Shareholders of Ready Capital would probably like to forget the past six months even happened. The stock dropped 29.2% and now trades at $3.13. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in Ready Capital, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free for active Edge members.

Why Do We Think Ready Capital Will Underperform?

Even with the cheaper entry price, we're cautious about Ready Capital. Here are three reasons there are better opportunities than RC and a stock we'd rather own.

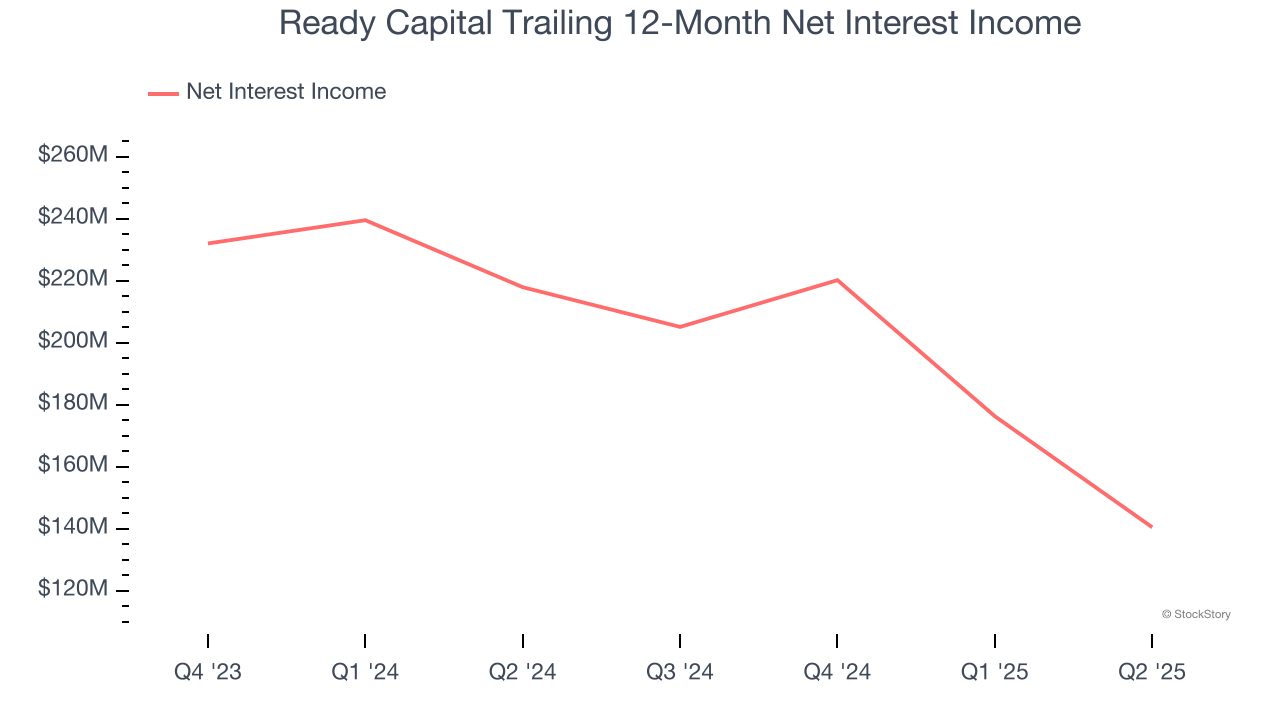

1. Net Interest Income Points to Soft Demand

While bank generate revenue from multiple sources, investors view net interest income as a cornerstone - its predictable, recurring characteristics stand in sharp contrast to the volatility of one-time fees.

Ready Capital’s net interest income has grown at a 4.9% annualized rate over the last five years, worse than the broader banking industry and slower than its total revenue.

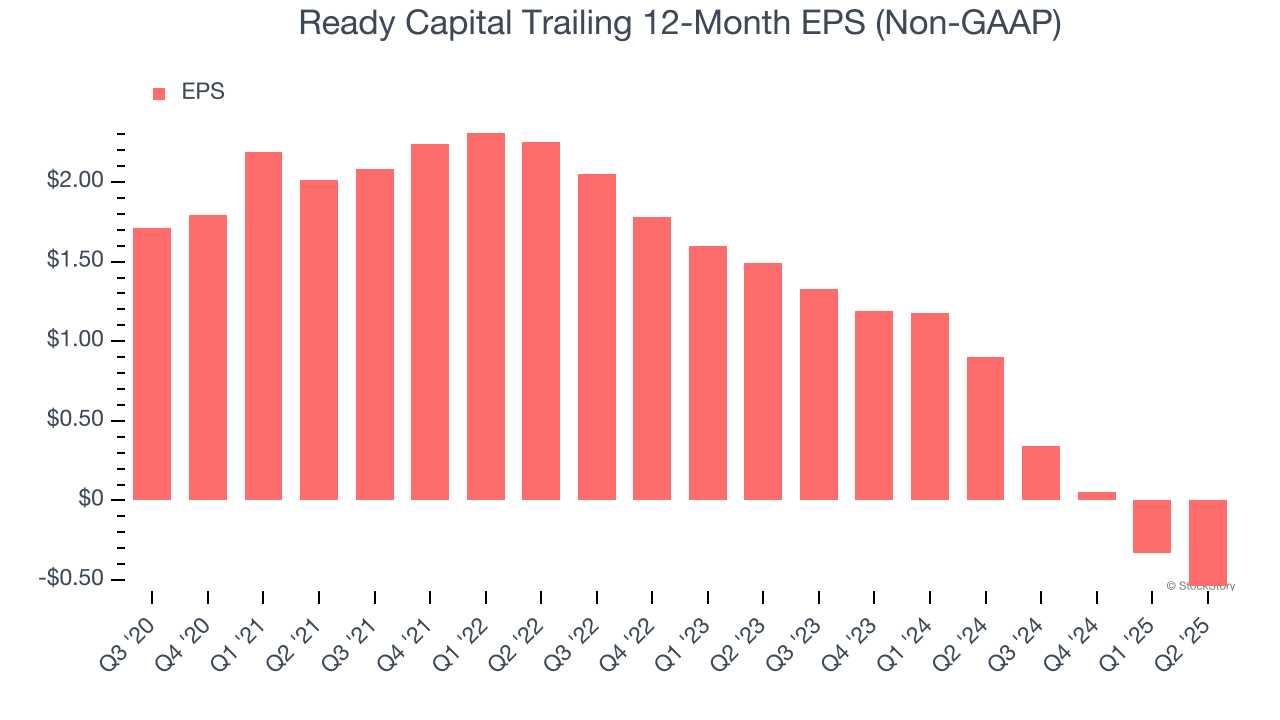

2. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Ready Capital, its EPS declined by 17.4% annually over the last five years while its revenue grew by 10.2%. This tells us the company became less profitable on a per-share basis as it expanded.

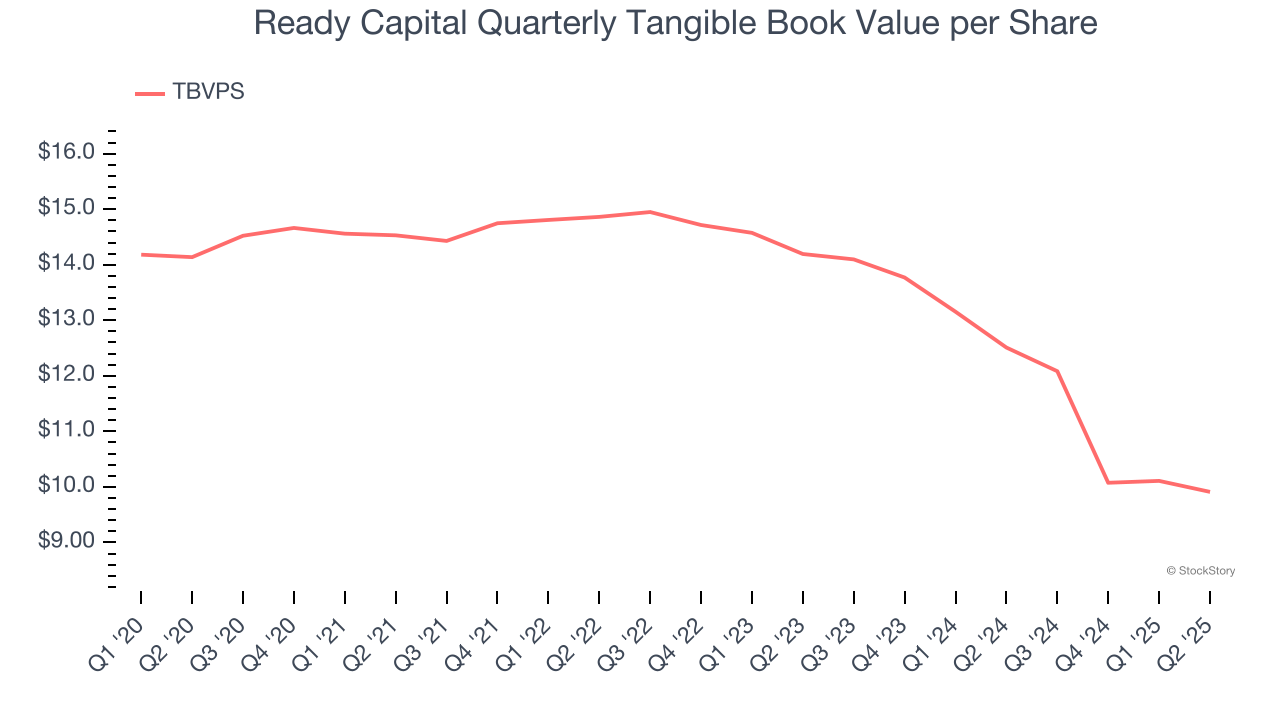

3. Declining TBVPS Reflects Erosion of Asset Value

Tangible book value per share (TBVPS) serves as a key indicator of a bank’s financial strength, representing the hard assets available to shareholders after removing intangible assets that could evaporate during financial distress.

Disappointingly for investors, Ready Capital’s TBVPS continued freefalling over the past two years as TBVPS declined at a -16.4% annual clip (from $14.19 to $9.91 per share).

Final Judgment

We see the value of companies driving economic growth, but in the case of Ready Capital, we’re out. After the recent drawdown, the stock trades at 0.3× forward P/B (or $3.13 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are superior stocks to buy right now. We’d suggest looking at one of our top digital advertising picks.

Stocks We Would Buy Instead of Ready Capital

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.