San Jose, California-based PayPal Holdings, Inc. (PYPL) operates a technology platform that enables digital payments for merchants and consumers worldwide. The company has a market capitalization of $43.2 billion and operates a two-sided network at scale that connects merchants and consumers, enabling its customers to connect, transact, and send and receive payments online and in person.

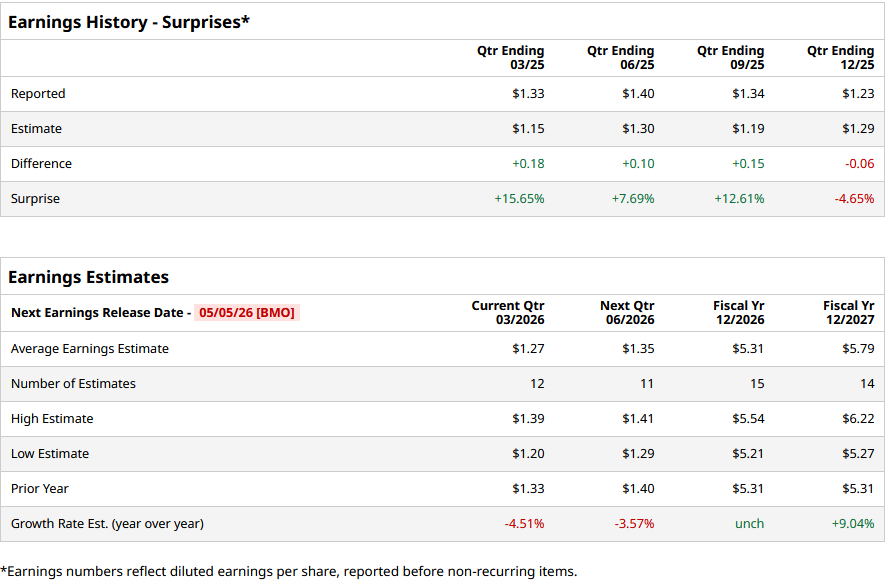

The company is expected to release its Q1 2026 earnings on May 5, before the market opens. Ahead of the event, analysts expect the company’s EPS to be $1.27 on a diluted basis, down 4.5% from $1.33 in the year-ago quarter. The company has exceeded Wall Street’s EPS estimates in three of its last four quarters, while missing on one occasion.

For fiscal 2026, analysts project the company’s EPS to be $5.31, unchanged from fiscal 2025. Moreover, its EPS is expected to rise by roughly 9% year over year (YoY) to $5.79 in fiscal 2027.

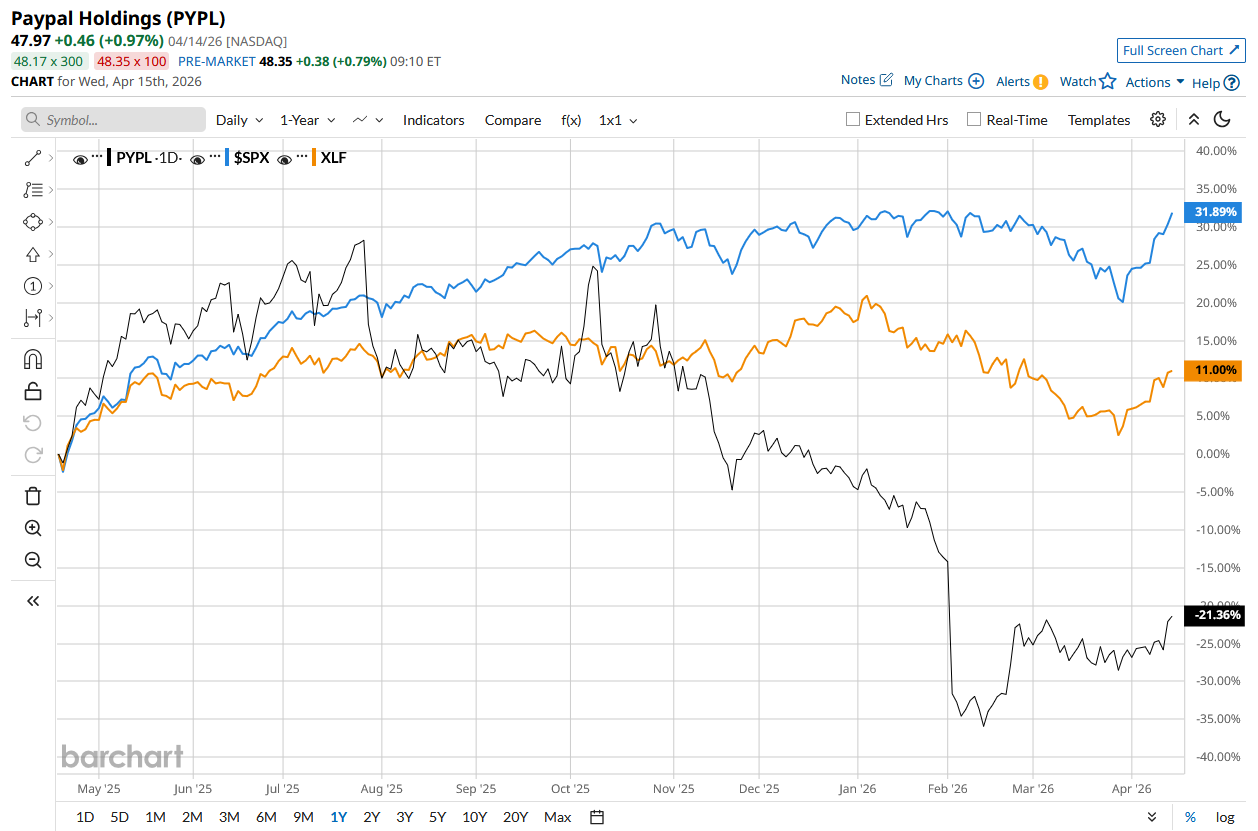

PYPL stock has declined 22.4% over the past 52 weeks, underperforming the S&P 500 Index’s ($SPX) 28.9% rise and the State Street Financial Select Sector SPDR ETF’s (XLF) 9.9% rise during the same time frame.

On Feb. 3, PayPal shares tanked 20.3% following the release of its worst-than-expected Q4 2025 earnings. The company’s revenue increased 3.7% to $8.7 billion but missed the Street’s estimates. Additionally, PYPL’s adjusted EPS for the quarter amounted to $1.23, also failing to surpass Wall Street estimates. Investor confidence was shattered on account of the company failing to meet analyst estimates on both fronts.

Analysts are skeptical about PYPL, with the stock having a “Hold” rating overall. Among the 43 analysts covering the stock, six are recommending a “Strong Buy,” two suggest a “Moderate Buy,” 29 suggest a “Hold,” one suggests a “Moderate Sell,” and five suggest a “Strong Sell.” PYPL’s average analyst price target is $50.67, indicating an upside of 5.6% from the current levels.

On the date of publication, Aritra Gangopadhyay did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Macquarie Is Pounding the Table on CoreWeave Stock with a New ‘Outperform’ Rating. Should You Buy Here?

- Tesla Is Still a ‘Leader in Physical AI’ and You Should Buy TSLA Stock Now, Says UBS

- Turbine Season for Tech: John Rowland on the Next Era of AI Data Center Investments

- IonQ's DARPA Contract Win Makes It the Quantum Computing Stock to Own in 2026