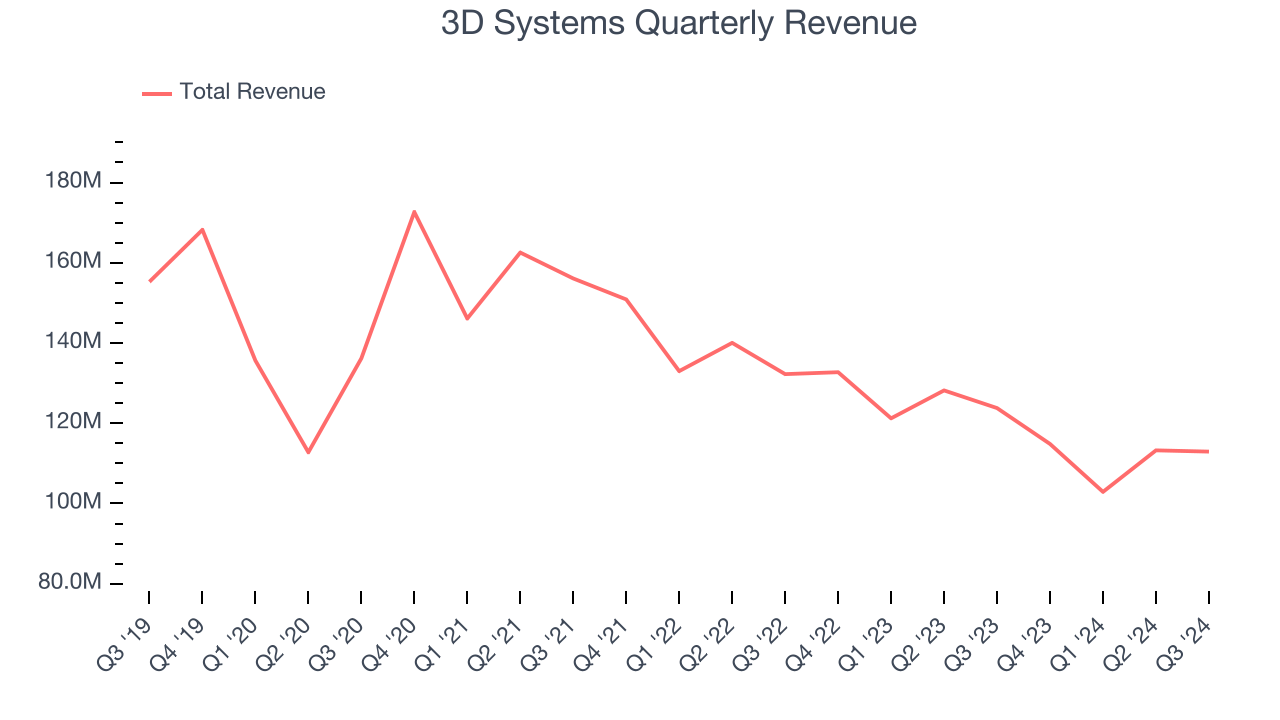

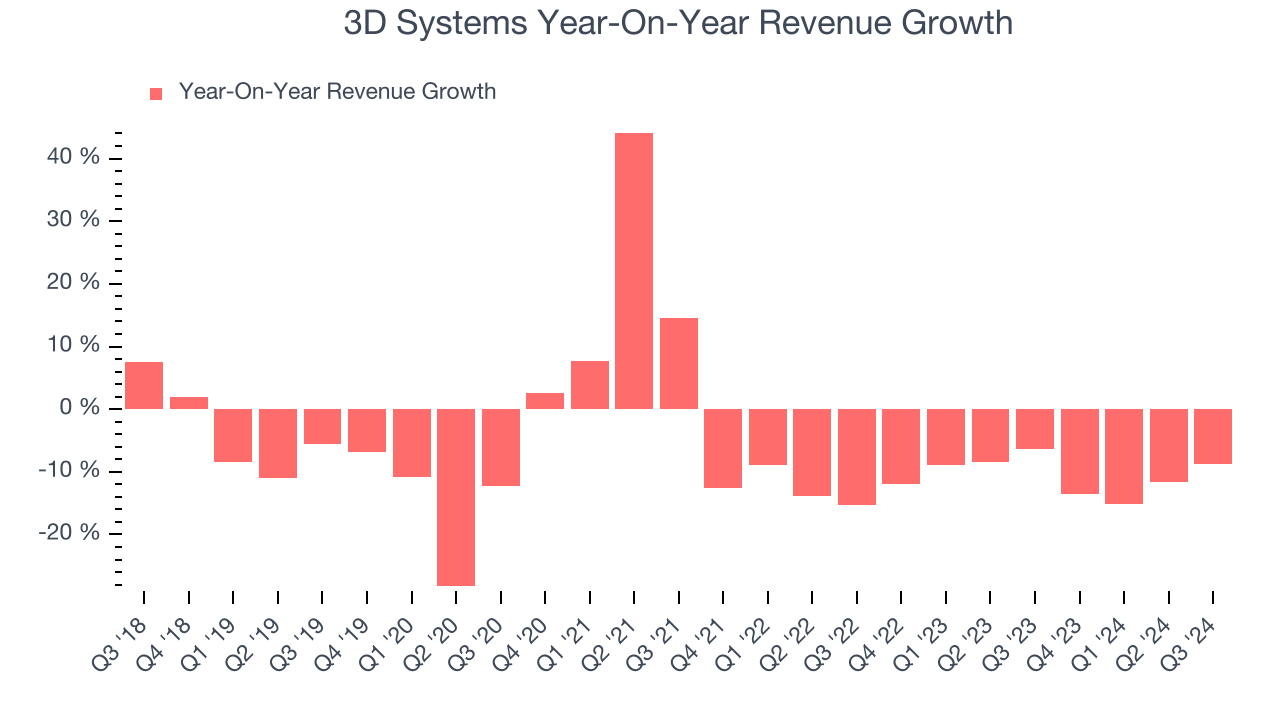

3D printing company 3D Systems (NYSE: DDD) missed Wall Street’s revenue expectations in Q3 CY2024, with sales falling 8.8% year on year to $112.9 million. The company’s full-year revenue guidance of $445 million at the midpoint came in 1.6% below analysts’ estimates. Its non-GAAP loss of $0.12 per share was 26.3% below analysts’ consensus estimates.

Is now the time to buy 3D Systems? Find out by accessing our full research report, it’s free.

3D Systems (DDD) Q3 CY2024 Highlights:

- Revenue: $112.9 million vs analyst estimates of $113.7 million (8.8% year-on-year decline, 0.6% miss)

- Adjusted EPS: -$0.12 vs analyst expectations of -$0.10 (26.3% miss)

- Adjusted EBITDA: -$14,300 vs analyst estimates of -$5.78 million (0% margin, 99.8% beat)

- The company dropped its revenue guidance for the full year to $445 million at the midpoint from $455 million, a 2.2% decrease

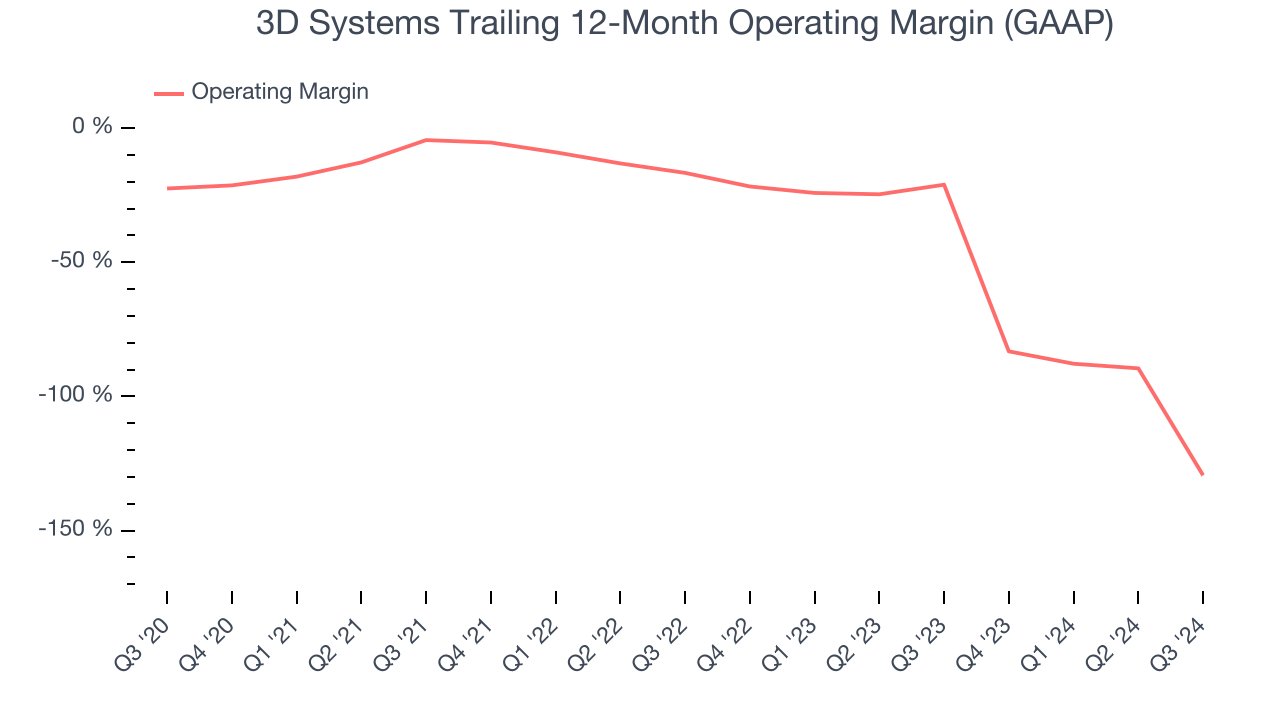

- Operating Margin: -160%, down from -11% in the same quarter last year

- Free Cash Flow was -$4.45 million compared to -$33.07 million in the same quarter last year

- Market Capitalization: $458.2 million

Commenting on third quarter results, Dr. Jeffrey Graves, president and CEO of 3D Systems said, “As recently shared, our third quarter revenues continued to be impacted by sluggish capital investments by our customers for new production capacity, particularly in the Industrial markets, impacting the sale of new printing systems. On a positive note however, capacity utilization for our installed printer fleet broadly increased, translating into an increase in consumable revenues, which grew nearly 10% on both prior year and sequential comparisons. While 2024 has been a challenging year for new printer system sales, we are increasingly encouraged about the future, driven in large part by customer demand for our Application Innovation Group, a group of highly skilled process specialists who assist customers in developing new applications for 3D printing. Year-to-date this group, which spans both polymer and metal solutions, has experienced a rise of over 26% in revenues derived from new application development, particularly in highly regulated markets such a semiconductor equipment manufacturing, oil & gas, aerospace & defense markets, and our medical markets. Much of this performance, and the future growth potential it implies, has been fueled by an aggressive cycle of innovation at our company, enabled by our sustained focus on new product innovation across all of our major polymer and metal printing solutions. As a result of this sustained focus, which we believe differentiates us from many others in our industry, we are on pace to deliver nearly 40 new products to market since the third quarter of last year, and 25 in calendar 2024 alone. We believe no other company in our industry has matched this output that we expect will pay dividends in growth and profitability improvements as the economy rebounds in the future.”

Company Overview

Founded by the inventor of stereolithography, 3D Systems (NYSE: DDD) engineers, manufactures, and sells 3D printers and other related products to the aerospace, automotive, healthcare, and consumer goods industries.

Custom Parts Manufacturing

Onshoring and inventory management–themes that grew in focus after COVID wreaked havoc on global supply chains–are tailwinds for companies that combine economies of scale with reliable service. Many in the space have adopted 3D printing to efficiently address the need for bespoke parts and components, but all companies are still at the whim of economic cycles. For example, consumer spending and interest rates can greatly impact the industrial production that drives demand for these companies’ offerings.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. 3D Systems’s demand was weak over the last five years as its sales fell by 7.2% annually. This fell short of our benchmarks and signals it’s a low quality business.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. 3D Systems’s recent history shows its demand has stayed suppressed as its revenue has declined by 10.7% annually over the last two years.

We can better understand the company’s revenue dynamics by analyzing its most important segments, Industrial and Healthcare, which are 48.8% and 51.2% of revenue. Over the last two years, 3D Systems’s Industrial revenue (aerospace, defense, and transportation manufacturing) averaged 7% year-on-year declines while its Healthcare revenue (dental and medical devices) averaged 13.5% declines.

This quarter, 3D Systems missed Wall Street’s estimates and reported a rather uninspiring 8.8% year-on-year revenue decline, generating $112.9 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 4.7% over the next 12 months, an improvement versus the last two years. Although this projection indicates its newer products and services will catalyze better performance, it is still below average for the sector.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

3D Systems’s high expenses have contributed to an average operating margin of negative 34.4% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Looking at the trend in its profitability, 3D Systems’s annual operating margin decreased significantly over the last five years. The company’s performance was poor no matter how you look at it. It shows operating expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, 3D Systems generated a negative 160% operating margin. The company's consistent lack of profits raise a flag.

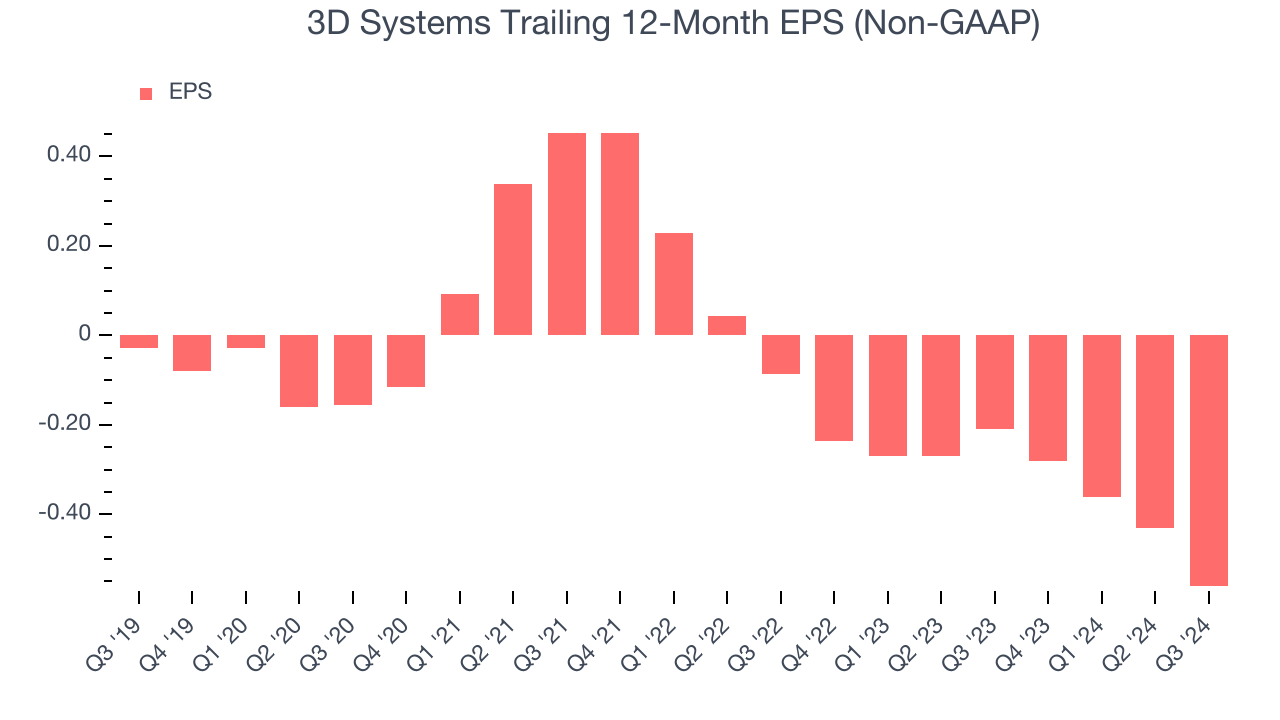

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

3D Systems’s earnings losses deepened over the last five years as its EPS dropped 81% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, 3D Systems’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For 3D Systems, its two-year annual EPS declines of 154% show it’s continued to underperform. These results were bad no matter how you slice the data.In Q3, 3D Systems reported EPS at negative $0.12, down from $0.01 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast 3D Systems’s full-year EPS of negative $0.56 will reach break even.

Key Takeaways from 3D Systems’s Q3 Results

3D Systems's EPS missed significantly and its full-year revenue guidance fell short of Wall Street’s estimates. Overall, this was a bad quarter. The stock traded down 11.8% to $2.99 immediately following the results.

3D Systems underperformed this quarter, but does that create an opportunity to invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.