As the craze of earnings season draws to a close, here’s a look back at some of the most exciting (and some less so) results from Q1. Today, we are looking at home construction materials stocks, starting with Quanex (NYSE: NX).

Traditionally, home construction materials companies have built economic moats with expertise in specialized areas, brand recognition, and strong relationships with contractors. More recently, advances to address labor availability and job site productivity have spurred innovation that is driving incremental demand. However, these companies are at the whim of residential construction volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates. Additionally, the costs of raw materials can be driven by a myriad of worldwide factors and greatly influence the profitability of home construction materials companies.

The 11 home construction materials stocks we track reported a strong Q1. As a group, revenues beat analysts’ consensus estimates by 2.8% while next quarter’s revenue guidance was in line.

In light of this news, share prices of the companies have held steady. On average, they are relatively unchanged since the latest earnings results.

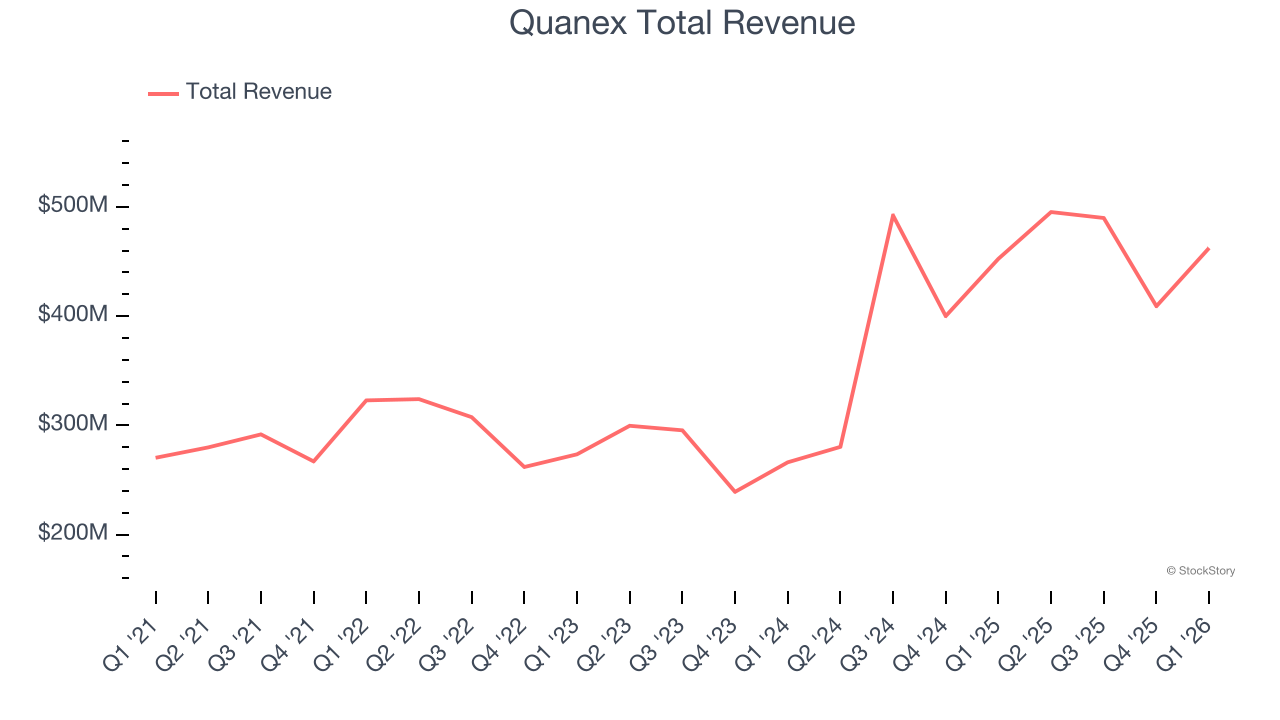

Quanex (NYSE: NX)

Starting in the seamless tube industry, Quanex (NYSE: NX) manufactures building products like window, door, kitchen, and bath cabinet components.

Quanex reported revenues of $462.4 million, up 2.2% year on year. This print exceeded analysts’ expectations by 0.6%. Overall, it was an exceptional quarter for the company with a solid beat of analysts’ adjusted operating income estimates and a beat of analysts’ EPS estimates.

George Wilson, Chairman, President and Chief Executive Officer, commented, “Despite the headwinds our industry is facing, demand for the products we manufacture was as expected during the second quarter of 2026. Rapid inflationary pressures related to macroeconomic concerns and the ongoing conflict in the Middle East led to an unfavorable price versus cost dynamic, which pressured our margins. As previously disclosed, we utilize surcharges to respond to rapid increases in costs and we have index pricing mechanisms in place in North America to handle fluctuations in major raw material costs, but when costs increase quickly there is a timing lag and margins are negatively impacted. We are addressing the current price versus cost imbalance to minimize further negative impact and expect to recover some of the shortfall to date during the second half of this year, assuming volumes continue to track the normal seasonality of our business, and the rate of inflationary pressure subsides.

Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 10.9% since reporting and currently trades at $15.87.

Is now the time to buy Quanex? Access our full analysis of the earnings results here, it’s free.

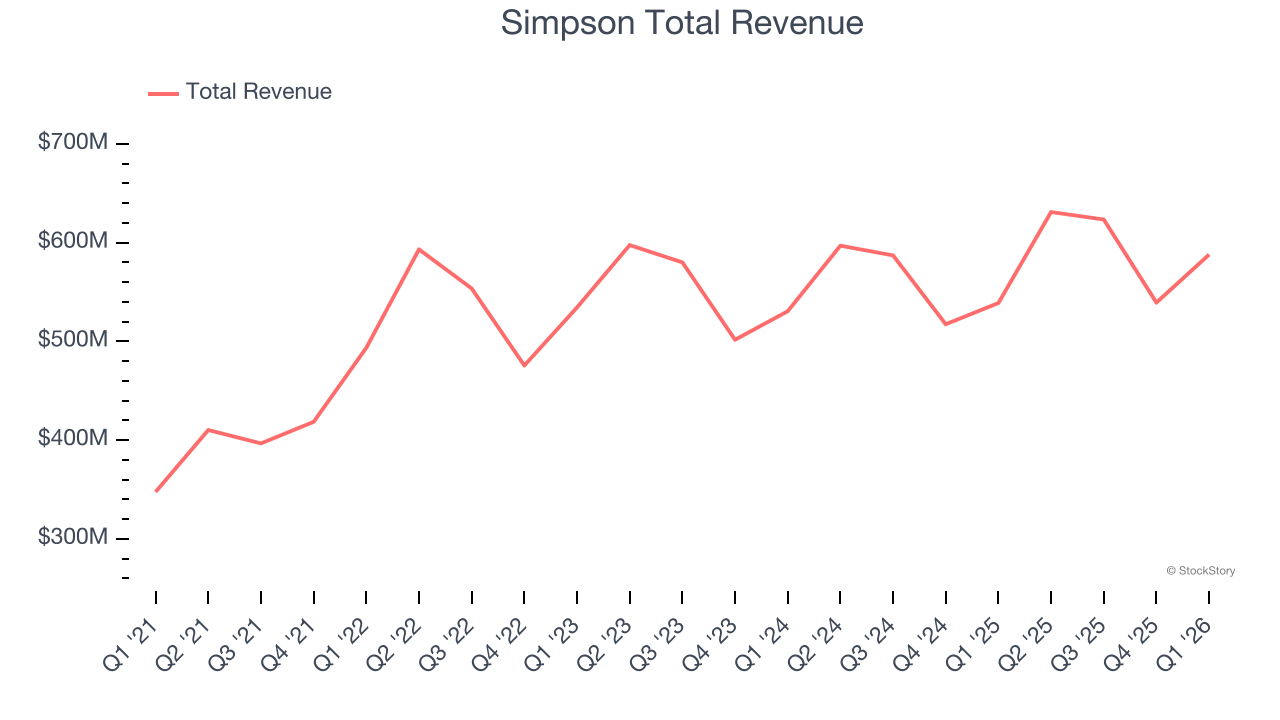

Best Q1: Simpson (NYSE: SSD)

Aiming to build safer and stronger buildings, Simpson (NYSE: SSD) designs and manufactures structural connectors, anchors, and other construction products.

Simpson reported revenues of $588 million, up 9.1% year on year, outperforming analysts’ expectations by 6.4%. The business had a stunning quarter with a solid beat of analysts’ EBITDA estimates.

However, the results were likely priced into the stock as it’s traded sideways since reporting. Shares currently sit at $186.23.

Is now the time to buy Simpson? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Griffon (NYSE: GFF)

Initially in the defense industry, Griffon (NYSE: GFF) is a now diversified company specializing in home improvement, professional equipment, and building products.

Griffon reported revenues of $421.9 million, down 1.1% year on year, exceeding analysts’ expectations by 1.8%. Still, it was a slower quarter as it posted full-year revenue and full-year EBITDA guidance missing analysts’ expectations.

Griffon delivered the weakest full-year guidance update in the group. As expected, the stock is down 1.9% since the results and currently trades at $90.78.

Read our full analysis of Griffon’s results here.

Hayward (NYSE: HAYW)

Credited with introducing the first variable-speed pool pump, Hayward (NYSE: HAYW) makes residential and commercial pool equipment and accessories.

Hayward reported revenues of $255.2 million, up 11.5% year on year. This number topped analysts’ expectations by 6.5%. It was a stunning quarter as it also put up an impressive beat of analysts’ EBITDA estimates.

Hayward pulled off the biggest analyst estimate beat among its peers. The stock is down 10.7% since reporting and currently trades at $14.12.

Read our full, actionable report on Hayward here, it’s free.

JELD-WEN (NYSE: JELD)

Founded in the 1960s as a general wood-making company, JELD-WEN (NYSE: JELD) manufactures doors, windows, and other related building products.

JELD-WEN reported revenues of $722.1 million, down 6.9% year on year. This result met analysts’ expectations. Zooming out, it was a mixed quarter as it also recorded full-year EBITDA guidance exceeding analysts’ expectations but a significant miss of analysts’ adjusted operating income estimates.

The stock is up 20.4% since reporting and currently trades at $1.67.

Read our full, actionable report on JELD-WEN here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.