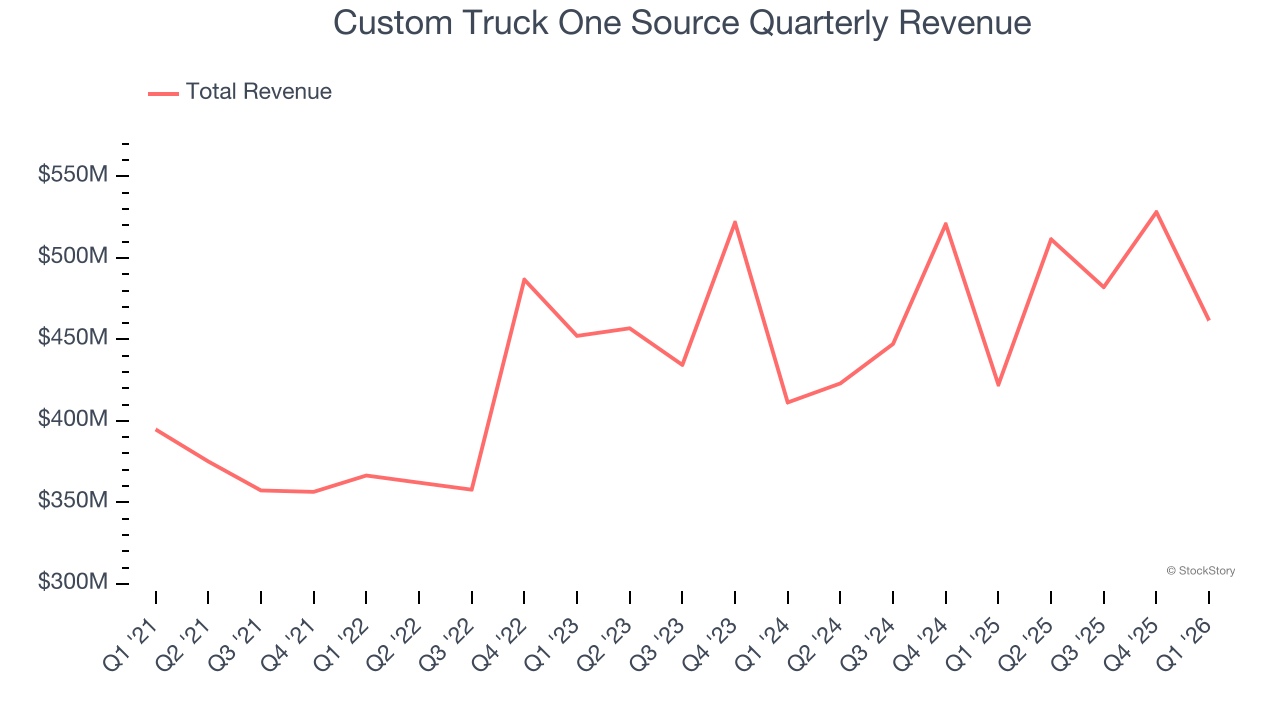

Heavy equipment distributor Custom Truck One Source (NYSE: CTOS) reported Q1 CY2026 results exceeding the market’s revenue expectations, with sales up 9.3% year on year to $461.6 million. The company’s full-year revenue guidance of $2.06 billion at the midpoint came in 1.5% above analysts’ estimates. Its GAAP loss of $0.02 per share was 62.9% above analysts’ consensus estimates.

Is now the time to buy Custom Truck One Source? Find out by accessing our full research report, it’s free.

Custom Truck One Source (CTOS) Q1 CY2026 Highlights:

- Revenue: $461.6 million vs analyst estimates of $454.2 million (9.3% year-on-year growth, 1.6% beat)

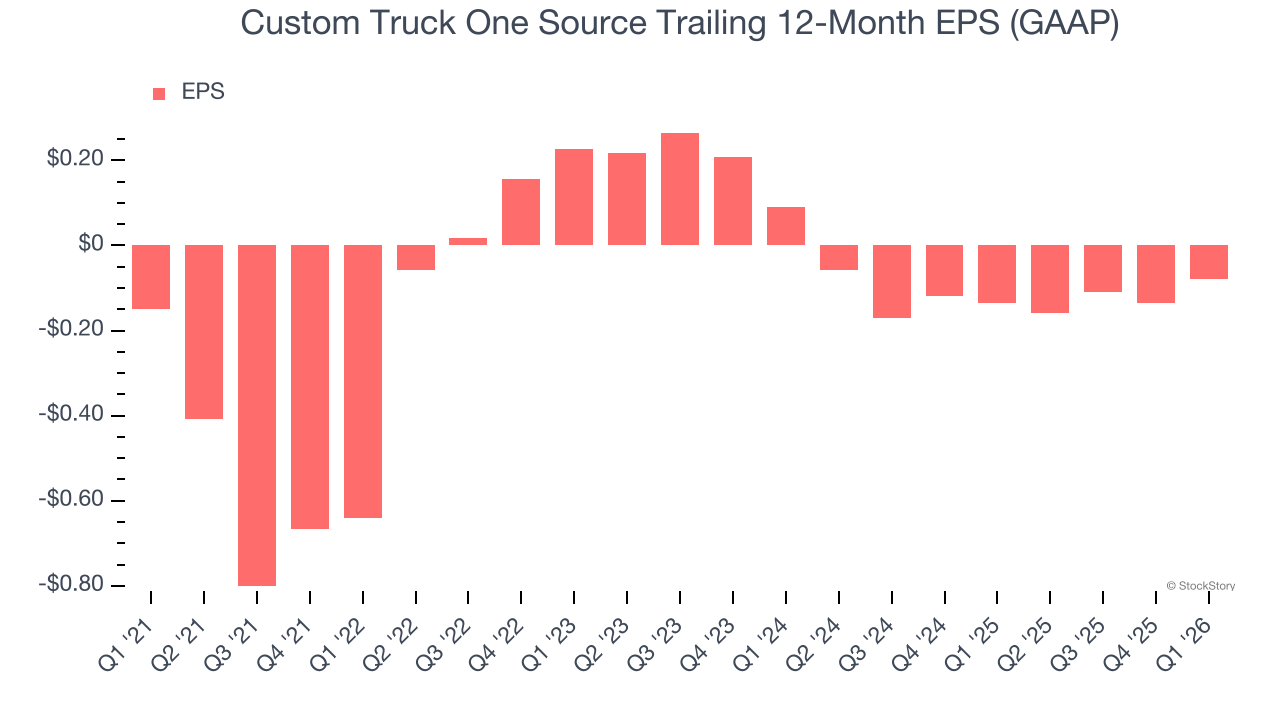

- EPS (GAAP): -$0.02 vs analyst estimates of -$0.05 (62.9% beat)

- Adjusted EBITDA: $97.99 million vs analyst estimates of $86.33 million (21.2% margin, 13.5% beat)

- The company reconfirmed its revenue guidance for the full year of $2.06 billion at the midpoint

- EBITDA guidance for the full year is $427.5 million at the midpoint, in line with analyst expectations

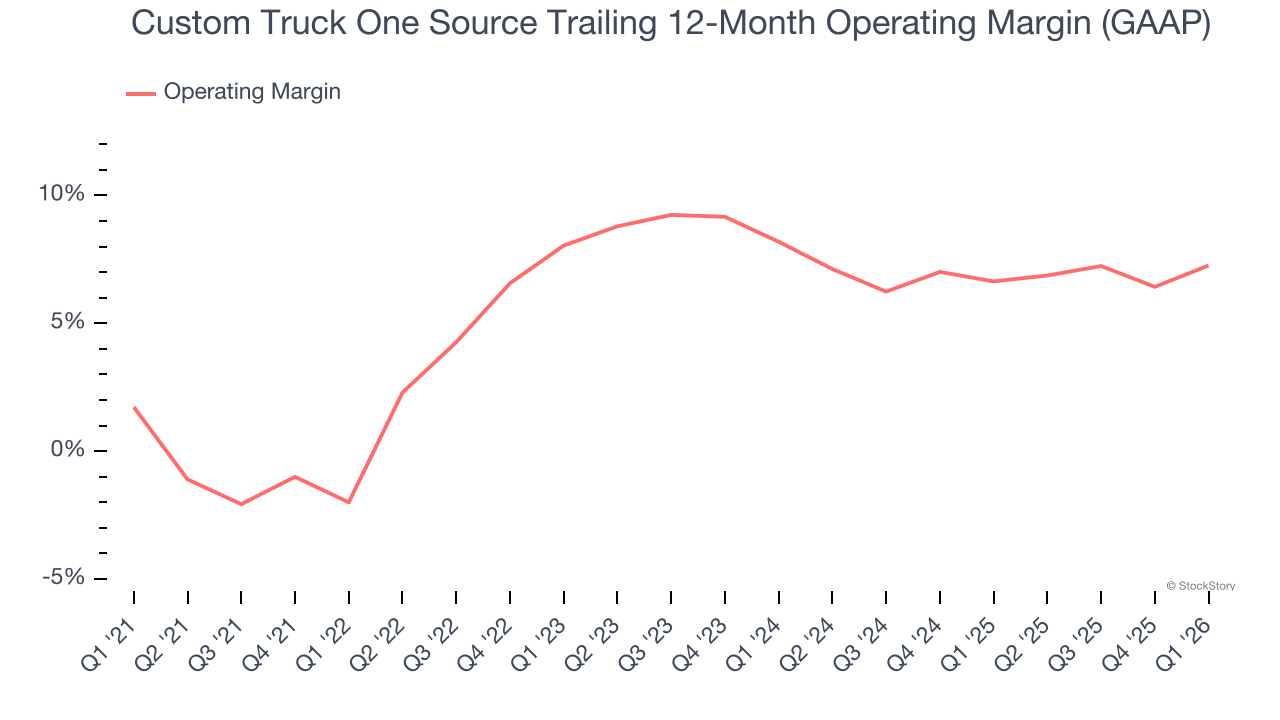

- Operating Margin: 6.8%, up from 2.9% in the same quarter last year

- Free Cash Flow was -$73.09 million compared to -$56.3 million in the same quarter last year

- Backlog: $411.3 million at quarter end, down 2.1% year on year

- Market Capitalization: $1.98 billion

“In the first quarter, we achieved record first-quarter revenue and delivered substantial year-over-year growth in revenue and Adjusted EBITDA of 9% and 33%, respectively. The sustained performance in our core T&D markets continues to be the primary driver of performance within our SER segment and for the Company as a whole. For the quarter, our rental fleet achieved average utilization of 81.4%, up 370 basis points versus the first quarter of last year. We ended the quarter with total OEC of $1.66 billion, the highest in our history, which should support our expected growth within SER in 2026,” said Ryan McMonagle, Chief Executive Officer of CTOS.

Company Overview

Inspired by a family gas station, Custom Truck One Source (NYSE: CTOS) is a distributor of trucks and heavy equipment.

Revenue Growth

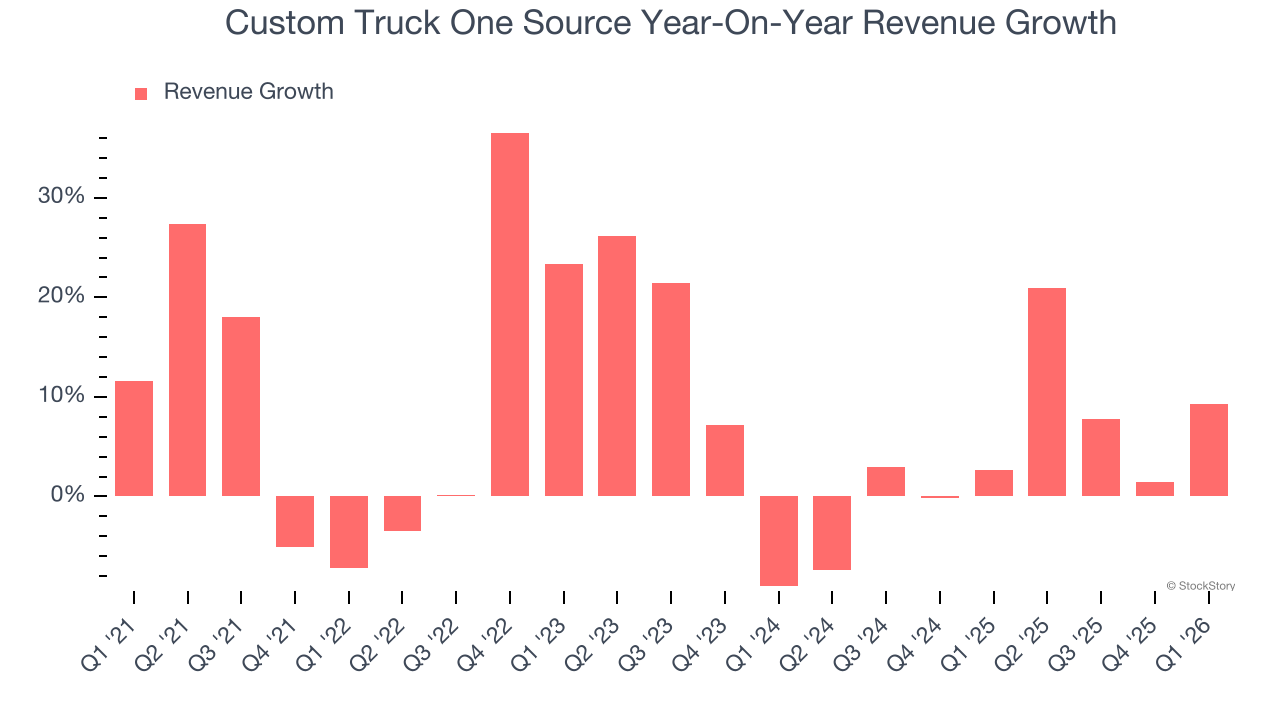

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Thankfully, Custom Truck One Source’s 7.7% annualized revenue growth over the last five years was decent. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Custom Truck One Source’s recent performance shows its demand has slowed as its annualized revenue growth of 4.3% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Custom Truck One Source reported year-on-year revenue growth of 9.3%, and its $461.6 million of revenue exceeded Wall Street’s estimates by 1.6%.

Looking ahead, sell-side analysts expect revenue to grow 3.8% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and suggests its newer products and services will not accelerate its top-line performance yet.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Operating Margin

Custom Truck One Source was profitable over the last five years but held back by its large cost base. Its average operating margin of 5.9% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

On the plus side, Custom Truck One Source’s operating margin rose by 9.3 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, Custom Truck One Source generated an operating margin profit margin of 6.8%, up 3.9 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although Custom Truck One Source’s full-year earnings are still negative, it reduced its losses and improved its EPS by 12.2% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Sadly for Custom Truck One Source, its EPS declined by 69.2% annually over the last two years while its revenue grew by 4.3%. This tells us the company became less profitable on a per-share basis as it expanded.

In Q1, Custom Truck One Source reported EPS of negative $0.02, up from negative $0.08 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street is optimistic. Analysts forecast Custom Truck One Source’s full-year EPS of negative $0.08 will flip to positive $0.07.

Key Takeaways from Custom Truck One Source’s Q1 Results

It was good to see Custom Truck One Source beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock traded up 2.7% to $9.01 immediately following the results.

Custom Truck One Source had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).