Since April 2021, the S&P 500 has delivered a total return of 69.7%. But one standout stock has more than doubled the market - over the past five years, Atlanticus Holdings has surged 149% to $79.96 per share. Its momentum hasn’t stopped as it’s also gained 34.1% in the last six months thanks to its solid quarterly results, beating the S&P by 30.7%.

Is there a buying opportunity in Atlanticus Holdings, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Atlanticus Holdings Not Exciting?

Despite the momentum, we're swiping left on Atlanticus Holdings for now. Here are two reasons why ATLC doesn't excite us and a stock we'd rather own.

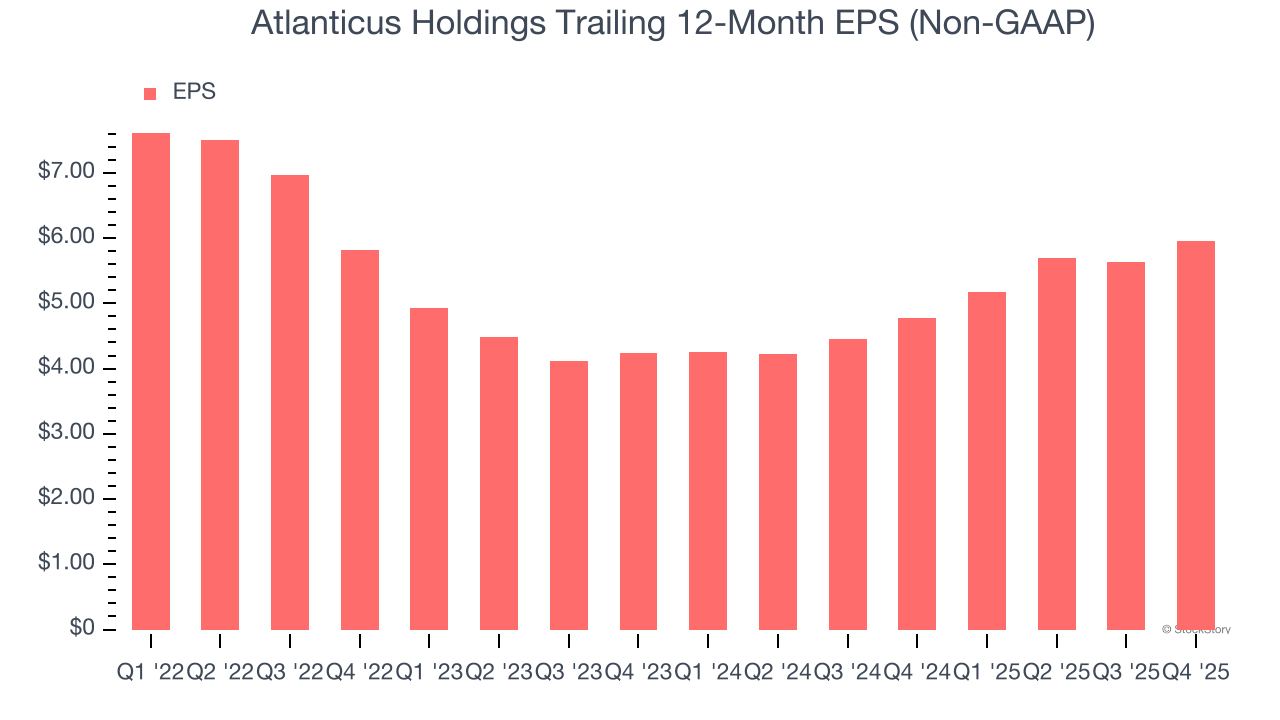

1. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Atlanticus Holdings’s full-year EPS dropped 24.8%, or 5.7% annually, over the last four years. We’ll keep a close eye on the company as diminishing earnings could imply changing secular trends and preferences.

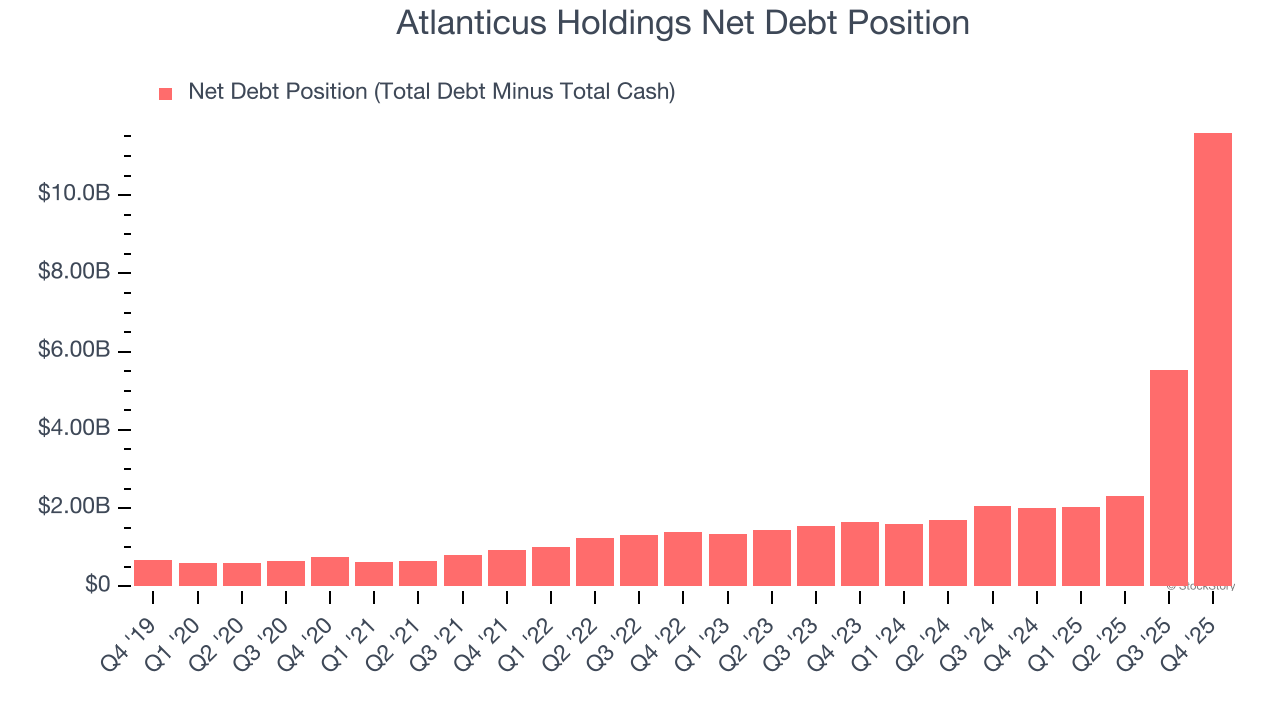

2. High Debt Levels Increase Risk

Atlanticus Holdings reported $767.4 million of cash and $12.37 billion of debt on its balance sheet in the most recent quarter.

As investors in high-quality companies, we primarily focus on whether a company’s profits can support its debt.

With $176.6 million of EBITDA over the last 12 months, we view Atlanticus Holdings’s 65.7× net-debt-to-EBITDA ratio as inadequate. The company’s lacking profits relative to its borrowings give it little breathing room, raising red flags.

Final Judgment

Atlanticus Holdings isn’t a terrible business, but it isn’t one of our picks. With its shares topping the market in recent months, the stock trades at 8.5× forward P/E (or $79.96 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are superior stocks to buy right now. Let us point you toward a safe-and-steady industrials business benefiting from an upgrade cycle.

High-Quality Stocks for All Market Conditions

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.