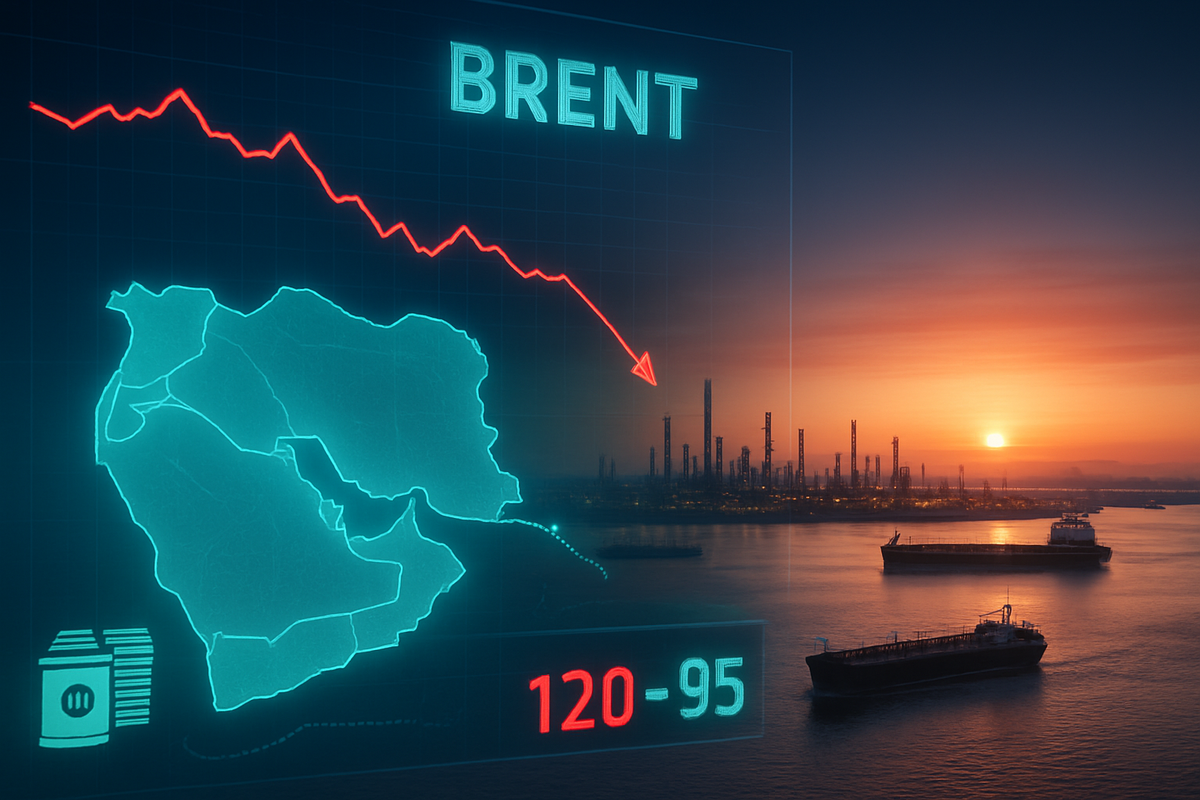

Global energy markets are experiencing a significant "price cliff" this week as Brent crude oil prices retreated from their March peaks near $120 per barrel toward the $95 level. This shift comes amid a flurry of diplomatic activity in the Middle East, sparking hopes for a de-escalation of the regional conflicts that have disrupted global supply chains and sent energy costs soaring earlier this year. As of April 15, 2026, Brent crude settled near $94.81, marking a nearly 13% decline from its wartime highs and providing much-needed relief to a global economy struggling with renewed inflationary pressures.

The sudden cooling of the energy market, often referred to by analysts as the "April Thaw," represents a critical turning point for central banks and policymakers. By easing the immediate "fossilflation" that pushed U.S. headline inflation to 3.3% in March, the stabilization of oil prices offers a potential reprieve for consumer spending and global GDP growth. However, market participants remain cautious, as the underlying structural deficit in oil production and the fragility of the current ceasefire agreements suggest that the road to permanent stability remains fraught with geopolitical risk.

The "April Thaw": Inside the Race for Regional Stability

The rapid descent in oil prices follows a period of extreme volatility triggered by the "Iran War" in early 2026, which saw critical maritime passages like the Strait of Hormuz partially blocked. The current stabilization was catalyzed by a 14-day conditional ceasefire brokered between the United States and Iran on April 7, 2026. This truce was designed to reopen the Strait of Hormuz to the 20 million barrels per day (bpd) of oil and LNG flows that had been restricted during the height of the hostilities. While the physical market remains tight with a structural shortfall of 7–8 million bpd due to infrastructure damage, the removal of the "war risk premium" has allowed prices to slide back into double digits.

The timeline leading to this moment has been characterized by intense "Track II" diplomacy. Following the ceasefire announcement, historic direct talks began in Washington between high-level representatives from Israel and Lebanon, providing psychological relief to energy traders. Simultaneously, a multilateral summit in Islamabad has been working toward a long-term resolution, though these negotiations are currently deadlocked over the duration of a proposed nuclear activity suspension. Despite the stalemate in the Gaza track involving Hamas and the "Board of Peace," the broader regional de-escalation has been sufficient to break the momentum of the oil rally that many feared would top $150.

Initial market reactions have been swift. On the Intercontinental Exchange (ICE), Brent futures plummeted $5 in a single trading session following reports that the first tankers had successfully transited the Strait of Hormuz under the new security protocols. While the global market transitioned from a projected surplus to a 750,000 bpd deficit in the first quarter, the prospect of returning production and stabilized shipping routes has convinced many hedge funds to unwind their long positions in energy futures.

Corporate Divergence: Winners and Losers in the Sub-$100 Era

The retreat in oil prices has created a stark divide among the heavyweights of the energy and transportation sectors. For integrated oil majors like ExxonMobil (NYSE: XOM) and Chevron (NYSE: CVX), the drop below $100 marks a cooling of what had been a record-breaking profit environment. ExxonMobil, which recently traded near all-time highs of $165, saw its shares pull back by roughly 4% this week as the value of its near-term hedges declined. Both Exxon and Chevron have remained relatively insulated compared to their European peers due to their aggressive expansion in the Permian Basin and Guyana, which are shielded from Middle Eastern volatility. Conversely, BP (NYSE: BP) has faced a more difficult transition, reporting a significant working capital build of $4–$7 billion and a 6% drop in share price as it navigates the unwinding of complex hedging strategies in a falling price environment.

On the other side of the ledger, the airline and logistics sectors are breathing a collective sigh of relief. Delta Air Lines (NYSE: DAL) had previously warned of a $2 billion spike in fuel costs for the upcoming quarter, forcing the carrier to cut capacity on off-peak routes. The move toward $95 oil is expected to immediately bolster margins for Delta and United Airlines (NASDAQ: UAL), the latter of which saw a 12% relief rally in its stock price. United's management had previously prepared for a "dire scenario" involving $175 oil, and the current stabilization has reportedly paused discussions regarding emergency defensive "mega-mergers" with competitors like American Airlines (NASDAQ: AAL). For these companies, every dollar drop in the price of jet fuel translates to hundreds of millions in annual savings.

The "Fossilflation" Crisis and the New Energy Order

The significance of this price correction extends far beyond the trading floor, as it hits at the heart of the "fossilflation" trend that has plagued 2026. Global energy prices surged 12.5% year-over-year in early 2026, acting as a massive "energy tax" on consumers and cooling discretionary spending worldwide. The OECD has warned that without a sustained move back toward $80 oil, headline inflation across the G20 could average 4.0% for the full year. This event fits into a broader industry trend where geopolitical volatility has replaced traditional supply-and-demand metrics as the primary driver of the consumer price index.

Historically, periods of "energy-driven inflation" have led to aggressive central bank tightening, but the current scenario is complicated by the transition to renewable energy. Some analysts argue that the volatility of 2026 is a symptom of the "messy middle" of the energy transition, where underinvestment in traditional oil and gas has left the global economy vulnerable to regional shocks. The ripple effects of this price drop are also being felt in the policy world, where the U.S. and EU are reassessing the speed of their decarbonization mandates to ensure short-term energy security doesn't come at the cost of long-term economic stability.

Looking Ahead: The Islamabad Deadline and Beyond

The short-term outlook for oil hinges almost entirely on the Islamabad negotiations, which are set to expire on April 21, 2026. If the conditional ceasefire is not extended or converted into a permanent treaty, analysts warn that Brent could snap back toward $110 or higher overnight. The potential for a strategic pivot remains high; if the "April Thaw" leads to a durable peace, we could see Brent average $90–$95 through the third quarter, potentially settling at a "new normal" of $80 by year-end. However, if Iran remains firm on its 5-year nuclear suspension limit versus the West’s 20-year demand, the ceasefire may prove to be a temporary lull rather than a permanent fix.

Investors must also monitor the potential for a "rebound effect" in demand. As fuel prices ease, the capacity cuts previously implemented by airlines and shipping firms like FedEx and UPS could be reversed, leading to a surge in consumption that tests the limits of current production. The strategic challenge for the market will be managing the 7–8 million bpd structural shortfall that persists despite the ceasefire. Market opportunities may emerge in the energy services sector, as companies are contracted to repair the infrastructure damaged during the recent hostilities in the Persian Gulf.

Assessment of the Market Moving Forward

In summary, the fall of Brent crude toward the $95 level is a vital safety valve for a global economy that was beginning to buckle under the weight of $120 oil. The "April Thaw" has successfully mitigated the immediate threat of a global recession driven by energy costs, but the underlying tensions remain unresolved. The key takeaway for investors is that while the "war risk premium" is currently being priced out, the "structural scarcity premium" remains very much intact.

Moving forward, the market will likely remain in a state of "fragile stability." Investors should keep a close eye on the volume of shipping through the Strait of Hormuz and the daily updates from the Islamabad diplomatic track. The ability of the global economy to sustain its 2.9% GDP growth projection for 2026 depends entirely on whether oil remains in this $90–$100 corridor. As we move into the summer months, the lasting impact of this period will be determined by whether the current ceasefire can be transformed into a lasting regional security framework.

This content is intended for informational purposes only and is not financial advice.