Graphic Packaging Holding’s stock price has taken a beating over the past six months, shedding 44.1% of its value and falling to $9.64 per share. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in Graphic Packaging Holding, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Do We Think Graphic Packaging Holding Will Underperform?

Despite the more favorable entry price, we don't have much confidence in Graphic Packaging Holding. Here are three reasons why GPK doesn't excite us and a stock we'd rather own.

1. Long-Term Revenue Growth Disappoints

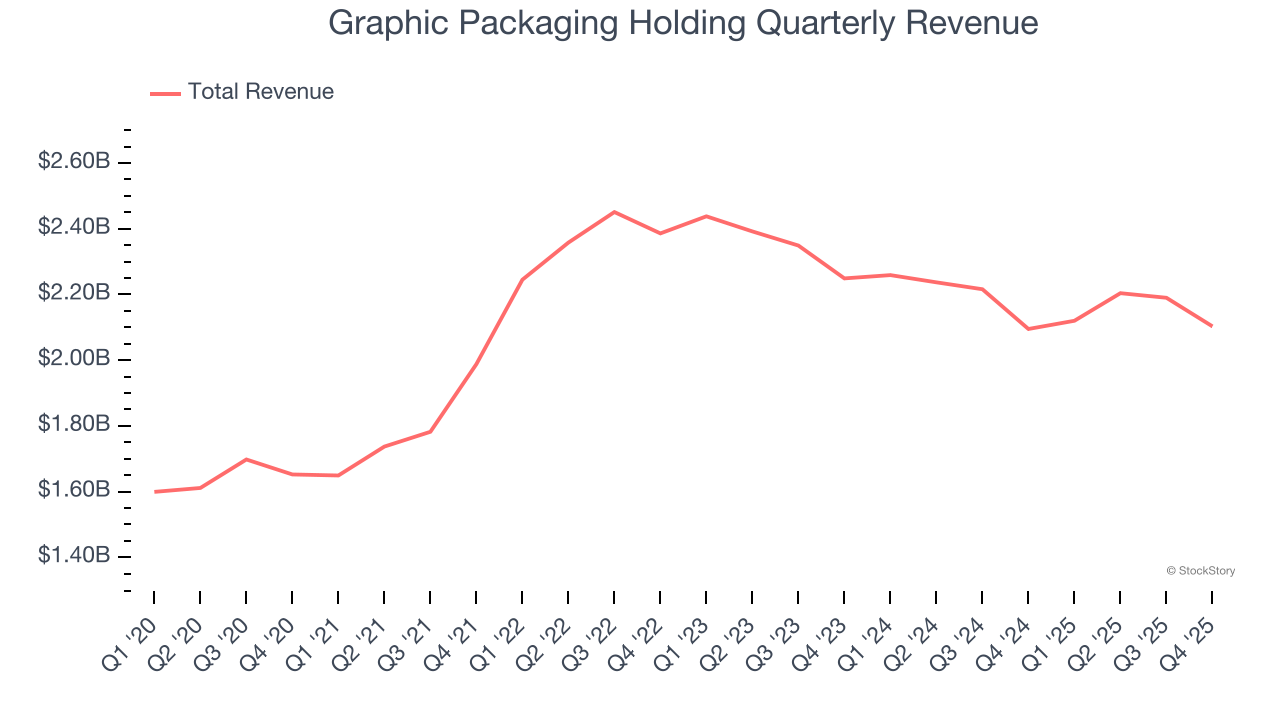

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, Graphic Packaging Holding’s sales grew at a tepid 5.6% compounded annual growth rate over the last five years. This was below our standard for the industrials sector.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Graphic Packaging Holding’s revenue to drop by 2.1%. While this projection is better than its two-year trend, it’s hard to get excited about a company that is struggling with demand.

3. EPS Took a Dip Over the Last Two Years

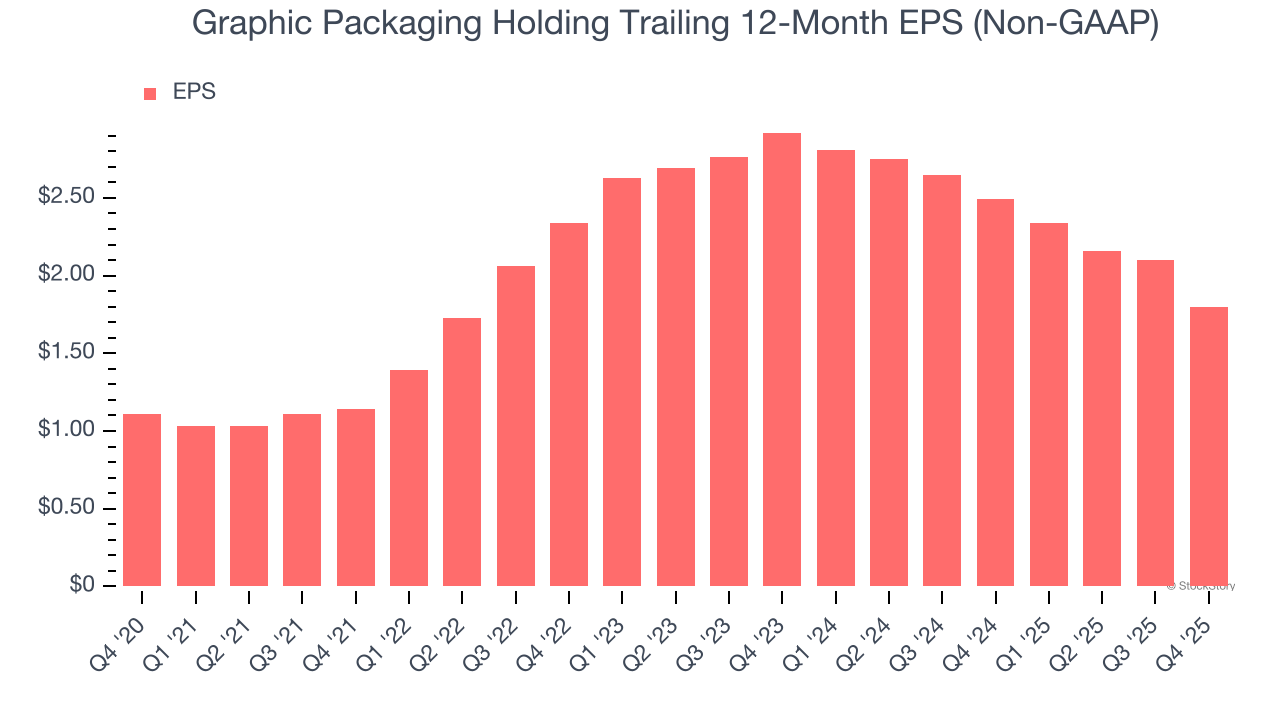

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Sadly for Graphic Packaging Holding, its EPS declined by more than its revenue over the last two years, dropping 21.5%. This tells us the company struggled to adjust to shrinking demand.

Final Judgment

Graphic Packaging Holding doesn’t pass our quality test. After the recent drawdown, the stock trades at 11× forward P/E (or $9.64 per share). This valuation multiple is fair, but we don’t have much confidence in the company. There are better stocks to buy right now. We’d suggest looking at a top digital advertising platform riding the creator economy.

High-Quality Stocks for All Market Conditions

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.