The Honest Company has been treading water for the past six months, recording a small loss of 2.7% while holding steady at $3.57. The stock also fell short of the S&P 500’s 3.4% gain during that period.

Is there a buying opportunity in The Honest Company, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Do We Think The Honest Company Will Underperform?

We're cautious about The Honest Company. Here are three reasons there are better opportunities than HNST and a stock we'd rather own.

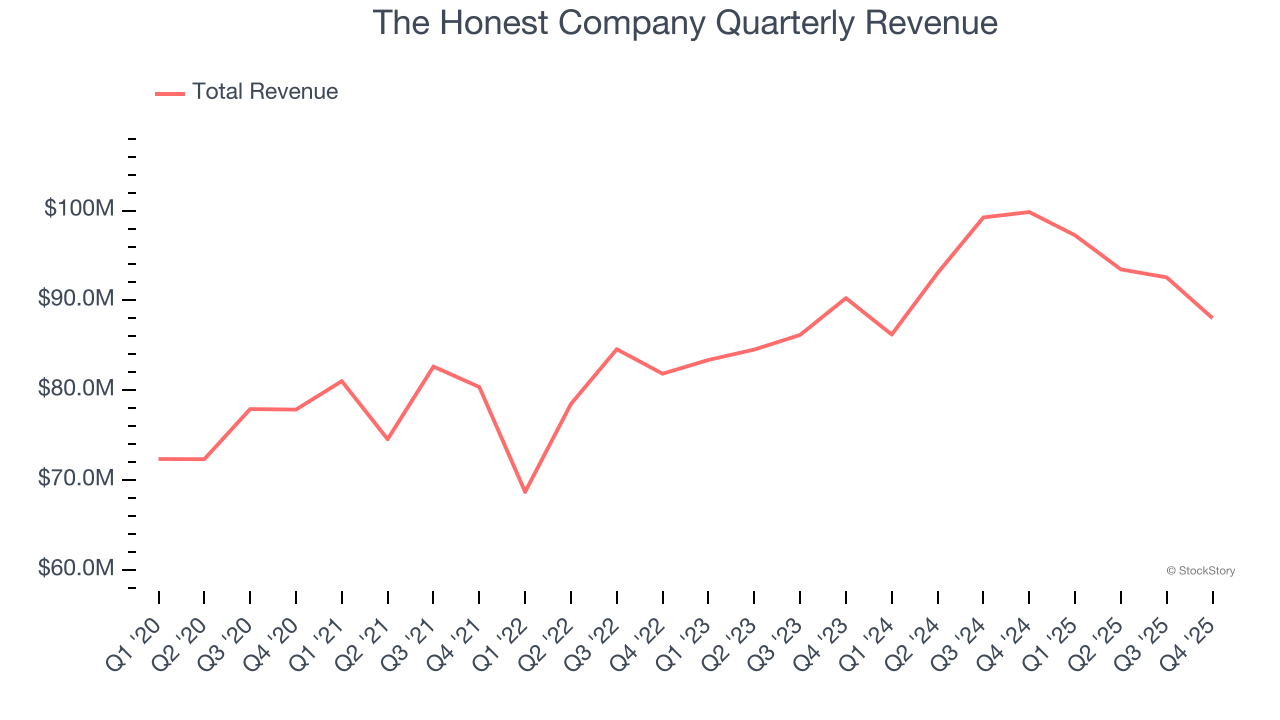

1. Long-Term Revenue Growth Disappoints

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, The Honest Company’s 5.8% annualized revenue growth over the last three years was mediocre. This was below our standard for the consumer staples sector.

2. Fewer Distribution Channels Limit its Ceiling

With $371.3 million in revenue over the past 12 months, The Honest Company is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

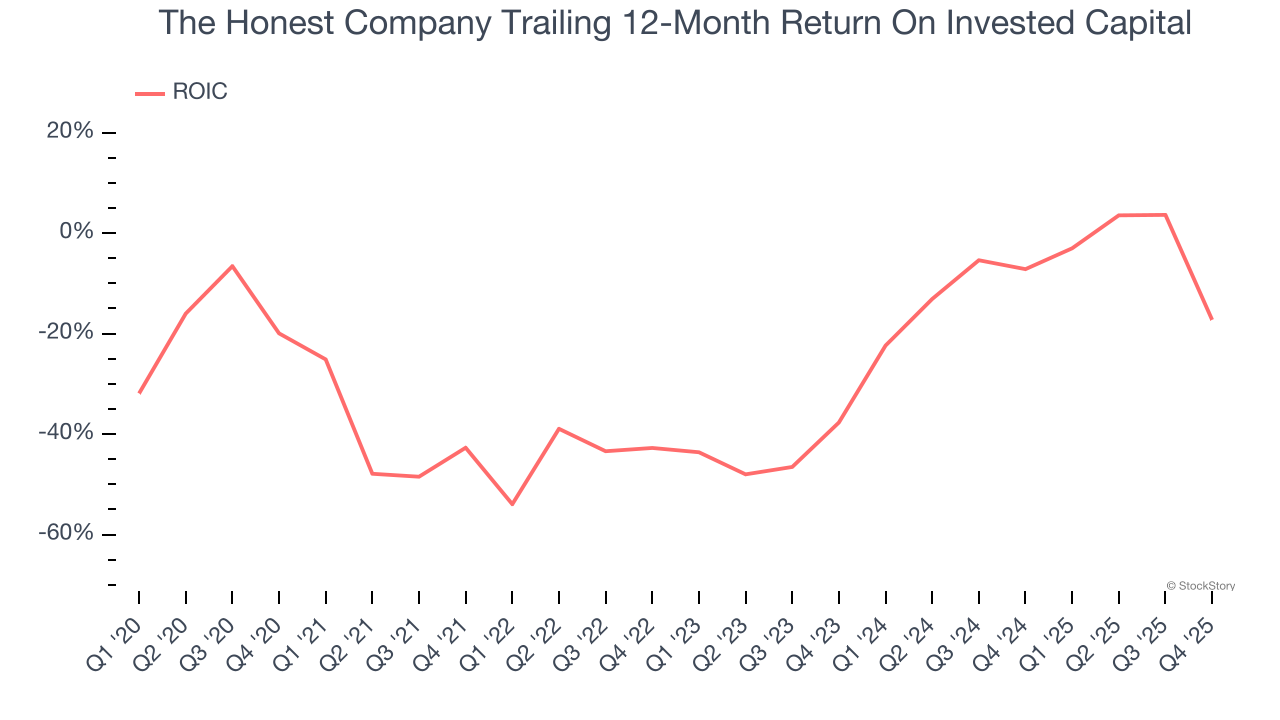

3. Previous Growth Initiatives Have Lost Money

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

The Honest Company’s five-year average ROIC was negative 29.5%, meaning management lost money while trying to expand the business. Its returns were among the worst in the consumer staples sector.

Final Judgment

The Honest Company doesn’t pass our quality test. With its shares lagging the market recently, the stock trades at 37.2× forward P/E (or $3.57 per share). This valuation tells us a lot of optimism is priced in - we think there are better stocks to buy right now. Let us point you toward a dominant Aerospace business that has perfected its M&A strategy.

High-Quality Stocks for All Market Conditions

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.