Danaher has gotten torched over the last six months - since December 2025, its stock price has dropped 21.2% to $178.42 per share. This may have investors wondering how to approach the situation.

Is now the time to buy Danaher, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is Danaher Not Exciting?

Even though the stock has become cheaper, we’re cautious about Danaher. Here are three reasons why DHR doesn’t excite us, plus one stock we’d rather own.

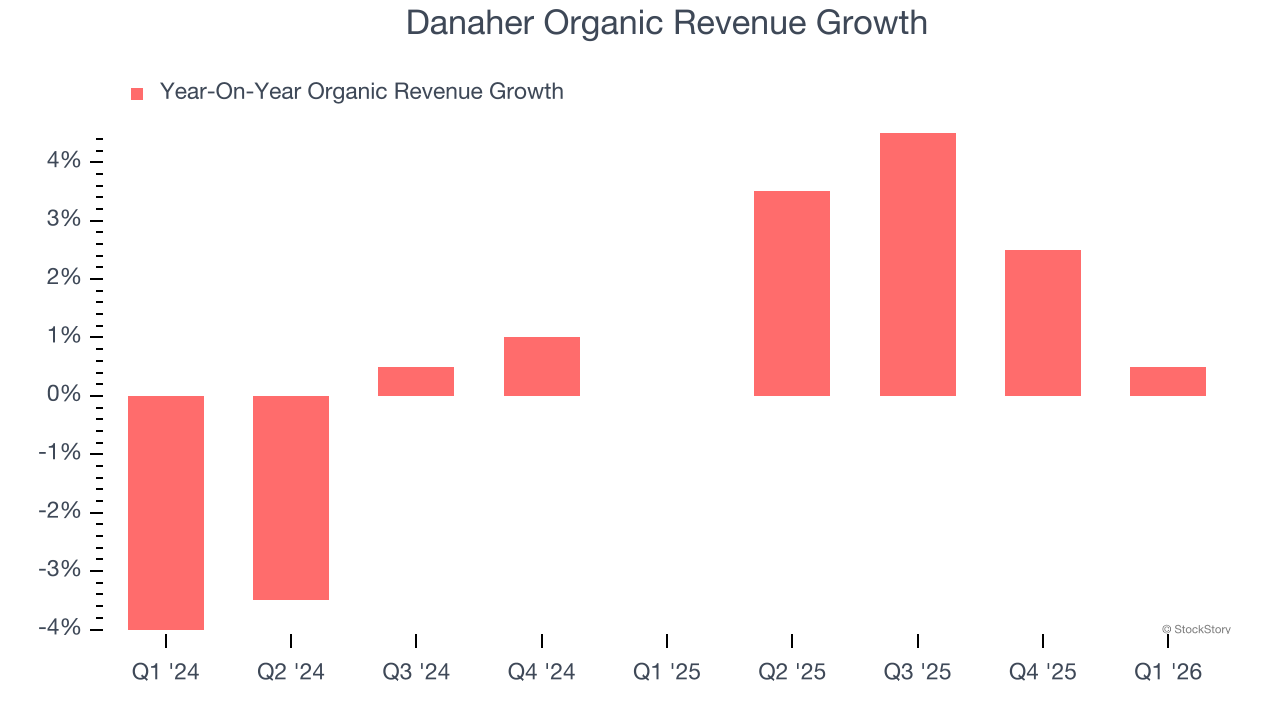

1. Slow Organic Growth Suggests Waning Demand In Core Business

We can better understand Research Tools & Consumables companies by analyzing their organic revenue. This metric gives visibility into Danaher’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Danaher’s organic revenue averaged 1.1% year-on-year growth. This performance was underwhelming and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

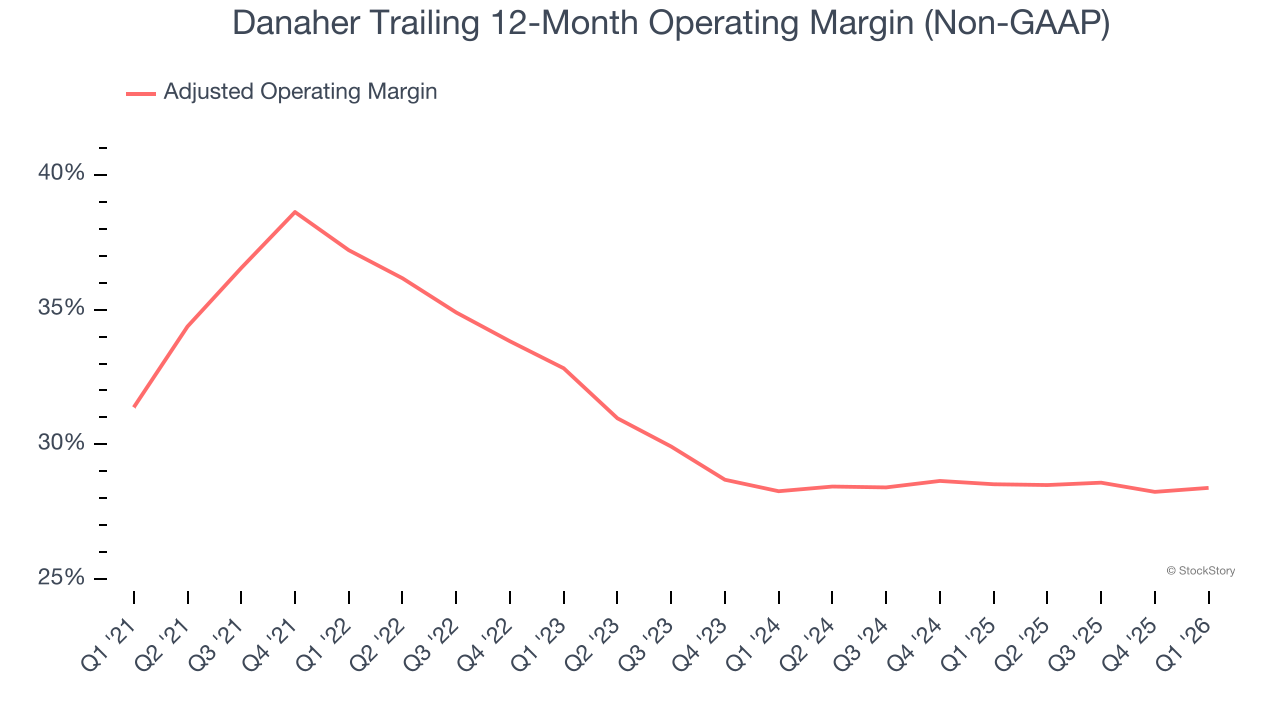

2. Shrinking Adjusted Operating Margin

Adjusted operating margin is a key measure of profitability. Think of it as net income (the bottom line) excluding the impact of non-recurring expenses, taxes, and interest on debt - metrics less connected to business fundamentals.

Looking at the trend in its profitability, Danaher’s adjusted operating margin decreased by 8.8 percentage points over the last five years. Even though its historical margin was healthy, shareholders will want to see Danaher become more profitable in the future. Its adjusted operating margin for the trailing 12 months was 28.4%.

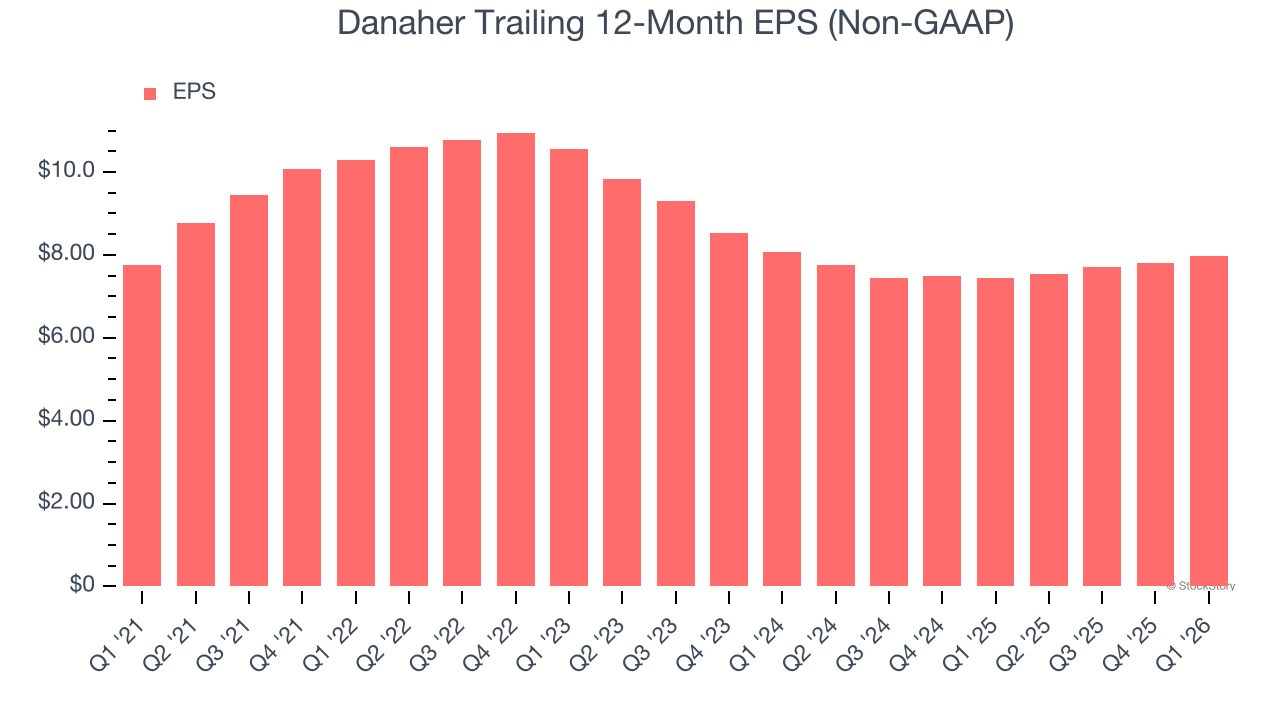

3. EPS Growth Has Stalled

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

Danaher’s EPS was flat over the last five years, just like its revenue. This performance was underwhelming across the board.

Final Judgment

Danaher isn’t a terrible business, but it doesn’t pass our quality test. After the recent drawdown, the stock trades at 21.5× forward P/E (or $178.42 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We’re pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at one of our all-time favorite software stocks.

Stocks We Like More Than Danaher

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.