With a market cap of $87.4 billion, Waste Management, Inc. (WM) is North America’s largest provider of waste collection, recycling, and environmental services. Headquartered in Houston, Texas, the company serves residential, commercial, industrial, and municipal customers across the United States and Canada.

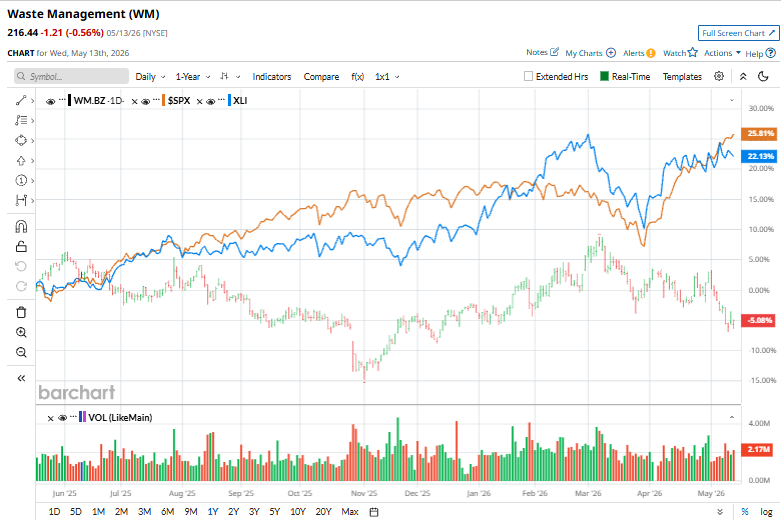

Shares of the company have lagged behind the broader market over the past 52 weeks. WM stock has declined 2.7% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 26.5%. Moreover, shares of the company are down 1.5% on a YTD basis, compared to SPX’s 8.8% gain.

Focusing more closely, shares of the garbage and recycling hauler have underperformed the State Street Industrial Select Sector SPDR Fund’s (XLI) 22.9% rise over the past 52 weeks and an 11.9% YTD return.

On Apr. 28, Waste Management posted its FY2026 Q1 results, and its shares jumped 1.3% in the next trading session. Revenue increased 3.5% year over year to $6.23 billion, and adjusted earnings per share came in at $1.81, up 8.4% from the prior-year quarter and ahead of analyst expectations. Its adjusted operating EBITDA rose 5.9% to $1.85 billion, with margins expanding 70 basis points to 29.8%. The company’s core Collection and Disposal segment remained the primary growth driver, benefiting from strong pricing execution and favorable price-to-cost spreads.

For the fiscal year ending in December 2026, analysts expect Waste Management’s adjusted EPS to grow 8.7% year over year to $8.15. The company's earnings surprise history is mixed. It topped the consensus estimates in two of the last four quarters while missing on two other occasions.

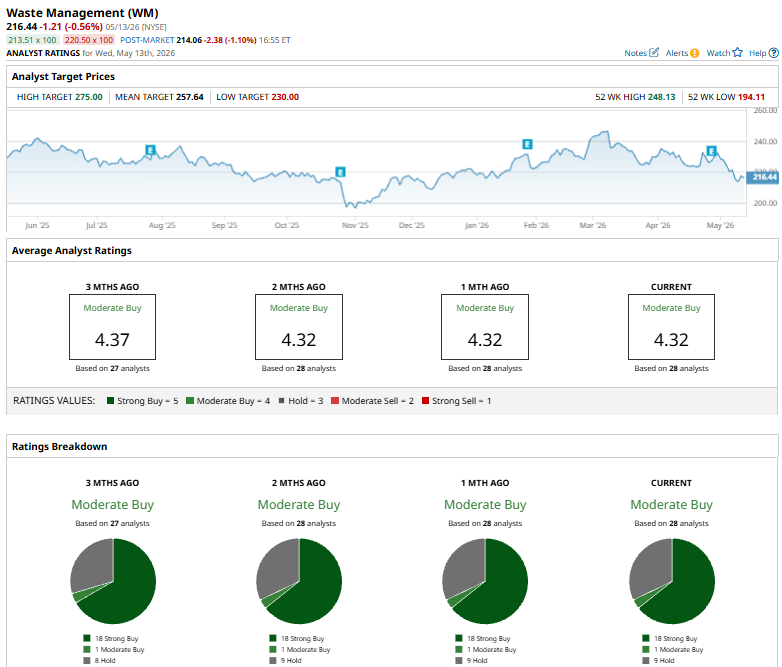

Among the 28 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on 18 “Strong Buy” ratings, one “Moderate Buy,” and nine “Holds.”

On Apr. 29, TD Cowen raised its price target on Waste Management to $275 from $270 while maintaining a “Buy” rating, reflecting continued confidence in the company’s long-term outlook. Analysts also said management remains confident in its 2026 outlook, viewing the company’s guidance as reasonable.

The mean price target of $257.64 represents a 19% premium to WM’s current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart