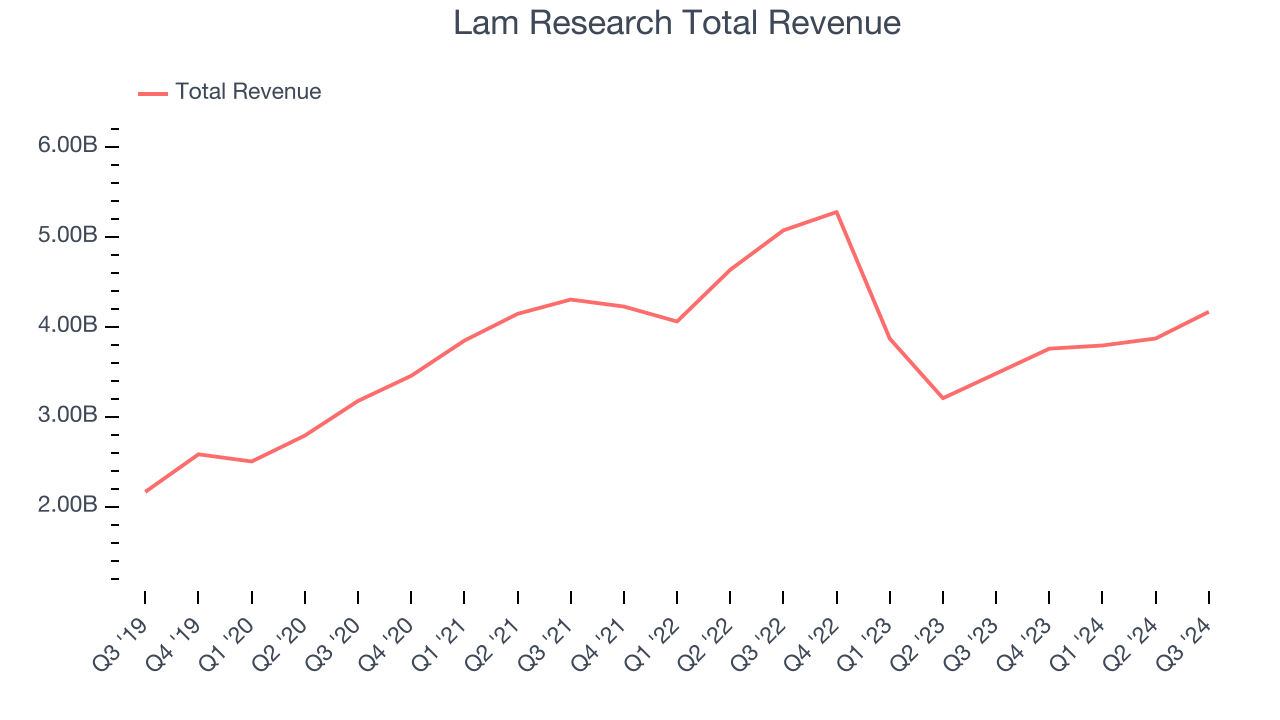

Semiconductor equipment maker Lam Research (NASDAQ: LRCX) reported Q3 CY2024 results beating Wall Street’s revenue expectations, with sales up 19.7% year on year to $4.17 billion. Guidance for next quarter’s revenue was also better than expected at $4.3 billion at the midpoint, 1.3% above analysts’ estimates. Its non-GAAP profit of $0.86 per share was also 6.5% above analysts’ consensus estimates.

Is now the time to buy Lam Research? Find out by accessing our full research report, it’s free.

Lam Research (LRCX) Q3 CY2024 Highlights:

- Revenue: $4.17 billion vs analyst estimates of $4.06 billion (2.7% beat)

- Adjusted EPS: $0.86 vs analyst estimates of $0.81 (6.5% beat)

- Adjusted Operating Income: $1.29 billion vs analyst estimates of $1.21 billion (6.8% beat)

- Revenue Guidance for Q4 CY2024 is $4.3 billion at the midpoint, above analyst estimates of $4.25 billion

- Adjusted EPS guidance for Q4 CY2024 is $0.87 at the midpoint, above analyst estimates of $0.85

- Gross Margin (GAAP): 48%, in line with the same quarter last year

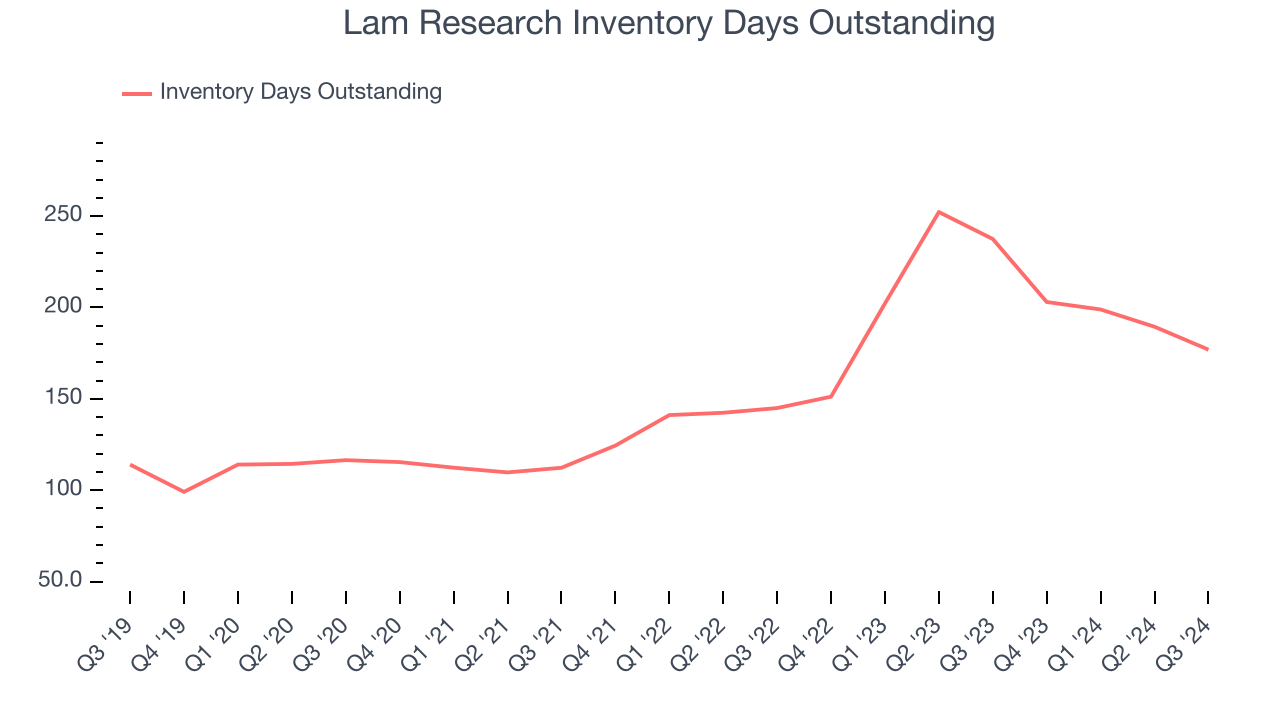

- Inventory Days Outstanding: 177, down from 189 in the previous quarter

- Operating Margin: 30.3%, in line with the same quarter last year

- Free Cash Flow Margin: 35%, up from 25.1% in the same quarter last year

- Market Capitalization: $94.62 billion

"With continued strong execution, Lam delivered financial performance ahead of expectations," said Tim Archer, Lam Research's President and Chief Executive Officer.

Company Overview

Founded in 1980 by David Lam, the man who pioneered semiconductor etching technology, Lam Research (NASDAQ: LRCX) is one of the leading providers of wafer fabrication equipment used to make semiconductors.

Semiconductor Manufacturing

The semiconductor industry is driven by demand for advanced electronic products like smartphones, PCs, servers, and data storage. The need for technologies like artificial intelligence, 5G networks, and smart cars is also creating the next wave of growth for the industry. Keeping up with this dynamism requires new tools that can design, fabricate, and test chips at ever smaller sizes and more complex architectures, creating a dire need for semiconductor capital manufacturing equipment.

Sales Growth

A company’s long-term performance is an indicator of its overall business quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for multiple years. Thankfully, Lam Research’s 10.4% annualized revenue growth over the last five years was solid. This is encouraging because it shows Lam Research was more successful in expanding than most semiconductor companies.

Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions (which can sometimes offer opportune times to buy).

We at StockStory place the most emphasis on long-term growth, but within semiconductors, a half-decade historical view may miss new demand cycles or industry trends like AI. Lam Research’s recent history marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 6.9% over the last two years.

This quarter, Lam Research reported year-on-year revenue growth of 19.7%, and its $4.17 billion of revenue exceeded Wall Street’s estimates by 2.7%. Management is currently guiding for a 14.4% year-on-year increase next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 16.1% over the next 12 months, an acceleration versus the last two years. This projection is noteworthy and indicates the market thinks its newer products and services will spur faster growth.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Lam Research’s DIO came in at 177, which is 24 days above its five-year average. These numbers suggest that despite the recent decrease, the company’s inventory levels are higher than what we’ve seen in the past.

Key Takeaways from Lam Research’s Q3 Results

We were impressed that Lam Research beat analysts’ revenue and EPS expectations this quarter. Next quarter's guidance for revenue and EPS were also both ahead. Overall, we think this was a solid quarter. The stock traded up 5.5% to $77.05 immediately following the results.

Lam Research may have had a good quarter, but does that mean you should invest right now?When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.