Haemonetics has gotten torched over the last six months - since October 2024, its stock price has dropped 20.1% to $63.39 per share. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Haemonetics, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Even though the stock has become cheaper, we're sitting this one out for now. Here are three reasons why we avoid HAE and a stock we'd rather own.

Why Is Haemonetics Not Exciting?

With roots dating back to 1971 and a mission to improve blood-related healthcare, Haemonetics (NYSE: HAE) provides specialized medical devices and software for blood collection, processing, and management across plasma centers, blood banks, and hospitals.

1. Long-Term Revenue Growth Disappoints

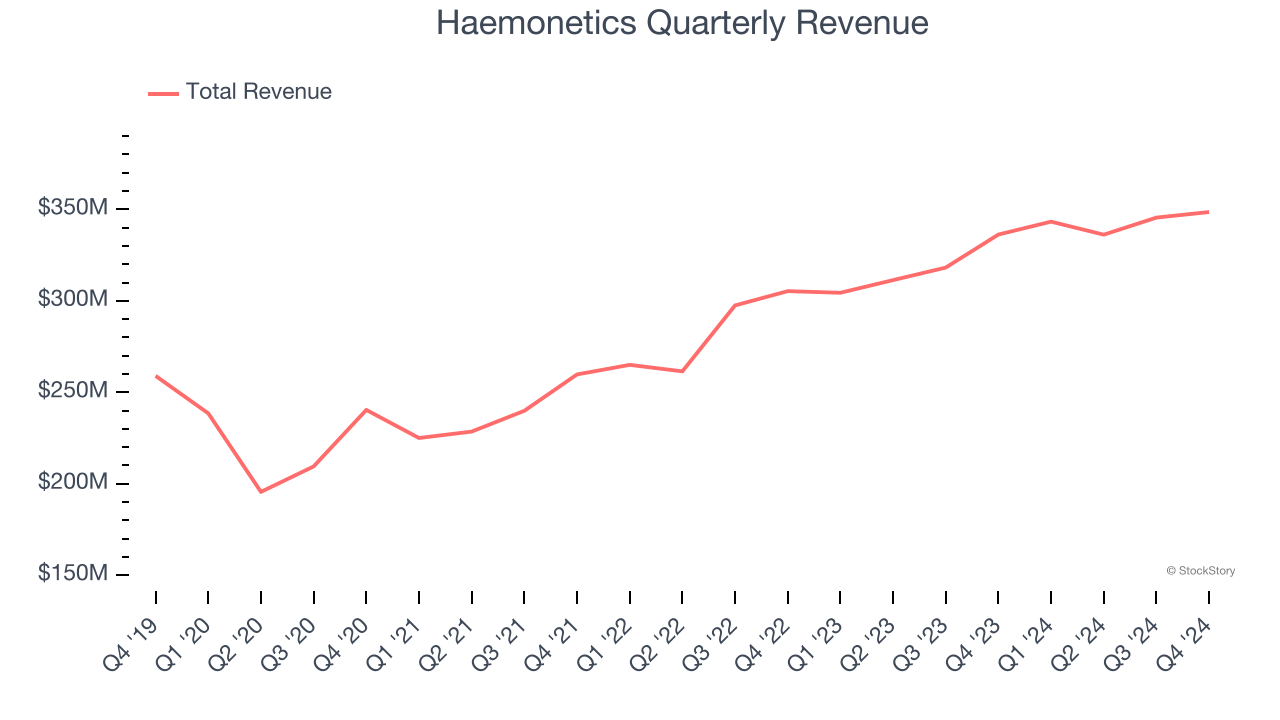

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Haemonetics grew its sales at a mediocre 6.6% compounded annual growth rate. This was below our standard for the healthcare sector.

2. Fewer Distribution Channels Limit its Ceiling

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $1.37 billion in revenue over the past 12 months, Haemonetics is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

3. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Haemonetics’s revenue to drop by 4.4%, a decrease from its 10.3% annualized growth for the past two years. This projection is underwhelming and implies its products and services will face some demand challenges.

Final Judgment

Haemonetics isn’t a terrible business, but it doesn’t pass our bar. Following the recent decline, the stock trades at 12.4× forward price-to-earnings (or $63.39 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're pretty confident there are superior stocks to buy right now. We’d recommend looking at one of our top digital advertising picks.

Stocks We Would Buy Instead of Haemonetics

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.