Toyota Motor’s (TM) latest $1 billion investment announcement comes at an interesting time for the company’s stock. The company announced that it would be investing $800 million in Georgetown, Kentucky, and another $200 million in Princeton, Indiana, as part of a larger plan to invest up to $10 billion in its U.S. operations over the next five years.

The question for investors, however, is not just the dollar amount. It’s a sign that the company believes there’s enough demand for its existing lineup in the U.S. to support additional investment, even in a more challenging tariff and regulatory environment.

That’s important for investors to keep in mind. This isn’t a company that’s in trouble. It’s the world’s largest auto manufacturer by sales. Toyota sold a record 11.3 million vehicles in 2025 despite the disruptions caused by the ongoing global trade wars. Yet, the ADR is trading below its 52-week high. So, there’s a bit more to the story here than the most recent news might initially indicate.

About Toyota Stock

Toyota Motor sells cars under the Toyota and Lexus brands and also has a significant financial services segment. The company is headquartered in Toyota City, Japan. The ADR currently has a market capitalization of approximately $274.5 billion, and the company’s scale is an important part of the overall appeal here. It gives the company the ability to continue to make investments in the industry even as many of its peers are forced to play defense.

On the price front, TM has been a solid but not spectacular performer. While the stock has risen about 36% from its 52-week low of $155, it still remains about 15% off its 52-week high of $248.90. This puts Toyota in an interesting position. While the stock may not be particularly cheap based on its book value alone, it has not been driven up like some of its more volatile peers in the auto or EV space. Compared to a more volatile market backdrop, Toyota’s 0.60 beta makes its price movement a positive.

It’s when we discuss valuation, however, that things get particularly interesting. TM currently trades at 10.8 times trailing earnings, 10.9 times forward earnings, 0.85 times sales, and just over 1.0 times book value. For a company like Toyota, which boasts a brand name, a manufacturing presence in multiple countries, and a still-respectable profitability profile, this valuation doesn’t look particularly stretched. In fact, I think it’s more fair to say undervalued.

This is particularly true if one believes that Toyota will continue to successfully defend its profitability margins even as it ramps up domestic U.S. production. As a bonus, the ADR currently boasts a forward dividend yield of 2.4%.

Toyota Beats on Earnings

The latest quarterly announcement from Toyota was a bit mixed at first glance, but it was pretty good after digging a bit deeper. In the latest fiscal third quarter, which was announced on Feb. 6, Toyota announced a quarterly operating income of approximately 1.19 trillion yen, beating estimates, and also saw revenue increase almost 8% year-over-year (YoY) to 13.46 trillion yen. Another announcement from Toyota was that it raised its forecast for operating profit for the year by 11.8% to 3.8 trillion yen, driven by a weak Japanese currency and cost discipline, according to a report from Reuters. That, frankly, is important because it suggests that Toyota is continuing to navigate the impact of tariffs better than most thought.

However, the business isn’t quite firing on all cylinders. While automotive revenue increased 5.7% to 34.17 trillion yen in the first nine months of FY2026, automotive operating income declined 21.3% to 2.42 trillion yen. Similarly, in North America, revenue increased 12.1% to 16.15 trillion yen, but operating income decreased 44.8% to just 94.9 billion yen. This tension in the business is what’s currently driving the stock. This latest effort by the company to invest in U.S. manufacturing is right in line with some of that debate.

The company is trying to protect its long-term market share and align manufacturing with demand. And yes, there are some tariffs and some supply chain issues. But at the same time, you have to think about the philosophy of a company like Toyota, which invests in manufacturing where it sells. This type of manufacturing strategy will be more important in the coming years than people currently realize. I think it's one of the more positive arguments out there right now.

What Do Analysts Expect for TM Stock?

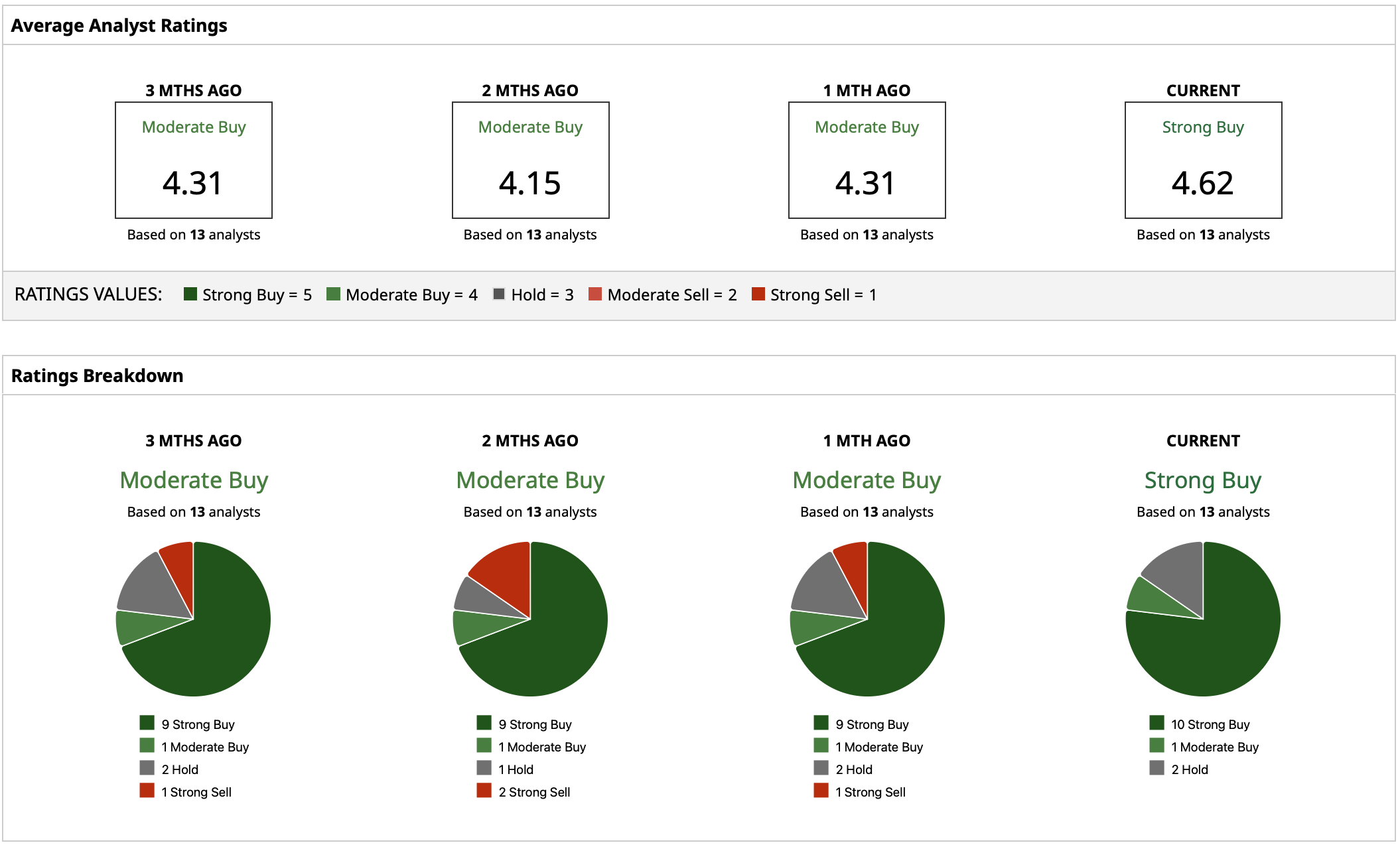

Wall Street seems positive, and analysts’ sentiment has improved with a “Strong Buy” rating consensus. Analysts’ ratings have improved even as the stock has pulled back from its highs. Analysts expect a positive run. Toyota has a mean target price of $248.45 above its current price of about $211. The high target price of $275.90 represents a 31% increase. Even a low target price of $221 represents a 5% increase.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- EchoStar Stock Just Broke Above Its 50-Day Moving Average on SpaceX IPO Hype. Does That Make SATS a Buy?

- Micron Broke Below Its 50-Day Moving Average. Should You Buy the Dip?

- As the Oil Shock Sends Energy Stocks Soaring, Buy These 3 Now

- Warning: Investing in Tech Stocks May Just Be 1 Big, Overcrowded Trade