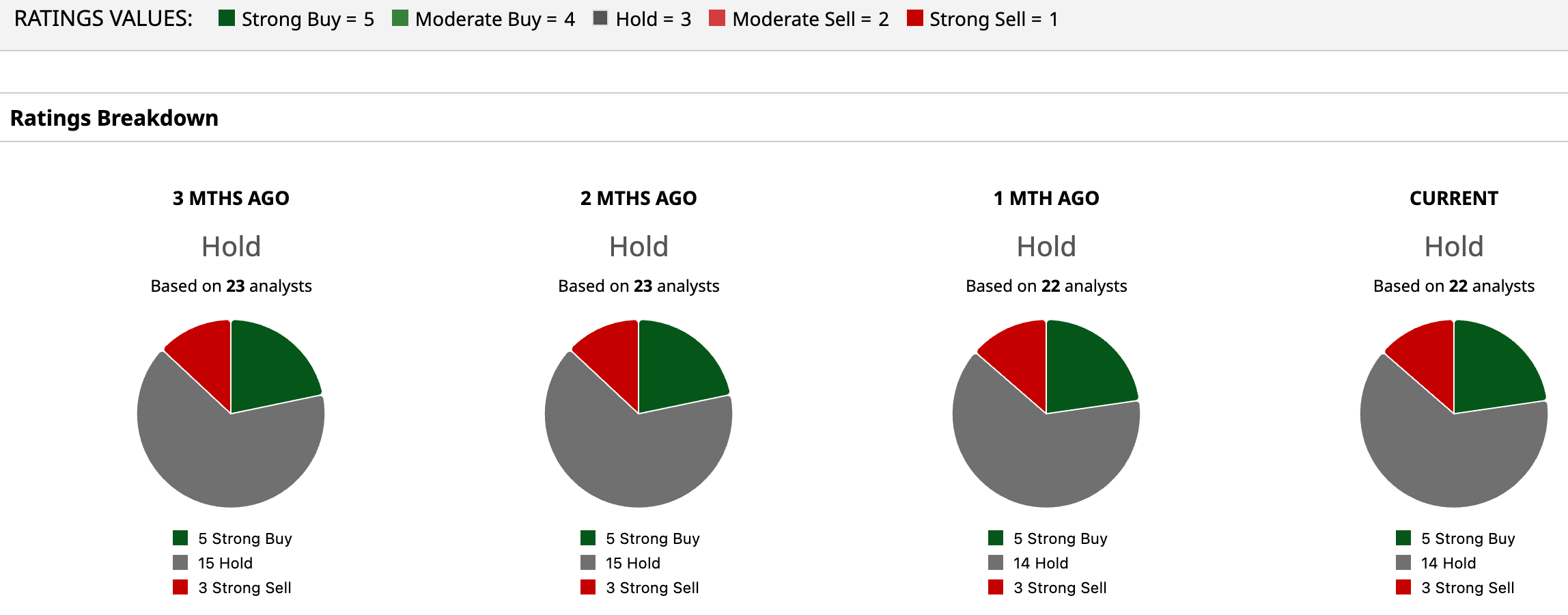

Considering this, analysts have deemed PLUG as a “Hold” with a mean target price that has already been surpassed. The high target price of $7 indicates an upside potential of 96.6% from current levels. Out of 22 analysts covering the stock, five have a “Strong Buy” rating, 14 have a “Hold” rating, and three have a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- After Major Layoffs, Block Stock Is Staging a Turnaround. CEO Jack Dorsey Says AI Is Leading the Way.

- This Analyst Just Raised the Price Target on Coherent Stock by 50%. What to Know.

- CoreWeave Stock Falls as the AI Growth Story Slows Down

- A Major Catalyst for AAPL Stock Is Just a Month Away: Apple Is a ‘Sleep Tech Giant’ Says Wedbush