Let’s dig into the relative performance of Cracker Barrel (NASDAQ: CBRL) and its peers as we unravel the now-completed Q4 sit-down dining earnings season.

Sit-down restaurants offer a complete dining experience with table service. These establishments span various cuisines and are renowned for their warm hospitality and welcoming ambiance, making them perfect for family gatherings, special occasions, or simply unwinding. Their extensive menus range from appetizers to indulgent desserts and wines and cocktails. This space is extremely fragmented and competition includes everything from publicly-traded companies owning multiple chains to single-location mom-and-pop restaurants.

The 11 sit-down dining stocks we track reported a satisfactory Q4. As a group, revenues were in line with analysts’ consensus estimates.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 6.9% since the latest earnings results.

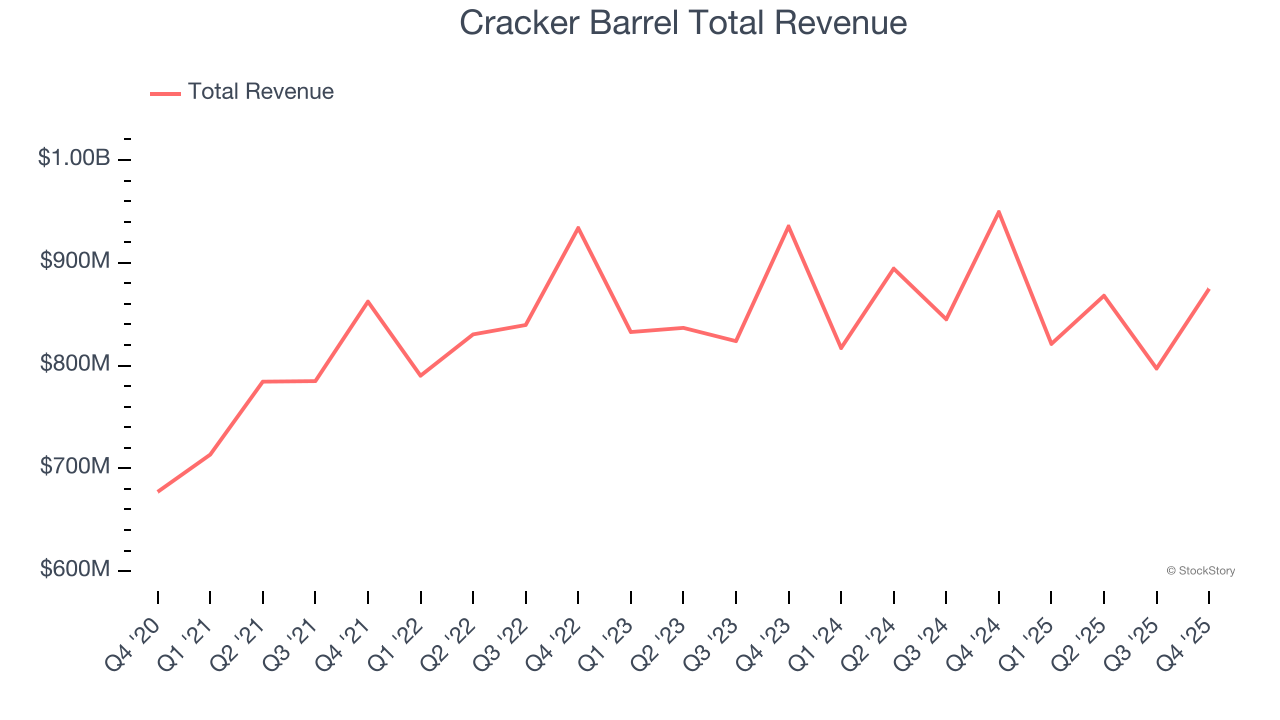

Cracker Barrel (NASDAQ: CBRL)

Known for its country-themed food and merchandise, Cracker Barrel (NASDAQ: CBRL) is a beloved American restaurant and retail chain that celebrates the warmth and charm of Southern hospitality.

Cracker Barrel reported revenues of $874.8 million, down 7.9% year on year. This print exceeded analysts’ expectations by 1.2%. Overall, it was a very strong quarter for the company with a beat of analysts’ EPS and EBITDA estimates.

Cracker Barrel President and Chief Executive Officer Julie Masino said, "Our disciplined focus on operational excellence is driving significant improvements in several key guest metrics, many of which serve as important leading traffic indicators. We have also taken additional actions to improve financial performance and remain confident that we are well-positioned to regain prior momentum."

Cracker Barrel delivered the slowest revenue growth of the whole group. Unsurprisingly, the stock is down 10.1% since reporting and currently trades at $27.53.

Is now the time to buy Cracker Barrel? Access our full analysis of the earnings results here, it’s free.

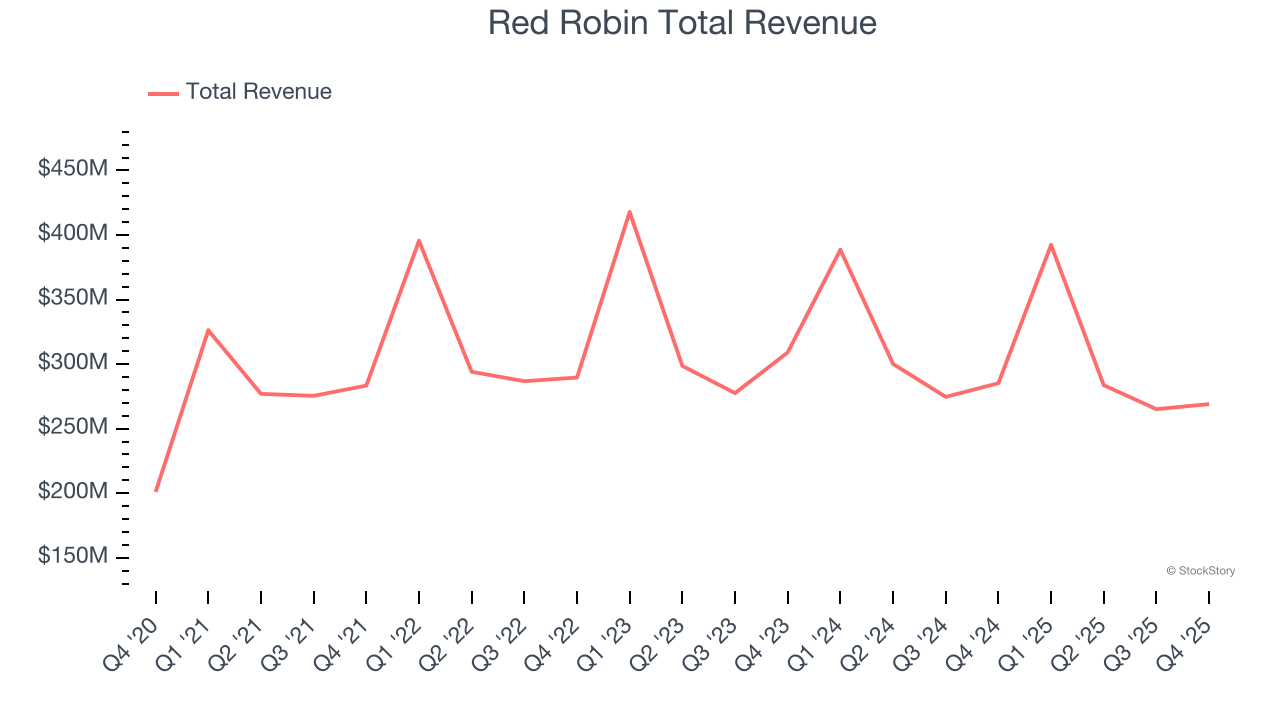

Best Q4: Red Robin (NASDAQ: RRGB)

Known for its bottomless steak fries, Red Robin (NASDAQ: RRGB) is a chain of casual restaurants specializing in burgers and general American fare.

Red Robin reported revenues of $269 million, down 5.7% year on year, outperforming analysts’ expectations by 1.8%. The business had an exceptional quarter with an impressive beat of analysts’ EBITDA estimates and full-year EBITDA guidance beating analysts’ expectations.

Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 14.5% since reporting. It currently trades at $3.11.

Is now the time to buy Red Robin? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Texas Roadhouse (NASDAQ: TXRH)

With locations often featuring Western-inspired decor, Texas Roadhouse (NASDAQ: TXRH) is an American restaurant chain specializing in Southern-style cuisine and steaks.

Texas Roadhouse reported revenues of $1.48 billion, up 3.1% year on year, falling short of analysts’ expectations by 0.8%. It was a softer quarter as it posted a significant miss of analysts’ EBITDA estimates and a significant miss of analysts’ EPS estimates.

As expected, the stock is down 7.5% since the results and currently trades at $168.83.

Read our full analysis of Texas Roadhouse’s results here.

Kura Sushi (NASDAQ: KRUS)

Known for its conveyor belt that transports dishes to diners, Kura Sushi (NASDAQ: KRUS) is a chain of sushi restaurants serving traditional Japanese fare with a touch of modernity and technology.

Kura Sushi reported revenues of $73.46 million, up 14% year on year. This result met analysts’ expectations. Taking a step back, it was a slower quarter as it logged a significant miss of analysts’ EBITDA estimates and a significant miss of analysts’ EPS estimates.

Kura Sushi delivered the highest full-year guidance raise among its peers. The stock is up 15% since reporting and currently trades at $64.

Read our full, actionable report on Kura Sushi here, it’s free.

BJ's (NASDAQ: BJRI)

Founded in 1978 in California, BJ’s Restaurants (NASDAQ: BJRI) is a chain of restaurants whose menu features classic American dishes, often with a twist.

BJ's reported revenues of $355.4 million, up 3.2% year on year. This print beat analysts’ expectations by 0.6%. More broadly, it was a mixed quarter as it also logged full-year EBITDA guidance topping analysts’ expectations but a miss of analysts’ EBITDA estimates.

The stock is down 10.2% since reporting and currently trades at $36.70.

Read our full, actionable report on BJ's here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.