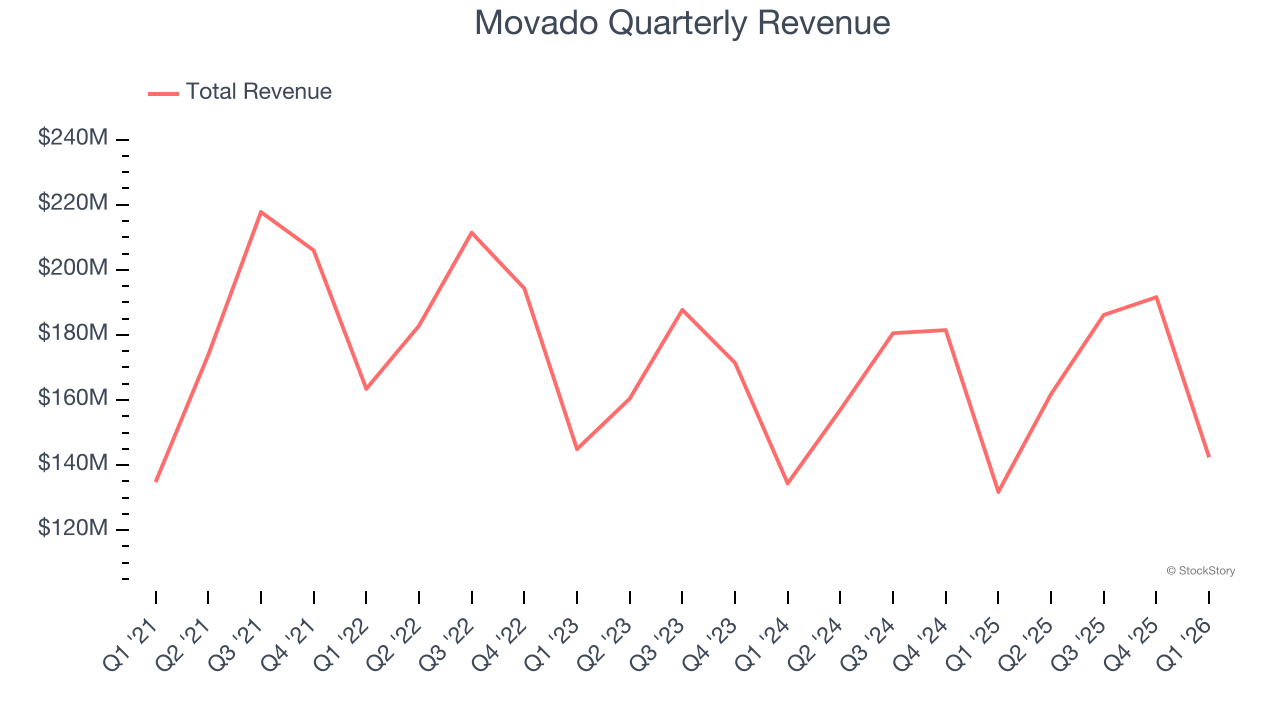

Luxury watch company Movado (NYSE: MOV) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 8.1% year on year to $142.4 million. Its non-GAAP profit of $0.32 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Movado? Find out by accessing our full research report, it’s free.

Movado (MOV) Q1 CY2026 Highlights:

- Revenue: $142.4 million vs analyst estimates of $135.1 million (8.1% year-on-year growth, 5.4% beat)

- Adjusted EPS: $0.32 vs analyst estimates of $0.07 (significant beat)

- Adjusted EBITDA: $9.33 million vs analyst estimates of $3.24 million (6.5% margin, significant beat)

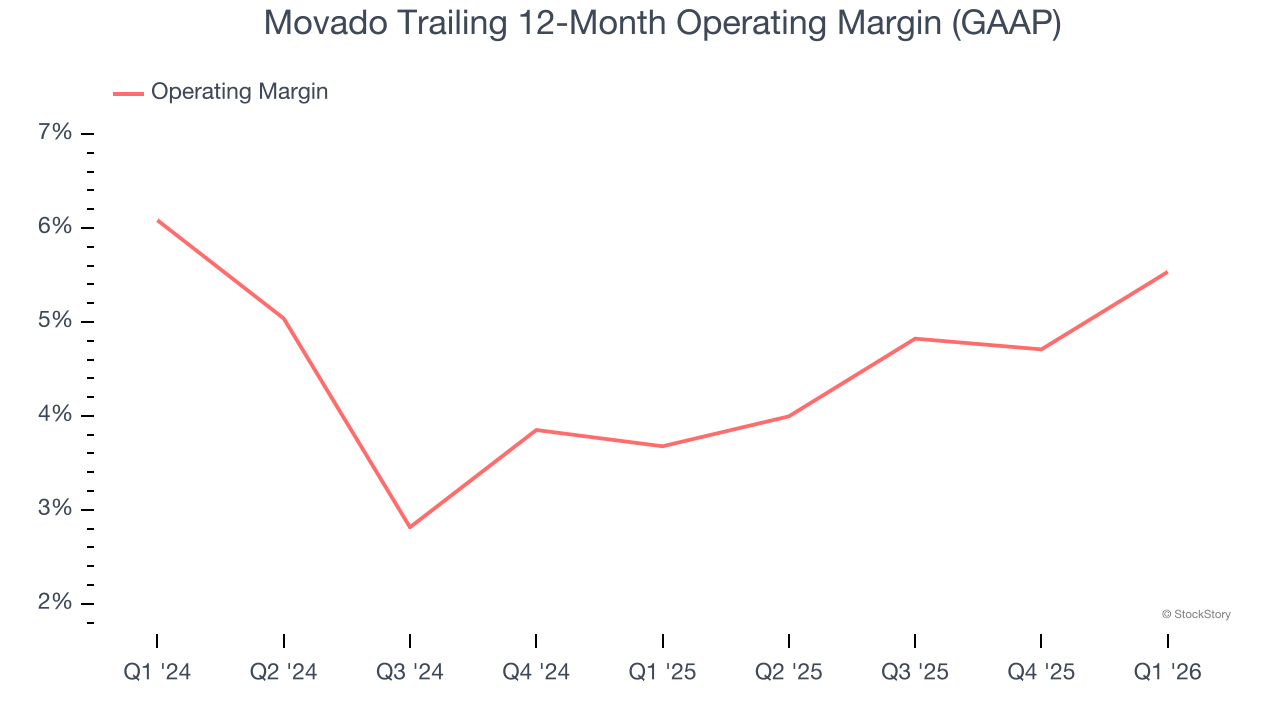

- Operating Margin: 4.9%, up from 0.7% in the same quarter last year

- Free Cash Flow was $5.8 million, up from -$8.75 million in the same quarter last year

- Market Capitalization: $662.8 million

Efraim Grinberg, Chairman and Chief Executive Officer, stated: “We are pleased with our start to the year, accelerating the momentum from year-end and delivering a strong first quarter. We increased net sales by 8%, expanded gross margin by 320 basis points, and delivered earnings per share of $0.30 compared to $0.06 in the prior year — while also making meaningful progress on our strategic initiatives.”

Company Overview

With its watches displayed in 20 museums around the world, Movado (NYSE: MOV) is a watchmaking company with a portfolio of watch brands and accessories.

Revenue Growth

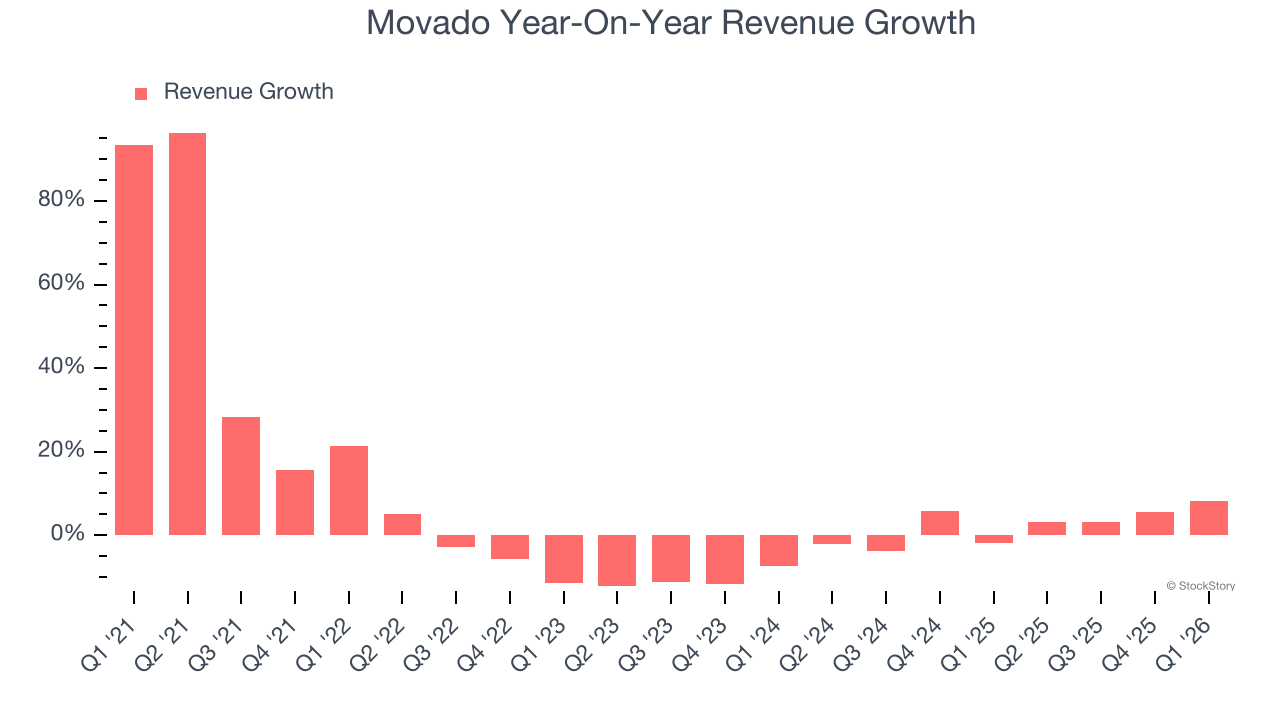

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, Movado’s sales grew at a weak 3.6% compounded annual growth rate over the last five years. This was below our standard for the consumer discretionary sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Movado’s recent performance shows its demand has slowed as its annualized revenue growth of 2.1% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Movado reported year-on-year revenue growth of 8.1%, and its $142.4 million of revenue exceeded Wall Street’s estimates by 5.4%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a slight deceleration versus the last two years. This projection is underwhelming and suggests its products and services will face some demand challenges.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Operating Margin

Movado’s operating margin has been trending up over the last 12 months and averaged 4.6% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

In Q1, Movado generated an operating margin profit margin of 4.9%, up 4.3 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

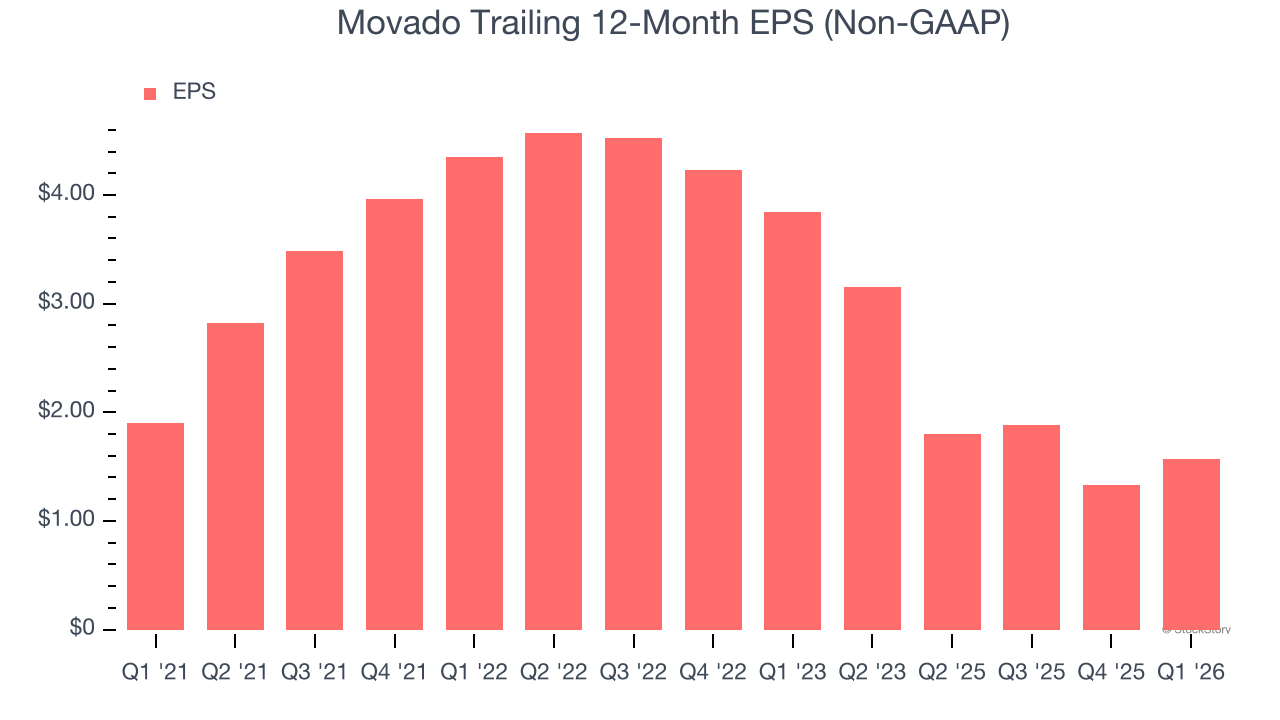

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Movado, its EPS declined by 3.7% annually over the last five years while its revenue grew by 3.6%. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

In Q1, Movado reported adjusted EPS of $0.32, up from $0.08 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Movado’s full-year EPS of $1.57 to grow 5.7%.

Key Takeaways from Movado’s Q1 Results

It was good to see Movado beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 1.4% to $30.25 immediately after reporting.

Indeed, Movado had a rock-solid quarterly earnings result, but is this stock a good investment here? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).