Since December 2025, AdaptHealth has been in a holding pattern, posting a small loss of 3% while floating around $9.94. The stock also fell short of the S&P 500’s 6.9% gain during that period.

Is now the time to buy AdaptHealth, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is AdaptHealth Not Exciting?

We’re swiping left on AdaptHealth for now. Here are three reasons we avoid AHCO, plus one stock we’d rather own.

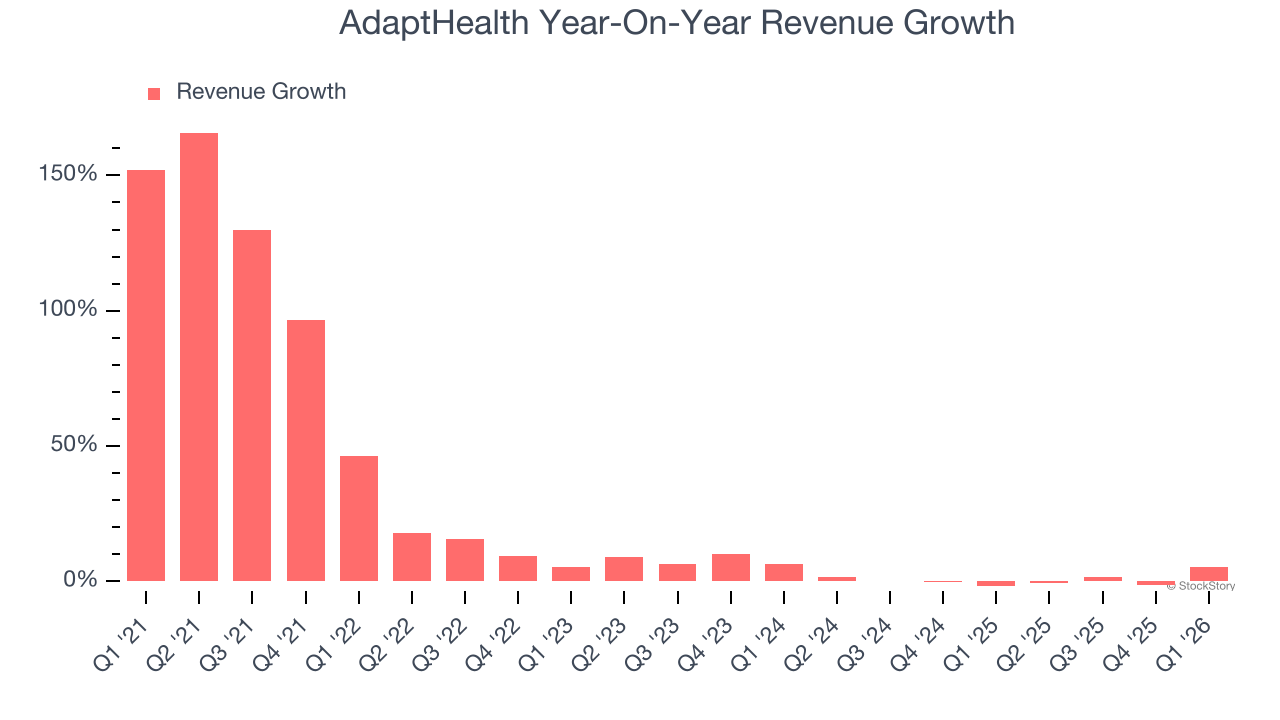

1. Revenue Growth Flatlining

We at StockStory place the most emphasis on long-term growth, but within healthcare, a stretched historical view may miss recent innovations or disruptive industry trends. AdaptHealth’s recent performance shows its demand has slowed significantly as its revenue was flat over the last two years.

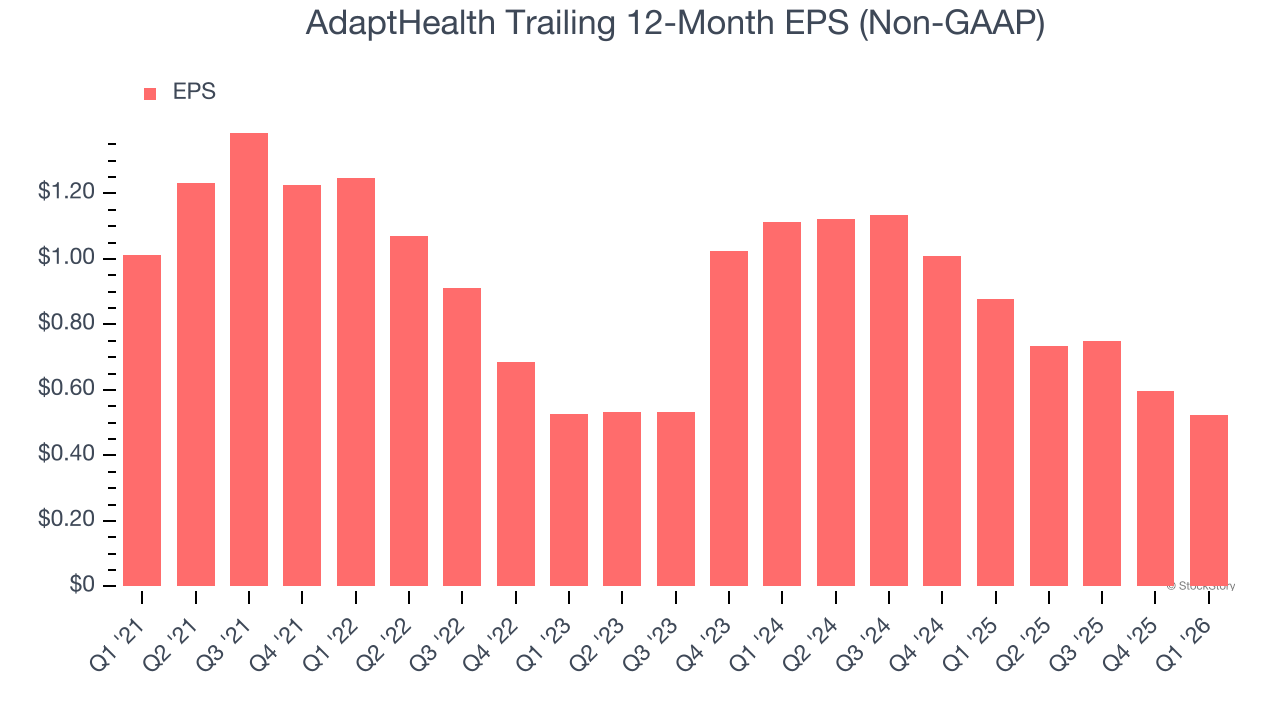

2. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for AdaptHealth, its EPS declined by 12.4% annually over the last five years while its revenue grew by 19.3%. This tells us the company became less profitable on a per-share basis as it expanded.

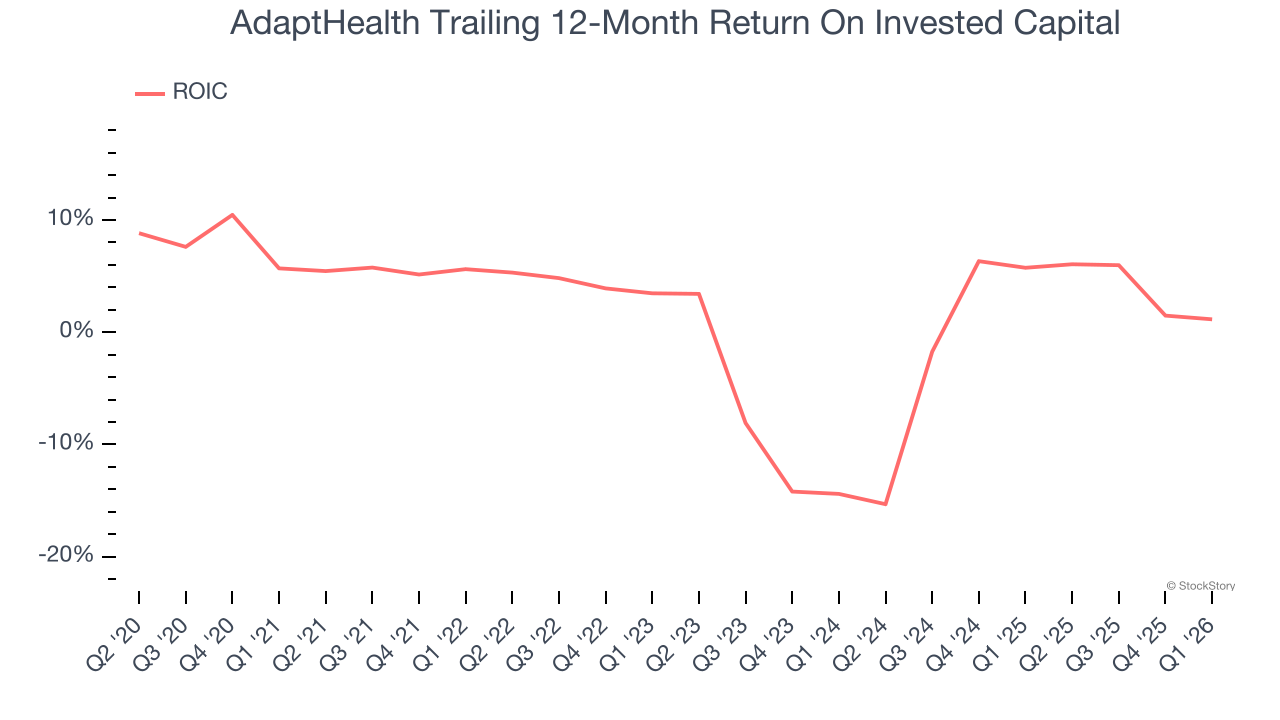

3. Previous Growth Initiatives Haven’t Paid Off Yet

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

AdaptHealth historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 0.3%, lower than the typical cost of capital (how much it costs to raise money) for healthcare companies.

Final Judgment

AdaptHealth isn’t a terrible business, but it isn’t one of our picks. With its shares underperforming the market lately, the stock trades at 10.5× forward P/E (or $9.94 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We’re pretty confident there are superior stocks to buy right now. We’d recommend looking at the most dominant software business in the world.

Stocks We Like More Than AdaptHealth

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.