Valued at $91.8 billion by market cap, Bank of New York Mellon Corporation (BK) is one of the world’s largest financial services and asset servicing companies. Headquartered in New York City, the company specializes in investment management, custody banking, wealth management, treasury services, and financial market infrastructure for institutions, corporations, and high-net-worth individuals.

The banking giant has significantly outpaced the broader market over the past year. BNY stock has soared 53.5% over the past 52 weeks and 16.3% on a YTD basis, compared to the S&P 500 Index’s ($SPX) 26.5% gains over the past year and 8.8% returns on a YTD basis.

Narrowing the focus, BNY has also outperformed the industry-focused SPDR S&P Bank ETF’s (KBE) 11.8% rise over the past year and 1.8% rally in 2026.

The Bank of New York Mellon Corporation delivered a strong Q1 2026 result on Apr. 16, with record revenue rising 13% year over year to $5.41 billion and EPS surging 42% to $2.25, both comfortably ahead of analyst expectations. Growth was broad-based across its Securities Services and Market & Wealth Services businesses, supported by higher client activity, stronger market values, rising net interest income, and a sharp increase in foreign exchange revenue. Assets under custody and administration climbed to $59.4 trillion, while assets under management reached $2.1 trillion. Investors were impressed by the result and pushed the stock up 2.2% post-announcement.

For the current year ending in December, analysts expect Bk to deliver an adjusted EPS of $8.78, up 17.1% year over year. The company has a robust earnings surprise history. It has surpassed the Street’s bottom-line estimates in each of the past four quarters.

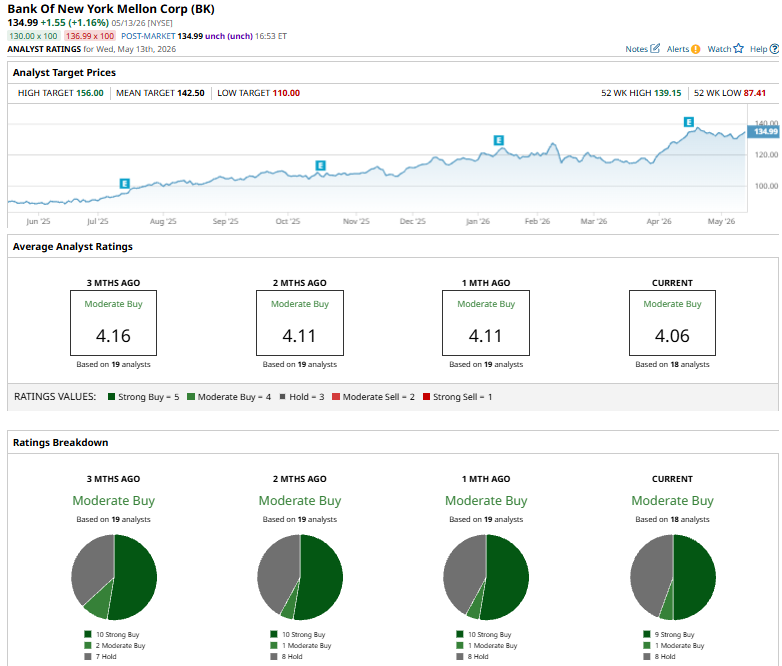

Among the 18 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on nine “Strong Buys,” one “Moderate Buy,” and eight “Holds.”

This configuration is bearish than one month ago, when ten analysts gave “Strong Buy” recommendations.

On Apr. 7, analyst Vivek Juneja maintained an “Overweight” rating on The Bank of New York Mellon and raised the stock’s price target to $130.50 from $128.50, reflecting increased confidence in the company’s outlook and growth potential.

BNY’s mean price target of $142.50 represents a modest 5.6% premium to current price levels. The Street-high target of $156 implies an upswing potential of 15.6%.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart