The traditional appeal of dividend investing — steady income and lower volatility — is being challenged by a 2026 market that prizes price momentum over payout ratios. This has been going on for about 10 years. I know because I lived through it as a dividend investor.

About a decade ago, based on research I did with my then-college-aged son (now a CFA), we created Yield At a Reasonable Price (YARP)®, a factor that helps investors research dividend-paying stocks by analyzing their yield history. That’s a short-cut definition, but suffice it to say, around that time, dividend investing started to change. And not in a way that made it more attractive.

Frankly, we saw it coming in the form of relatively few high-yield stocks making the grade as long-term investments. This was the period leading up to the pandemic in 2020, and that was the final straw for the outperformance potential of yield stocks over low/no yield equities. And while I’m looking carefully to see if and when dividend investing will return to its former glory days, here’s the rub: even when they do, they will still likely take a back seat to growth stocks. Particularly, artificial intelligence (AI) and technology names.

This is NOT a complaint. In fact, I still believe that dividend yield is a useful contributor to total returns. What I rebel against is the obsession with yield. Because a generation of investors has learned to either ignore it or misunderstand it. Or, perhaps both.

We can’t solve that hurdle in one article. But we can look at the most recent evidence of how yield investing, at least concerning U.S. large-cap stocks, is still very much Scottie Pippen to Michael Jordan, if you get the reference to the NBA championship run of the Chicago Bulls years ago.

In fact, Jordan was recently asked how he thought those Bulls teams would do against today’s NBA teams. His response: “We’d lose by a few points.” When reporters followed up and asked, “Don’t you think you could beat them?” Jordan’s response: “Well, most of us are around 60 years old now.”

What’s the analogy to dividend investing? It hasn’t lost its skills entirely. However, a new generation of “players” has come along. And just as a bunch of 60-year-old former NBA players won’t compete with 20-somethings playing in the league right now, so too will dividend stalwarts — the Dividend Kings and Aristocrats — not likely return to their former market leadership.

Don’t be sad about it. I’m not. I’m just realistic, just as I was back when I ran a dividend fund and created a trademarked dividend factor a decade ago. While dividend exchange-traded funds (ETFs) still have some merit as investment holdings, the best use I find for them is for stock screening and selection. That is, using them as a scouting list to find single stocks. After all, those ETFs are typically constructed based on dividend indexes, essentially market cap or fundamental screens. So it cuts a step in the process, assuming you like the nature of the screen and index applied.

What 5 Dividend ETFs Are Saying About Dividend Investing

A look at the current landscape of popular dividend ETFs shows a sector that has effectively split into two camps: those chasing dividend growth as a proxy for tech-lite capital appreciation, and those offering high yields that come with a significant side of price risk.

That latter issue has been the killer for yield stocks for a decade now. Too many weak performers beyond the dividend, which is really just getting back money. Remember that dividends, when paid, reduce the price of the ETF or stock distributing them.

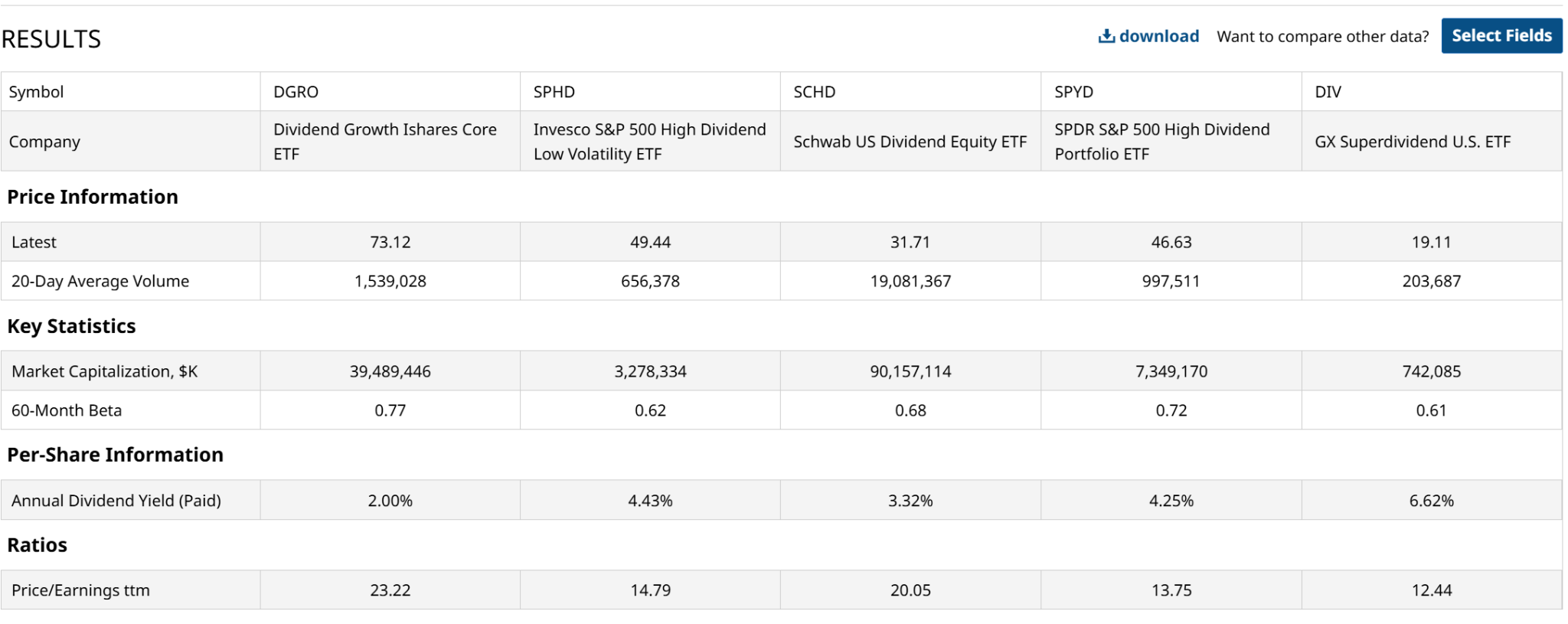

This table is simply a quick snapshot of five of many I’ve followed over the years. One thing I notice is that their five-year betas are fairly clustered, though the iShares Core Dividend Growth ETF (DGRO) is clearly and logically the most aggressive. And thus, easily the most successful in recent years. The Global X Superdividend U.S. ETF (DIV), on the other hand, pays a much higher dividend yield, and the SPDR S&P 500 High Dividend Portfolio ETF (SPYD) and the Invesco S&P 500 High Dividend Low Volatility ETF (SPHD) also emphasize yield more than price gains. The Schwab U.S. Dividend Equity ETF (SCHD) is somewhere in the middle.

In particular, DGRO exemplifies the shift from income to price growth. With an annual dividend yield of just 2%, DGRO is no longer an income play in the traditional sense. Instead, its price-to-earnings (P/E) ratio of 23x suggests it is behaving more like a core growth fund.

In this environment, dividend growth has become a branding exercise for high-quality stocks that are participating in the broader market rally, bringing along with it a level of price volatility that dividend purists might find jarring. There are even mega-cap companies that pay a puny dividend, just to qualify to be in a fund that targets dividend-paying stocks.

Look at DGRO’s three biggest holdings. It holds 400+ stocks, essentially the S&P 500 minus the zero-yield names. But it is top-heavy and yield-light, no different than an S&P 500 Index ($SPX) fund.

The best performers here (DGRO and SCHD) have seen their P/E ratios expand consistently, while the other three yield more, are better value on paper, but lack the interest of investors. There’s no sign of that changing. Not with AI, memory, and data centers hogging the market narrative.

At the other end of the spectrum, DIV offers a staggering 6.6% yield, but the trade-off is clear in the fundamentals. Despite the low beta, DIV carries a massive discount in valuation, trading at a P/E of just 12.4. In a market dominated by liquidity flows into tech and infrastructure, these high-yielding vehicles are often left behind, acting more like value traps than stable harbor investments. The high yield is frequently a function of a stagnant or declining share price rather than organic cash flow growth.

The Bottom Line

Yield doesn’t matter much anymore because the annual yield spread between a 2% yield and a 4% yield is easily swallowed by a single day of price volatility. For the modern investor, the choice isn't about the payout. It is now about the P/E and the beta.

As dividend growth funds increasingly mirror the volatility of the S&P 500, the "safety" traditionally associated with these ETFs is becoming a historical footnote. Nowadays, you aren't buying a dividend. You're buying a factor, and that factor is currently under the thumb of broader market momentum.

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob's written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Yield Is No Longer King: What These 5 Dividend ETFs Are Telling Investors

- Berkshire Hathaway Just Upped Its Stake in Sumitomo Stock. Greg Abel Says It’s Holding for the Long Term.

- A Major Catalyst for AAPL Stock Is Just a Month Away: Apple Is a ‘Sleep Tech Giant’ Says Wedbush

- Shake Shack Stock Looks Ugly After Earnings. Burger Eaters Were Opting for Value Instead