Portsmouth-based Iron Mountain Incorporated (IRM) is a global leader in information management services, trusted by more than 240,000 customers in 61 countries. The company has a market cap of $37.5 billion and offers solutions for information management, digital transformation, information security, data centers, and asset lifecycle management (ALM).

Shares of the company have rallied the broader market over the past year and in 2026. IRM stock has grown 29.5% over the past 52 weeks and 52% on a YTD basis. In comparison, the S&P 500 Index ($SPX) has returned 26.5% over the past year and risen 8.8% in 2026.

Narrowing the focus, IRM has also outperformed the State Street Real Estate Select Sector SPDR ETF (XLRE), which rose 7.6% over the past 52 weeks and its 9.6% rise this year.

On Apr. 30, IRM stock rose 10% following the release of its Q1 2026 earnings. The company’s revenue rose 21.6% from the prior year’s quarter to $1.9 billion, driven by an 12.6% increase in storage rental revenue and a 27.6% increase in service revenue. Moreover, its AFFO per share for the quarter also came in at $1.43. The company now expects its revenue to be in the range of $7.8 to $7.9 billion for the full fiscal year.

For the current year ending in December, analysts expect IRM’s EPS to increase 154.7% year over year to $5.40. Moreover, the company has surpassed analysts’ consensus estimates in each of the past four quarters.

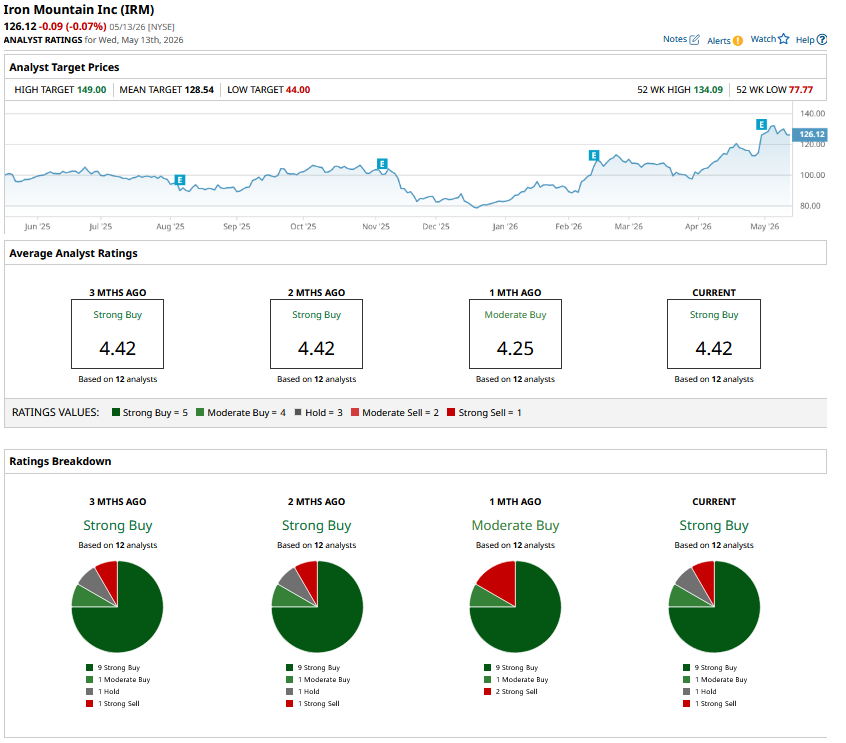

Among the 12 analysts covering the stock, the consensus rating is a “Strong Buy.” That’s based on nine “Strong Buy” ratings, one “Moderate Buy,” one “Hold,” and one “Strong Sell” rating.

The configuration has remained unchanged over the past month.

On May 1, JP Morgan analyst Andrew Steinerman maintained an “Overweight” rating on Iron Mountain and raised its price target from $121 to $138.

IRM’s mean price target of $128.54 indicates a premium of 1.9% from the current market prices. Its Street-high target of $149 suggests a robust 18.1% upside potential from current price levels.

On the date of publication, Aritra Gangopadhyay did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Microsoft Stock Is a Buy as Its AI Business’ Annual Revenue Run Rate Swells

- Nebius Group Stock Soars 16% as AI Revenue Growth Hits 684%. Its Meta Deal Changes Everything.

- 2 Unusually Active Shopify Stock Calls Work Out to 1 Interesting Strategy

- The AI Boom Has a Power Problem. This Stock May Be the Biggest Winner.